The Rhythm That Defines a Mature Market

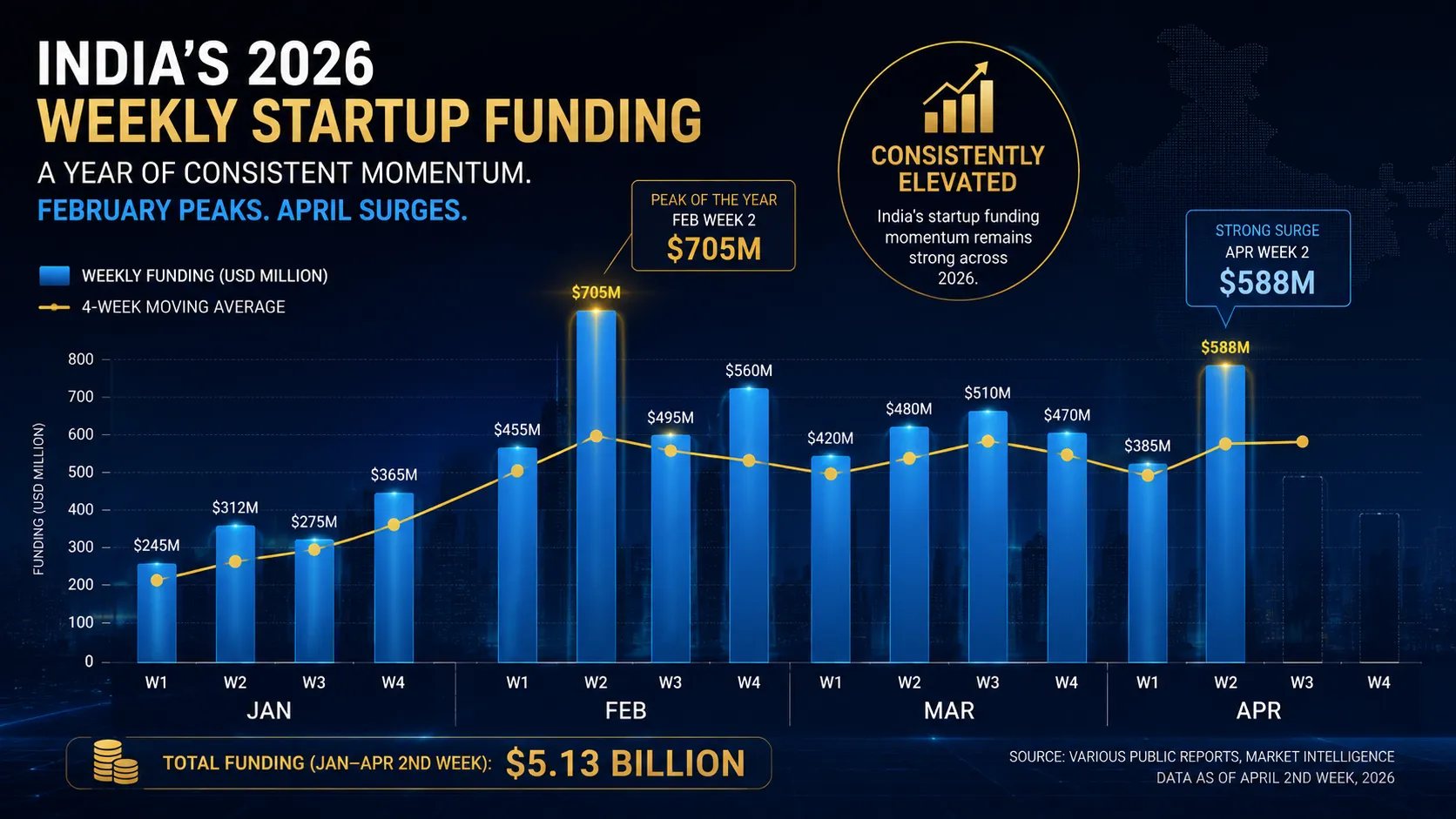

Markets do not achieve maturity through individual spectacular events. They achieve it through the accumulation of consistent, broad-based activity that fills the calendar without requiring any single watershed deal to maintain the pace. The most telling indicator of a mature investment market is not the height of its peak weeks but the floor of its slow weeks — the level of activity that the market sustains even when no single large deal is generating headlines.

India's startup funding market, measured through this lens, has matured significantly. The $588 million week of April 14-21 — the second week of April 2026 — would have been extraordinary by the standards of any prior year. In 2026, it is the second time in the year that weekly funding has exceeded $500 million, suggesting that this level of activity is approaching the new normal rather than representing an exceptional departure from it.

The comparison to February's $705 million week is instructive. February's record was driven significantly by the India AI Impact Summit's immediate aftermath, when the announcement of over $200 billion in commitments catalyzed a surge of deal-closing activity that had been building through the preceding months. The April week has no such obvious catalyst. It is an expression of the underlying pace of deal-making in the ecosystem — deals that were being developed through months of relationship-building, due diligence, and negotiation, reaching the closing threshold in the same week by coincidence rather than by any common external event. This is what a market looks like when it is operating at maturity: consistent deal flow that fills the calendar without requiring external events to trigger activity.

