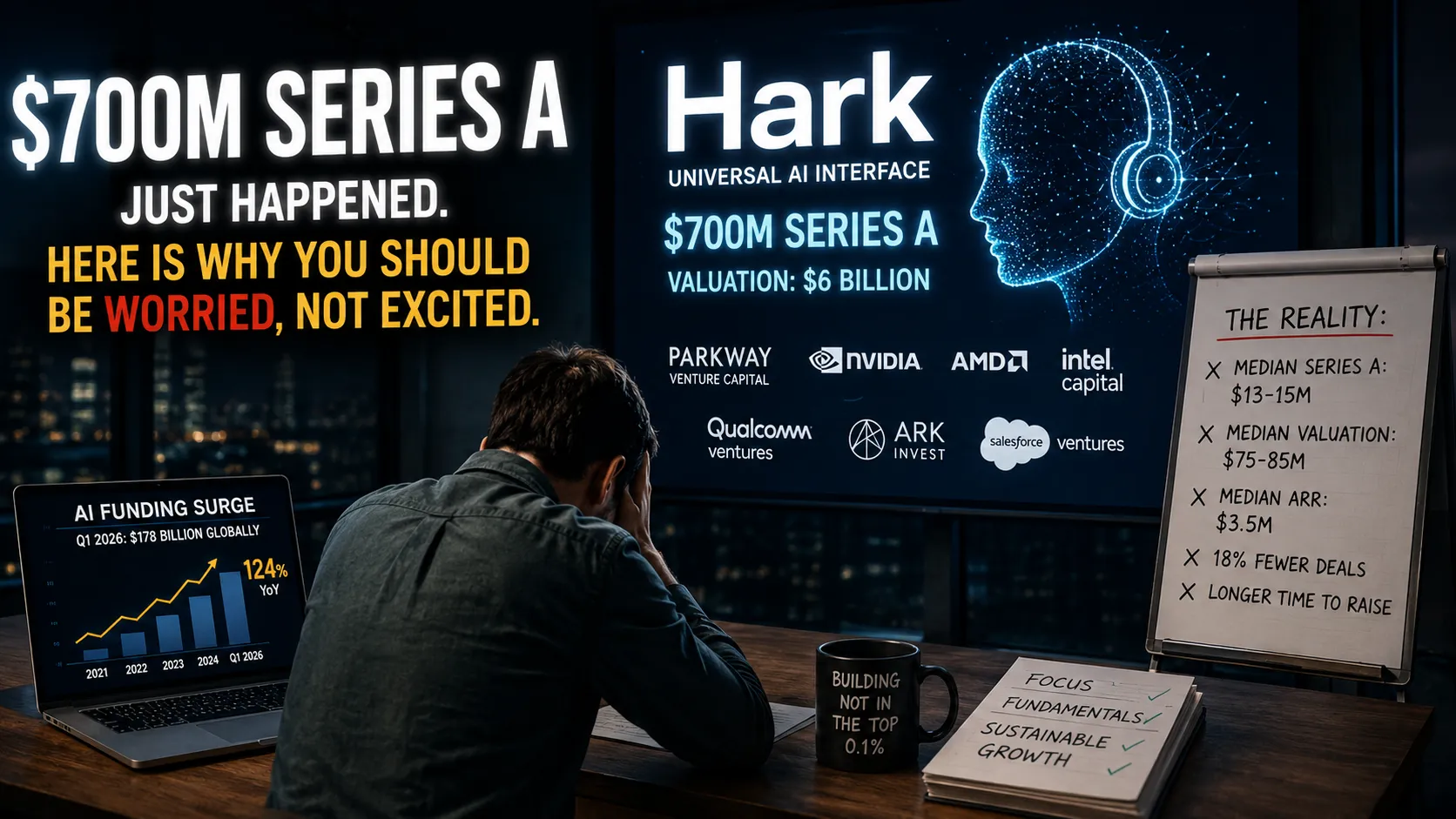

A $700M Series A Just Happened. Here Is Why You Should Be Worried, Not Excited.

On May 21, 2026, an AI startup called Hark announced it had raised $700 million in a Series A round — valuing the company at $6 billion — to build what it described as a "universal AI interface" between humans and machines. The round was led by Parkway Venture Capital and included Nvidia, AMD, Intel Capital, Qualcomm Ventures, ARK Invest, Salesforce Ventures, and several others.

The product? Still largely secret. The traction? Undisclosed. The launch date? Summer 2026, at earliest.

