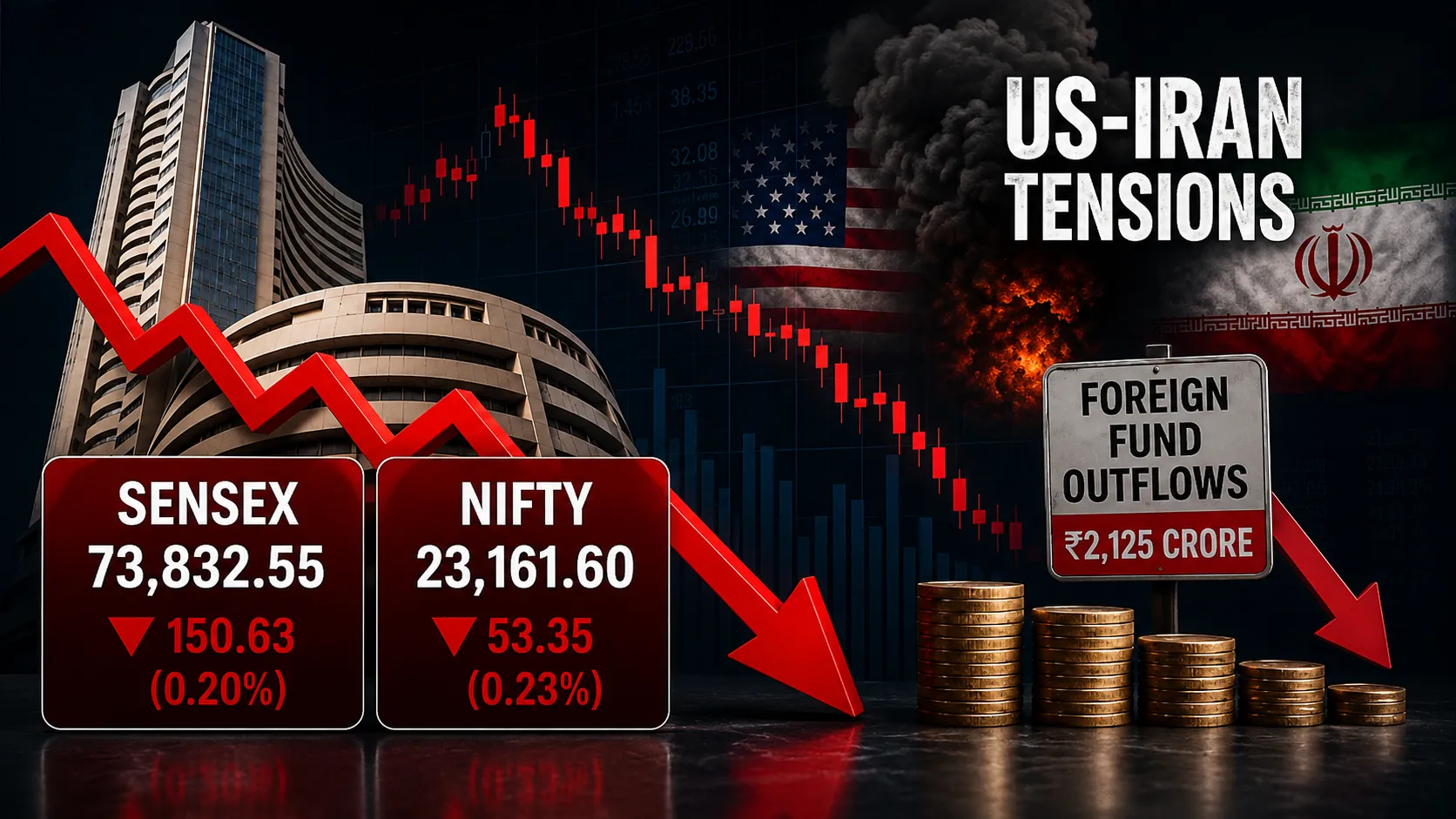

Mumbai's trading floors woke up to red on Tuesday, and by the time the closing bell rang, the mood on Dalal Street had shifted from cautious optimism to genuine unease. The BSE Sensex, India's most-watched equity benchmark, fell by roughly 600 points, or 0.77 percent, dragging the index down to close in the 77,000 band after touching an intraday low as the sell-off gathered pace through the afternoon session. The NSE Nifty 50 mirrored the decline, slipping around 159 points to settle near 24,052, comfortably below the psychologically important 24,100 mark that traders had been defending for much of the previous week.

For a market that had just strung together three consecutive sessions of gains, Tuesday's reversal was a sharp reminder of how quickly sentiment can turn when global geopolitics collide with domestic earnings season. The proximate trigger was not a surprise to anyone who had been watching overnight developments out of the Gulf: the United States Central Command signalled that its forces would resume blockading maritime traffic entering and exiting Iranian ports, reigniting fears of a broader escalation in the already tense standoff between Washington and Tehran. Brent crude, the international benchmark, spiked roughly 5 percent to trade near $87.38 a barrel, its sharpest single-day jump in weeks, as traders priced in the risk of disrupted shipping lanes through the Strait of Hormuz — the chokepoint through which nearly a fifth of the world's oil passes daily.