KreditBee at the Center: A Case Study in Platform Lending Economics

KreditBee's $280 million Series E, which dominated the media coverage of the week, is worth examining in detail as a case study in the economics of platform lending at scale — because the investor thesis behind this round illuminates why India's fintech sector continues to attract capital even in a global environment that has become more skeptical of growth-stage lending businesses.

Platform lending, as KreditBee practices it, is different from traditional banking in ways that are not immediately obvious to observers familiar with conventional financial services. The difference is not primarily in the product — personal loans are personal loans. The difference is in the information asymmetry that platform lending overcomes, and the mechanism through which it overcomes it.

Traditional personal lending requires the borrower to have a formal credit history — a record of prior borrowing and repayment that allows the lender to assess default probability. This requirement excludes the hundreds of millions of Indians who are new to formal credit — who have never had a credit card, never taken a bank loan, never been scored by a credit bureau. They may have excellent financial discipline, demonstrated through years of timely payment of rent, utilities, and informal loans. But without formal credit history, traditional lenders cannot see this discipline, and therefore cannot lend.

KreditBee uses alternative data — patterns of smartphone usage, app behavior, transaction history on mobile payment platforms, and other digital signals that correlate with creditworthiness — to build assessments of borrower quality that do not require formal credit history. The models that power these assessments are trained on actual loan repayment data from KreditBee's own portfolio — data that grows more informative with every loan originated and every repayment observed. The system gets better over time, improving both accuracy and the range of borrowers it can serve with appropriate confidence.

This self-improving model quality is a genuine competitive advantage — one that compounds with scale in a way that traditional credit risk models cannot. The investor thesis for the $280 million round is, fundamentally, a thesis about this compounding: that KreditBee's model quality advantage will continue to grow, that the market for the borrowers it can uniquely serve will continue to expand as India's middle class grows and formal credit penetration increases, and that the company's current market position is a durable foundation for the scale it aspires to.

The Global Context: India's Decoupling From Western Funding Cycles

The April 2026 funding surge — and the broader pattern of strong Indian startup funding in a period when global technology investment has become more cautious — raises a question that deserves direct engagement: is India decoupling from global funding cycles, and if so, what does that mean?

The evidence for partial decoupling is real. Global venture capital deployment has slowed as rising interest rates have made growth capital more expensive and as the recalibration of public technology valuations has forced private market investors to rethink the valuation assumptions built into their portfolio models. In this environment, many global VC firms have extended their hold periods, slowed new investment, and focused their attention and capital on supporting existing portfolio companies rather than making new bets.

India's domestic funding activity has not followed this pattern at the same magnitude. The reason is a combination of structural factors that are specific to India and less sensitive to global monetary conditions: the enormous size and growth rate of the domestic market, which continues to expand regardless of Federal Reserve policy; the demographic tailwind of a young population entering its peak earning and consumption years; the digital infrastructure buildout that continues to create new addressable markets for technology companies; and the deepening of India's domestic investor base, which has reduced the ecosystem's dependence on global capital flows.

The decoupling is partial rather than complete. India's startup ecosystem remains connected to global capital markets through the international LPs who back India-focused VC funds, the late-stage investors who rely on global exit markets, and the global technology companies whose India investments reflect their global capital allocation decisions. When global conditions tighten significantly, Indian funding is affected — but with a lag and a diminished magnitude relative to markets with thinner domestic investor bases.

This partial decoupling is itself evidence of ecosystem maturity. The most mature innovation ecosystems — Silicon Valley in the US, Zhongguancun in China — have domestic investor bases deep and committed enough to sustain activity through global cycles. India is building this depth. The April 2026 numbers are evidence that the building has progressed further than many observers realized.

The Pipeline and What It Predicts

The investment activity of April 2026 is not an end state. It is a moment in a pipeline — a point in the process through which ideas become companies, companies become funded startups, funded startups become growth-stage businesses, and growth-stage businesses become either public companies or acquired entities that return capital and experience to the ecosystem.

Reading the pipeline forward from April 2026, the signs are encouraging. The early-stage investments being made in AI, deeptech, climate technology, and the other frontier sectors will, if they develop on the trajectories their investors expect, produce the next cohort of late-stage Indian startups in three to five years. The late-stage companies approaching IPO readiness will, in twelve to eighteen months, begin the process of listing that will return capital to investors and create a new set of liquid, experienced technology shareholders who will reinvest in the next generation.

The acquisitions and acqui-hires of the current period are building the capabilities of India's established technology companies, making them stronger competitors in global markets and more attractive acquirers for future startups. The strategic investments of global technology companies — Microsoft, Google, NVIDIA — are building the infrastructure and the talent ecosystem that will support the next wave of AI-native companies.

All of these processes are running simultaneously, feeding each other, compounding their effects. The $588 million week is a snapshot of this system in motion. The system is working. The rhythm is strong. And the stories that will be told about what India's startup ecosystem built in the 2020s are still, for the most part, being written.