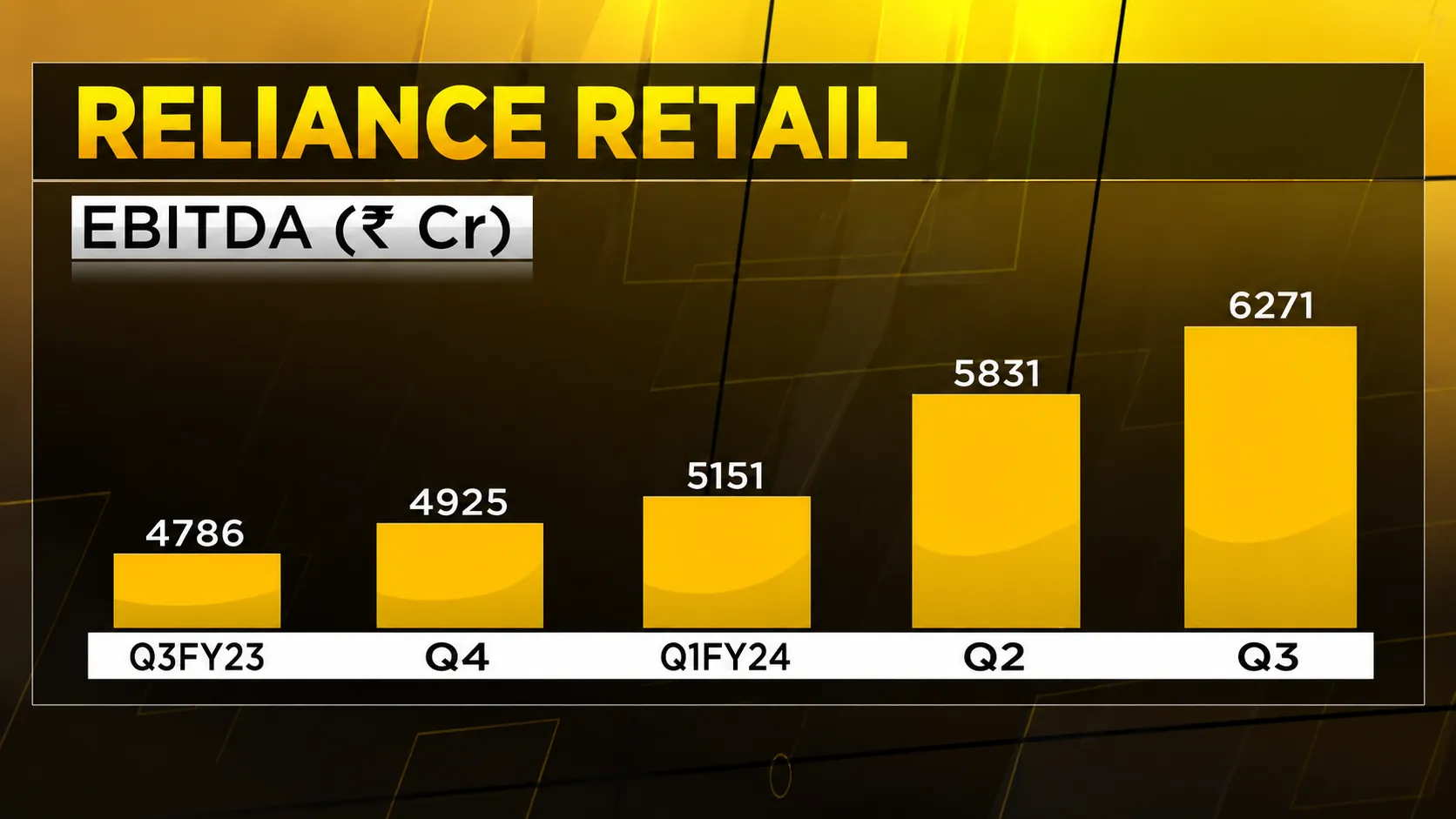

Amid the blockbuster headline numbers dominating Reliance Industries' Q1FY27 results disclosure on July 17, 2026 — the record O2C revenue, the margin-accretive Jio Platforms performance — one segment delivered a comparatively quieter, more measured quarter: Reliance Retail Ventures, the group's sprawling consumer-facing retail arm, which posted revenue of ₹90,408 crore, up 7.4 percent year-on-year, even as segment EBITDA slipped 1.1 percent to ₹6,309 crore.

**The headline numbers in context**

For a business of Reliance Retail's scale — India's largest retailer by a considerable margin, spanning grocery, fashion, consumer electronics, and an increasingly significant digital commerce footprint — high single-digit revenue growth alongside a marginal EBITDA decline represents a notably different growth profile from the double-digit revenue and EBITDA expansion posted by sister segments Jio Platforms and Oil-to-Chemicals this quarter. Commenting on the results, Reliance Industries Chairman and Managing Director Mukesh Ambani described the retail business as having delivered "resilient growth this quarter, with steady performance across all consumption formats and channels" — carefully measured language that reads as an acknowledgement of a quarter defined more by operational consolidation and steady execution than by the kind of headline-grabbing growth metrics that have characterised some of Reliance Retail's earlier expansion phases.