Seven hundred million dollars. Series A. For a product that, at the time of the raise, the public had not yet seen.

A few weeks earlier, spend-management platform Ramp closed $750 million in a single financing. Earlier in the year, foundational AI startups globally raised $178 billion in Q1 alone — more than double all of 2025 combined. US startups overall had pulled in $384 billion by June 2026, a 124 per cent jump on the same period the prior year.

These are the numbers that get written about. These are the numbers that end up in pitch decks as market context slides. These are the numbers that make founders recalibrate their asks and wonder if they are thinking too small.

They are also, in important ways, the most misleading numbers in the startup ecosystem right now. And if you are building a company in 2026 and you are letting the Hark headline shape your expectations, you may be walking into the most consequential financial misunderstanding of your career.

What the Headlines Are Not Telling You

Here is the number that does not make the press release: in Q1 2026, the largest VC quarter on record globally, five deals — Anthropic, xAI, OpenAI tranches, Project Prometheus, and Waymo — accounted for the vast majority of the headline figure. According to analysis by Peony citing PitchBook data, strip out those top five mega-deals and the quarter's figure falls by 73 per cent.

Sixty per cent of all 2025 venture funding went to just 629 companies. The remaining 600,000-plus startups — every other company raising money that year — collectively captured 7 per cent of the capital deployed.

The market has a top. The top is very well-funded. Everything below it is competing for what is left.

This is not a temporary distortion. It is a structural shift. The average number of funding rounds required to reach a $100 million-plus valuation fell from 3.4 rounds in 2020 to 2.6 rounds in 2025. Mega-rounds are not growing bigger — they are arriving earlier, concentrating more capital into fewer hands, faster than at any point in startup history. As one analysis put it plainly: "Concentration is the whole story."

What this means practically is that two very different markets are operating simultaneously under the same headline. One is the AI infrastructure market, where sovereign wealth funds, chip giants, and crossover investors are writing nine-figure checks to a small cohort of companies with defensible moats, established teams, and the kind of founder track records that took decades to build. The other is the market where everyone else is raising.

The Actual Series A Market in 2026

If you are a founder preparing to raise a Series A right now, here are the benchmarks that actually apply to you — not the ones generated by Hark or Anthropic.

The median Series A raise in 2026 is $13 to $15 million, according to Carta data cited by investor Peter Walker, up from $8 to $10 million a few years ago. The median post-money valuation sits at roughly $75 to $85 million. To get to that table, the median ARR required has climbed to approximately $3.5 million — compared to around $1 million just a few years back. The Series A market in 2025 saw an 18 per cent decline in deal volume year-over-year, with total capital invested down 23 per cent. Fewer deals are getting done. The ones that are getting done are at higher bars.

In plain terms: the typical Series A is bigger than it used to be, the bar to raise it is higher than it used to be, and the time between seed and Series A has stretched to around 616 days on average. The 18-to-24-month seed-to-A timeline that founders used to plan around is effectively dead. Sub-$10 million rounds take around 22 months to close. Rounds above $30 million close in 14 to 15 months. The market has split, and the split maps almost exactly onto whether the company is perceived as AI-native or not.

Why Hark Raised $700M at Series A (And Why You Probably Cannot)

Understanding the Hark round requires understanding who Brett Adcock is. Before founding Hark in late 2025 with $100 million of his own capital, Adcock built Figure AI — the humanoid robotics company — and Archer Aviation, the electric aircraft startup. He is a serial founder with a track record of attracting capital for capital-intensive frontier technology bets, a known quantity in the networks where these rounds get syndicated.

Hark is building models and hardware for an AI personal assistant, with a mega-round led by Parkway Venture Capital and including Nvidia, AMD, Intel Capital, Qualcomm Ventures, and Salesforce Ventures, among others. The involvement of semiconductor giants Nvidia, AMD, Intel, and Qualcomm is not incidental. These are strategic investors betting that Hark's hardware ambitions will drive chip demand — meaning part of the capital is coming from companies that have a vested commercial interest in the product existing, not just investors betting on a return.

Investors appear to be betting that the next wave of AI value creation may come less from model access itself and more from ownership of the user interface, memory layer, and interaction environment surrounding AI systems. That thesis — not Hark's product, which remained largely undisclosed at the time of the raise — is what the $700 million is funding.

This is an important distinction. Hark did not raise $700 million because it had demonstrated product-market fit. It raised $700 million because the investors in the round are betting on a market thesis, backed by a founder whose prior history suggests he can execute against it. The product is, in an important sense, secondary to the conviction.