For India, which imports more than 85 percent of its crude oil requirements, a sudden spike in oil prices is never just an energy story. It is a currency story, an inflation story, and, as Tuesday proved, very much a stock market story. The rupee buckled under the pressure, breaching the 96 level against the US dollar and shedding roughly 57 paise in a single session to trade around 96.20. A weaker rupee raises the cost of imported crude even further, creates a vicious feedback loop for the current account, and forces foreign investors to think twice about holding rupee-denominated assets — all factors that compounded the equity market's troubles on Tuesday.

WHO LED THE FALL

The list of laggards on the Sensex told its own story about where the pain was concentrated. HCL Technologies emerged as the single biggest drag on the index, falling as much as 4.6 percent in a session that came just a day after the IT major reported its June-quarter results. On the surface, HCL Tech's numbers looked solid — consolidated net profit rose over 20 percent year-on-year to around ₹4,624 crore, a marked improvement from the same quarter last fiscal. But investors were unimpressed by management's decision to retain its existing FY27 revenue guidance rather than raise it, reading the conservative stance as a sign that demand visibility in key markets like North America and Europe remains murky. The stock's slide illustrates a pattern that has become familiar this earnings season: strong headline numbers are no longer enough to move IT stocks higher unless they come paired with an upgraded, confident outlook.

Tata Motors was the second major casualty, falling close to 2.7 percent as its passenger vehicle business bore the brunt of investor anxiety over rising input costs. With crude oil prices climbing and global supply chains still sensitive to any hint of Middle East disruption, auto manufacturers — who depend heavily on plastics, resins and shipping-linked input costs — found themselves squarely in the firing line. Bajaj Finserv rounded out the top three decliners, down more than 2.2 percent, as financial stocks broadly came under pressure from the twin worries of currency depreciation and the prospect of tighter global liquidity conditions should oil-driven inflation force central banks to stay hawkish for longer.

They were not alone. Shriram Finance, HDFC Life Insurance, State Bank of India, IndiGo, Jio Financial Services, Mahindra & Mahindra and Larsen & Toubro all fell between roughly 2 and 3.5 percent, reflecting how broad-based Tuesday's sell-off truly was. IndiGo's decline was particularly notable given its direct exposure to fuel costs: aviation turbine fuel prices move in near lockstep with crude, and any sustained rally in oil eats directly into airline margins. Market breadth confirmed the scale of the pullback — more than 2,278 shares closed lower on the NSE compared with just over 1,000 that ended in positive territory, a ratio that underscored just how few pockets of the market were spared.

THE POCKETS OF RESILIENCE

Not every heavyweight stock succumbed to the selling pressure. Bharti Airtel, Apollo Hospitals, Sun Pharmaceutical Industries, Dr Reddy's Laboratories, Tata Steel, JSW Steel and Tata Consultancy Services all bucked the trend to close in positive territory. The gainers list offers a useful lens into how professional money managers were positioning through the volatility: defensive sectors such as pharmaceuticals and healthcare, which tend to be less sensitive to currency and oil-price shocks, attracted buying interest, as did select metal stocks that can sometimes benefit from a weaker rupee through higher realisations on export-linked revenue. Telecom, too, proved relatively insulated, with Bharti Airtel's domestic-revenue-driven business model largely shielded from the crude-and-currency double whammy hitting oil-import-dependent sectors.

Sector-wise, the damage was concentrated in real estate, which emerged as the single worst-performing segment on the exchanges, falling roughly 2 percent as profit-booking swept through property developer stocks. Real estate stocks are particularly sensitive to interest-rate expectations, and any scenario in which imported inflation forces the Reserve Bank of India to hold rates higher for longer tends to weigh disproportionately on housing finance costs and, by extension, developer valuations.

WHY THIS MATTERS BEYOND ONE TRADING SESSION

It would be easy to dismiss a single 600-point fall as routine market noise — Indian equities, after all, have weathered sharper single-day declines in recent years. But Tuesday's session is worth paying closer attention to for three reasons.

First, it snapped what had been a promising three-session winning streak, one that had been built on optimism around corporate earnings and hopes that global interest rates might soon start easing. That optimism now faces a real test: can Indian markets absorb a sustained period of elevated crude prices without a meaningful repricing of growth and inflation expectations?

Second, the sell-off arrived squarely in the middle of India's June-quarter earnings season, a period when investors typically look past macro noise to focus on company fundamentals. The fact that even a company like HCL Tech — which beat profit estimates — could not escape the sell-off is telling. It suggests that macro headwinds, not micro-level earnings disappointments, are currently the dominant force driving price action on Dalal Street. Traders will be watching Wipro's results, due later this week, and the broader IT sector's commentary on demand trends and AI-linked pricing pressure even more closely as a result.