**Why the EBITDA dip matters — and why it may not be alarming**

A 1.1 percent year-on-year EBITDA decline against 7.4 percent revenue growth implies a modest but real compression in overall segment margins during the quarter. For a retail business of Reliance's scale and diversity, several factors typically drive this kind of divergence between revenue and profitability growth in any given quarter: shifts in the mix of formats and categories contributing to revenue, near-term cost pressures associated with store network optimisation or new format rollouts, promotional or pricing activity aimed at defending market share in an increasingly competitive Indian retail landscape, and broader input cost pressures — particularly relevant this quarter given the elevated crude-oil-linked cost environment affecting packaging, logistics, and certain imported categories across the sector. Without more granular category-level disclosure, it is difficult to pinpoint the precise driver of this quarter's margin softness with certainty, but the broader context — a quarter marked by currency volatility and elevated energy costs across the Indian economy — suggests at least part of the pressure likely reflects macro cost headwinds common to the broader organised retail sector, rather than company-specific execution issues unique to Reliance Retail.

**A business in a different phase of its growth journey**

To properly contextualise this quarter's numbers, it helps to situate Reliance Retail within the broader arc of its now more than decade-long expansion since Reliance first entered organised retail in the mid-2000s. The business's earlier growth phases were characterised by extremely rapid, capital-intensive store network expansion, as Reliance raced to build out grocery, fashion, and electronics retail footprints across hundreds of Indian cities and towns. In more recent years, the company's strategic emphasis has shifted increasingly toward optimising the productivity and profitability of its existing, now-substantial store network, alongside building out digital commerce capabilities through platforms including JioMart, and increasingly, toward integrating its retail operations more closely with Jio's broader digital ecosystem to create bundled, cross-platform customer engagement and loyalty benefits. A quarter like this one — modest revenue growth, slight margin softness, but explicitly "steady performance across all consumption formats and channels" — fits a business in this more mature optimisation phase considerably better than it would a business still in an aggressive, store-count-driven land grab phase.

**How Reliance Retail compares to the broader Indian retail sector**

Placing Reliance Retail's growth within the broader context of India's organised retail sector offers useful additional perspective. Indian retail more broadly has navigated a genuinely challenging macro environment through much of 2026, with currency depreciation driving up costs for imported categories, elevated fuel prices squeezing discretionary consumer spending in certain segments, and broader caution among middle-income consumers amid the uncertain macroeconomic backdrop created by the ongoing Strait of Hormuz-driven energy crisis. Against that backdrop, Reliance Retail's ability to deliver positive revenue growth at all — let alone growth in the mid-to-high single digits — reflects meaningfully greater resilience than several smaller, less diversified retail competitors have been able to demonstrate over the same period, even if the segment's own growth trajectory has moderated relative to its own historical high-growth years.

**The grocery and essentials anchor**

Within Reliance Retail's diversified portfolio, the grocery and essentials category has historically functioned as the segment's most resilient revenue anchor, given the inherently less discretionary, more recession-resistant nature of consumer spending on daily essentials compared to categories like fashion, lifestyle, or consumer electronics that are more sensitive to broader economic sentiment and discretionary spending cycles. In a quarter marked by elevated inflationary pressure across parts of the economy — itself partly a function of the same crude-oil-driven cost pressures affecting O2C segment pricing this quarter — a grocery-anchored retail portfolio likely provided Reliance Retail with a degree of revenue stability that more discretionary-category-focused retailers may not have enjoyed to the same extent.

**Digital commerce and the JioMart integration story**

Beyond its physical store network, Reliance Retail's digital commerce ambitions, centred around the JioMart platform, continue to represent an important — if less granularly disclosed in this quarter's headline results — component of the broader retail growth story. The strategic logic of integrating JioMart's digital ordering and delivery capabilities with Reliance's vast physical store network, and increasingly with Jio's telecom and digital services ecosystem more broadly, reflects a long-term bet that the combination of physical retail scale, digital commerce convenience, and telecom-driven customer reach can create a genuinely differentiated retail proposition relative to both pure e-commerce players and traditional brick-and-mortar retailers operating without comparable digital or telecom integration capabilities.

**What comes next for Reliance Retail**

Looking ahead, investors and analysts tracking Reliance Retail will be watching closely for signs of whether this quarter's modest EBITDA softness proves to be a transient, single-quarter phenomenon tied to the specific macro cost pressures affecting the broader Indian retail sector this period, or whether it signals the beginning of a more sustained period of margin normalisation as the business matures beyond its earlier hyper-growth phase. Category-level performance — particularly within grocery, fashion and lifestyle, and consumer electronics — alongside continued disclosure on digital commerce penetration through JioMart, will likely remain the key metrics shaping how the market interprets Reliance Retail's trajectory through the remainder of FY27. For a business that remains, by a considerable margin, India's largest organised retailer, even a "steady" quarter represents a scale of operation that few domestic or international competitors can match, underscoring why Reliance Retail continues to be viewed as a structurally important, if not always the most dynamically growing, pillar of the broader Reliance Industries growth story.

