As global markets post headline-grabbing returns, a startling truth hides beneath the surface — most of the world's wealth creation is being captured by a breathtakingly small club of companies. What does this mean for your portfolio?

By The Impactful Global Indian — Markets Desk

The global stock market looks like a celebration from the outside. Indexes are hitting new highs, analyst forecasts are bullish, and financial television anchors speak of a broadening bull market with the enthusiasm of festival season. But strip away the headline numbers, and an uncomfortable truth emerges: the party is happening in one very exclusive room, and most investors are standing outside with their noses pressed against the glass.

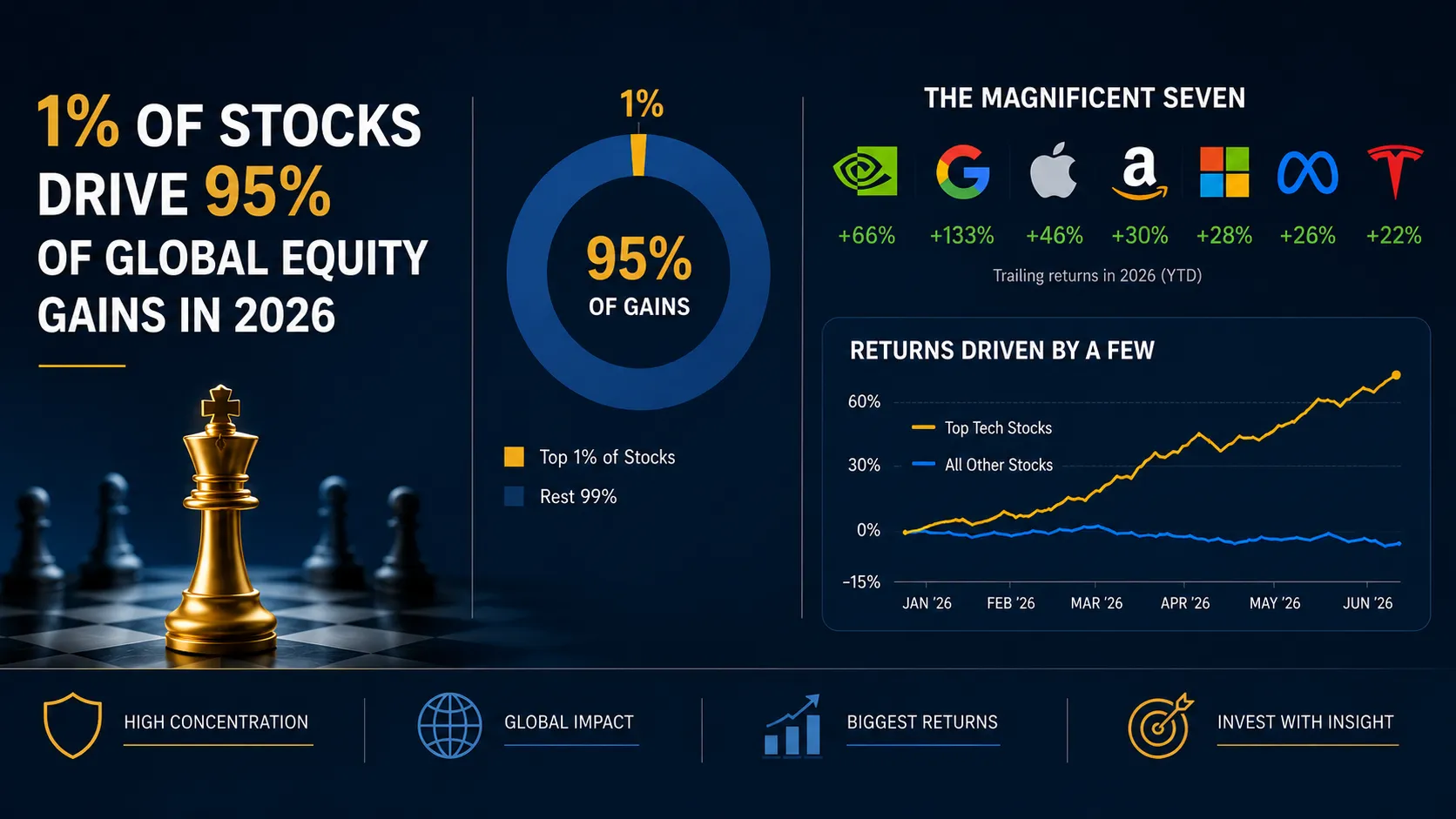

A remarkable — and deeply unsettling — phenomenon has taken hold of global equity markets in 2026: just one percent of listed stocks worldwide are responsible for generating approximately 95 percent of all equity wealth created this year. For the everyday investor, for the Indian diaspora professional managing a 401(k) or a Demat account, this is not a footnote. It is the entire story.

The Illusion of Broad-Based Growth

Goldman Sachs Research forecasts global equity returns of 11 percent for 2026, including dividends. Bank of America projects S&P 500 earnings growth of 14 percent. The FTSE All World Index returned a staggering 23.1 percent in 2025. These are the numbers that make headlines — the numbers that cause fund managers to smile and retail investors to feel reassured that their money is working hard for them.

But the data beneath the surface tells a profoundly different story. The top 10 stocks in the FTSE USA alone now control nearly 40 percent of the index — a level of concentration not witnessed since the 1960s. Inside the S&P 500, just five mega-cap names — NVIDIA, Apple, Microsoft, Alphabet, and Amazon — collectively account for roughly 26 percent of the entire index. According to Goldman Sachs Asset Management, in 2025, the top technology stocks alone were responsible for 53 percent of the S&P 500's total return. In 2026, that concentration has, if anything, intensified.

"The top 2 stocks in the FTSE USA weigh more than the combined weight of the entire Energy, Utilities, Real Estate, Telecommunications, and Basic Materials industries."

— LSEG / FTSE Russell Research, January 2026

Read that again. Two companies — outweighing five entire industries. This is not diversification. This is concentration masquerading as an index fund.