For the vast majority of founders, this playbook is not available. You are not raising capital against a thesis — you are raising against your metrics, your market, your retention numbers, and your ability to convince someone that you specifically can win in a specific space. The rules that applied to Hark's raise are not the rules that apply to your raise.

What Investors Are Actually Buying Right Now

The lion's share of capital now goes to companies already demonstrating product-market fit or infrastructure at scale, making it harder for newcomers to secure initial funding. Pre-seed and seed rounds remain, but their share of total capital is quickly shrinking.

Across the sectors that are attracting the most attention in 2026 — AI, defence technology, logistics, fintech — the pattern is consistent: investors are backing companies that solve expensive, specific, workflow-level problems for buyers who are already spending money in that category. Ramp raised $750 million because it sits directly inside corporate finance budgets. Tennr raised $101 million because it cuts friction in healthcare document processing. Gecko Robotics continues to attract attention because its robots inspect infrastructure where human inspection is dangerous and expensive. These are not "AI-powered" companies in a generic sense. They are companies that happen to use AI to do something that a specific buyer urgently needs done, and that creates a clear line from product to revenue to renewal.

VCs pressure test the quality signals that predict durability: customer concentration, contract structure, revenue composition, and expansion dynamics. Annual and multi-year contracts carry more weight than month-to-month plans. Renewal revenue should make up the clear majority of total revenue.

The implication for founders is direct: the question is not "how do I build an AI product?" It is "what expensive problem does a specific buyer need solved badly enough to sign an annual contract, renew it, and expand it?" The companies that can answer that question with real data are the ones getting funded. Companies that cannot are being told the market is tough.

The Distortion Problem: When Headlines Become Benchmarks

One of the most dangerous things a founder can do in the current market is use Hark's $700 million as a reference point for their own raise.

Median Series A post-money valuation in 2026 is approximately $75 to $85 million. But AI infrastructure companies — foundational model builders and their tooling — are raising seed rounds at $160 to $200 million post-money, creating a distorted benchmark that affects every other founder's expectations without reflecting their actual market.

When a founder walks into a meeting having internalised the Hark or Anthropic numbers, they often anchor at the wrong level — asking for too much at too early a stage, on too thin a set of metrics, against too vague a thesis. The investors they are meeting are not the investors who funded Hark. And the terms those investors use are not the terms Hark raised on.

Series A will be the hardest raise of 2026, according to PitchBook and NVCA analysis. Not the easiest. Not the one boosted by AI enthusiasm. The hardest. Because the bar has risen fastest at this stage — the stage where companies are supposed to have proven something but have not yet reached the scale that attracts growth-stage crossover capital.

What This Means If You Are Building Right Now

The 2026 funding landscape contains a real and important signal underneath all the noise, and it is this: the market is not broken, and it is not uniformly generous. It is structurally bifurcated. There is an AI infrastructure market operating at a scale that has never existed before. And there is everything else, operating on tighter terms, with higher bar requirements, and against a benchmark set by deals that have almost nothing to do with most founders' situations.

If you are building in the second category — which is the category that contains the overwhelming majority of the world's startups — the practical implications are clear. The metrics required to raise a serious Series A have risen significantly and will likely keep rising. The story you tell needs to be specific: one expensive problem, one identifiable buyer, one proof point that shows the pain is real and the solution is working. Investors do not fund categories in 2026. They fund evidence.

Less than 40 per cent of seed-funded startups successfully raise a Series A, so timing matters — raising too early with thin metrics will slow the process and weaken your terms.

And if the raise feels impossibly far away right now — if the Hark numbers make your traction feel trivially small by comparison — it is worth remembering that Suta, the Indian handloom brand, built a ₹75 crore business with ₹6 lakh and zero investors. Ramp, before its $750 million financing, was a real business with real customers and a very clear value proposition. Every company that raised enormous capital at Series A raised it because it had already done the harder, earlier work that the headline number obscures.

The $700 million round is not the story. The story is what has to happen before anyone will write it.

The 2026 funding market will generate the largest headline numbers in startup history. It will also deliver the most selective capital allocation in a generation. The founders who will benefit from it are not the ones benchmarking their raise against Hark — they are the ones solving a specific problem for a specific buyer, building evidence one customer at a time, until the evidence becomes undeniable. That is how every company that eventually raised a large round actually did it. The number at the top of the press release is not the lesson. The decade of work before it is.