**Competitive pressure from quick commerce and e-commerce**

One important contextual factor shaping this quarter's margin story is the intensifying competitive landscape Reliance Retail now navigates, particularly from the rapidly scaling quick commerce segment that has reshaped Indian urban grocery and essentials shopping behaviour over the past several years. Quick commerce platforms promising delivery within 10 to 30 minutes have captured substantial wallet share among urban consumers, particularly for smaller, top-up grocery purchases that were previously the domain of neighbourhood kirana stores and, increasingly, larger organised retail chains including Reliance's own grocery formats. Responding to this competitive pressure has required organised retailers like Reliance Retail to invest in their own faster-delivery capabilities and digital ordering infrastructure, investments that carry near-term cost implications even as they aim to protect long-term market share and customer relationships against nimbler, venture-capital-funded quick commerce challengers.

**The scale advantage that remains intact**

Despite this quarter's more measured growth profile, it is worth reiterating just how substantial Reliance Retail's underlying scale advantage remains within the Indian retail landscape. With quarterly revenue exceeding ₹90,000 crore, the business continues to operate at a scale that dwarfs virtually every other organised retail competitor in the country, spanning an extensive physical store network alongside its growing digital commerce capabilities. This scale advantage translates into meaningful negotiating leverage with suppliers, superior logistics and supply chain economics, and a breadth of category coverage — from groceries to fashion to consumer electronics to pharmacy — that few competitors can match within a single integrated retail platform. Even a "steady," lower-growth quarter for a business of this scale represents an absolute revenue and profit contribution that continues to make Reliance Retail one of the most important individual pillars supporting Reliance Industries' overall conglomerate valuation, alongside Jio Platforms and the O2C business.

**What analysts will listen for on the earnings call**

Beyond the headline segment numbers disclosed in Reliance's results presentation, analysts covering the stock will likely probe management commentary during the post-results earnings call for additional colour on the specific drivers behind this quarter's EBITDA softness, including any guidance on expected margin trajectory for the remainder of FY27, updates on store network expansion or consolidation plans, and further detail on JioMart's digital commerce growth trajectory relative to the broader e-commerce and quick commerce competitive landscape. Management's tone and specificity on these questions will likely shape near-term analyst rating and price target revisions for Reliance Industries stock more than the headline retail segment numbers alone.

**Fashion and lifestyle: a category under particular scrutiny**

Within Reliance Retail's broader category mix, the fashion and lifestyle segment — encompassing formats ranging from value fashion retail to premium and luxury brand partnerships — has historically been viewed by analysts as one of the more discretionary, and therefore more macro-sensitive, components of the overall retail portfolio. In an environment of currency depreciation and elevated consumer caution around discretionary spending, this category would typically be expected to show more pronounced softness than the grocery and essentials business, and analysts parsing more granular category-level disclosure, when available in fuller quarterly reporting, will likely pay particular attention to whether fashion and lifestyle growth has decelerated more sharply than the overall blended retail segment figures suggest, or whether the category has proven more resilient than the broader macro backdrop might imply.

**Consumer electronics and the import cost connection**

The consumer electronics category within Reliance Retail's portfolio carries a particularly direct linkage to this quarter's currency and import cost dynamics, given the segment's inherent dependence on imported components and finished goods, many of which are priced in US dollars. As the rupee has weakened amid the ongoing Strait of Hormuz-driven currency pressure, landed costs for imported electronics inventory have risen correspondingly, creating a direct margin pressure point for retailers unable to fully pass through these higher costs to price-sensitive Indian consumers without risking demand destruction. This dynamic offers one plausible, if unconfirmed, explanation for at least part of this quarter's overall segment margin softness, though definitive attribution would require the kind of granular category-level cost breakdown that Reliance has not disclosed within its headline quarterly results presentation.

**Reading Reliance Retail alongside the broader RIL narrative**

It is worth situating this quarter's retail performance within the broader context of how Reliance Industries as a whole chose to communicate its Q1FY27 story to the market. With O2C delivering record revenue and Jio Platforms posting margin-accretive growth ahead of its landmark IPO, Reliance Retail's more measured "steady" narrative this quarter arguably received comparatively less management and analyst attention than it might have in a quarter where the other two segments had delivered less spectacular results. This dynamic illustrates an interesting feature of Reliance's diversified conglomerate structure: strong performance in one or two segments can effectively buy the company's overall growth story some room for a more measured, consolidation-focused quarter in another segment without triggering the kind of intense standalone scrutiny that a similar retail performance might attract at a company where retail represented the sole or primary business line. As Reliance Retail continues navigating its transition from hyper-growth expansion toward disciplined, margin-conscious scaling, subsequent quarters will offer further evidence of whether this quarter's pattern represents the new normal for the segment or merely a single period of consolidation ahead of renewed acceleration. Overall, the quarter reinforces that Reliance Retail's next major re-rating catalyst is likely to come not from a single dramatic announcement but from a sustained, multi-quarter demonstration that margins can reaccelerate once the current currency and cost headwinds subside.