The New Magnificent Architecture of Wealth

The stocks doing the heavy lifting are well known to any market watcher: the so-called Magnificent Seven — Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla. These seven companies, operating at the crossroads of artificial intelligence, cloud computing, and consumer technology, have restructured what it means to participate in equity market growth.

NVIDIA, the undisputed torchbearer of the AI infrastructure era, returned 66 percent over the trailing year. Alphabet surged 133 percent. Apple climbed 46 percent. Amazon gained 30 percent.

Investors who held these names through the volatility — through the VIX spike above 31 in late March 2026, through trade friction anxieties, through geopolitical noise — were richly rewarded.

Those who did not are looking at a market that appears to be working, while their portfolios tell a quieter, more sobering story.

What This Means in Plain English

If you hold a diversified index fund, you may believe your money is spread across hundreds or thousands of companies. In reality, a market-cap-weighted S&P 500 tracker places roughly one rupee of every four — or one dollar of every four — in just five technology corporations. Diversification, as traditionally understood, is no longer what the label says it is.

An Indian Perspective: Why This Matters to You

For the Global Indian — whether you are a software engineer in Silicon Valley managing a portfolio, a finance professional in London with ISA investments, or a Mumbai-based investor with exposure to international equity funds — the implications of this concentration are not abstract. They are personal.

Indian investors have increasingly embraced international equity exposure through Liberalised Remittance Scheme (LRS) investments, international mutual funds, and NRI brokerage accounts. Many of these vehicles are benchmarked against or heavily correlated with the S&P 500 or global indices. What they may not realise is that their global diversification often means concentrated exposure to the same seven American technology companies, wrapped in different product names.

Emerging markets, including India, offer a genuine alternative narrative. U.S. Bank's latest market analysis confirms that emerging markets are leading major global stock index gains this year — between 8.6 percent and 20.9 percent — with nine of eleven S&P 500 sectors still positive year to date.