Third, and perhaps most importantly for retail investors and NRIs tracking Indian markets from abroad, Tuesday's price action is a reminder of how tightly interconnected India's equity market, currency market and global energy prices have become. A shock originating thousands of kilometres away in the Strait of Hormuz can, within hours, translate into a nearly one percent drop in Sensex value, a weaker rupee, and renewed questions about the trajectory of India's trade and current account balances — questions that become especially relevant against the backdrop of India's otherwise robust export performance this quarter (a story covered in detail elsewhere in this edition).

WHAT ANALYSTS ARE WATCHING NEXT

Market strategists caution against reading too much into a single session's move, but they are unanimous that the path of crude oil prices over the coming days will be the single biggest swing factor for Indian equities in the near term. Should the situation around the Strait of Hormuz de-escalate and shipping traffic normalise, Brent crude could just as quickly retrace its gains, providing relief to the rupee and to rate-sensitive sectors like autos, real estate and financials. Conversely, any further military escalation or a formal disruption to tanker traffic through the strait could push oil meaningfully higher, testing the Reserve Bank of India's tolerance for currency intervention and potentially delaying any prospective rate cuts.

For long-term investors, particularly the growing base of global Indians who allocate capital to Indian equities as part of a broader diversification strategy, the message from Tuesday's trading session is one of discipline rather than panic. Single-session volatility driven by geopolitical headlines has historically proven far less predictive of medium-term market direction than earnings trends and domestic macro fundamentals — both of which, as this week's export data shows, continue to tell a more encouraging story about the underlying health of the Indian economy. The coming days of earnings announcements from India's largest companies, layered against an unpredictable geopolitical backdrop, will determine whether Tuesday's dip was a brief wobble or the opening chapter of a more sustained repricing.

THE CURRENCY DIMENSION TRADERS CAN'T IGNORE

If there is one thread tying together Tuesday's equity sell-off with the wider set of stories dominating India's business news cycle this week, it is the rupee. A currency that slips past a key psychological level against the dollar does more than dent the returns of importers; it recalibrates the entire risk calculus for foreign portfolio managers who think in dollar terms. When the rupee weakens sharply in a single session, the dollar-denominated value of every Indian equity holding in a foreign portfolio falls in tandem, even if the underlying stock price in rupee terms barely moves. That mechanical effect alone can be enough to trigger a wave of tactical selling from overseas funds looking to protect portfolio-level returns — a dynamic that likely compounded Tuesday's domestic-led sell-off and one that ties directly into this week's broader story about foreign institutional investors snapping their recent buying streak.

The Reserve Bank of India, for its part, has historically preferred to smooth currency volatility gradually through calibrated interventions rather than allow sharp, disorderly moves in either direction. Traders and currency desks will be watching closely over the coming sessions for any sign of RBI intervention in the forex market, particularly if crude prices remain elevated and continue to pressure the rupee. A sustained defence of the currency would likely require the central bank to draw down foreign exchange reserves, a move that itself carries longer-term implications for India's external buffers should the Middle East situation fail to de-escalate quickly.

HISTORICAL CONTEXT: HOW MARKETS HAVE HANDLED PAST OIL SHOCKS

Indian equity markets are, unfortunately, no strangers to oil-driven volatility. Previous episodes of Middle East tension — from the aftermath of regional conflicts to earlier standoffs involving Iran's oil exports — have tended to follow a broadly similar pattern: a sharp initial sell-off concentrated in oil-import-sensitive sectors, followed by a period of elevated volatility that persists for as long as the underlying geopolitical uncertainty remains unresolved, and then a gradual normalisation once either the conflict de-escalates or markets simply adjust to a new, higher baseline for crude prices. What distinguishes the current episode is the timing: it has landed squarely in the middle of an earnings season already carrying its own crosscurrents, from IT sector caution around AI-driven pricing pressure to record export data that paints a considerably more optimistic picture of the underlying economy.

That juxtaposition — encouraging fundamental data on one hand, an unpredictable external shock on the other — is precisely the environment in which experienced market participants tend to counsel patience. Retail investors, index-linked systematic investment plan holders, and long-horizon NRI investors are typically best served by resisting the urge to react to single-session headlines, instead keeping their focus on the underlying trajectory of corporate earnings and macroeconomic fundamentals that unfold over months and quarters rather than single trading sessions. Whether Tuesday's decline proves to be a footnote or the start of a more prolonged correction will likely become clear only once the geopolitical picture out of the Gulf comes into sharper focus in the days ahead.

Domestic institutional investors, notably, continued to provide a measure of stability even as the benchmark indices slid, with mutual fund buying and steady systematic investment plan inflows partially cushioning the impact of any foreign portfolio caution — a structural feature of Indian markets that has repeatedly proven its worth during past bouts of externally driven volatility. As earnings season progresses and the geopolitical picture around the Strait of Hormuz becomes clearer, market participants across Mumbai's trading desks and abroad will be watching just as closely for the next signal, whether that arrives in the form of a ceasefire announcement, a fresh escalation, or simply another quarter of steady corporate results reasserting the fundamentals over the noise.

---