Vijay Shekhar Sharma — Borrowed ₹10 for a Train Ticket, Now Runs a $5 Billion Payments Bank

The ₹10 Loan That Launched a Dream

Vijay Shekhar Sharma grew up in a small town in Uttar Pradesh. His father was a schoolteacher, his mother a homemaker. He was brilliant at math and science but restless. He enrolled in engineering at Delhi College of Engineering (now DTU) but found the curriculum too slow. In 1997, he borrowed ₹10 from a friend for a train ticket to Delhi to attend a seminar on entrepreneurship. That seminar changed his life.

He dropped out of college before finishing his degree. He started a content company called XS Communications, providing news and cricket scores to mobile phones via SMS. This was before smartphones, before the internet, before anything digital. He struggled for years, sleeping on office floors, missing meals, and being humiliated by investors who laughed at him.

But he kept going. In 2010, he noticed that mobile phones were becoming cheaper and internet access was spreading. He pivoted to mobile payments, launching Paytm (Pay Through Mobile) as a digital wallet for recharges and bill payments. The timing was perfect. India was about to explode into a digital revolution.

The Demonetisation Moment

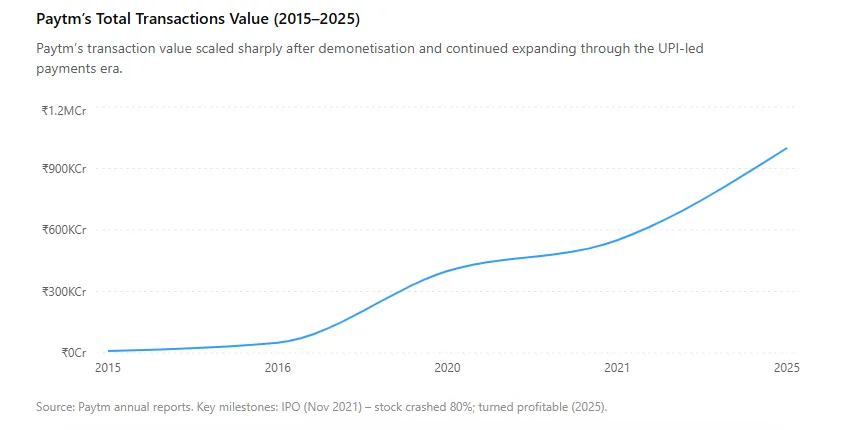

On November 8, 2016, Prime Minister Narendra Modi announced demonetisation, invalidating 86% of India’s currency overnight. People stood in long queues outside banks to exchange old notes. Digital payments became the only option. Paytm was ready.

Vijay appeared on national television, telling people to download Paytm and pay with their phones. Within weeks, Paytm’s app downloads went from 10 million to 100 million. The company processed billions of rupees in transactions. Vijay became the face of India’s cashless revolution.

Investors rushed in. Paytm raised money from Alibaba (Jack Ma’s group), SoftBank, and Berkshire Hathaway (Warren Buffett’s company). At its peak, Paytm was valued at $16 billion. Vijay’s personal stake made him a billionaire many times over.

The Banking License and Expansion

Vijay applied for a payments bank license from the RBI. In 2017, Paytm Payments Bank was launched, allowing users to open savings accounts and earn interest on their wallet balances. It was a game-changer: for the first time, millions of Indians without formal bank accounts could hold digital money safely.

Paytm also expanded into e-commerce (Paytm Mall), travel booking, movie ticketing, and wealth management. Vijay’s vision was to make Paytm the “super app” for all financial needs. But not everything worked. Paytm Mall burned cash and was eventually shut down. The payments bank faced regulatory scrutiny for data sharing issues.

The IPO Disaster

In November 2021, Paytm went public in India’s largest-ever IPO, raising ₹18,300 crore (about $2.5 billion). The hype was immense. But on listing day, the stock crashed 27% – the worst debut for a major IPO in Indian history. Over the next year, it fell further, dropping to 80% below the issue price.

What went wrong? Investors worried about:

Huge losses: Paytm was losing ₹3,000 crore a year.

Regulatory risks: The RBI had imposed restrictions on Paytm Payments Bank for onboarding new customers.

Competition: Google Pay, PhonePe, and Amazon Pay were eating Paytm’s market share in UPI payments.

Poor corporate governance: Vijay was seen as a founder with too much control and not enough oversight.

Vijay faced humiliation again. Critics called him a “one-trick pony” who had failed to build a profitable business. Paytm’s valuation dropped from $16 billion to under $3 billion.

The Turnaround

Instead of giving up, Vijay went into survival mode. He cut costs, shut unprofitable businesses, and refocused on core payments and lending. Paytm introduced small-ticket loans (₹5,000–₹50,000) to merchants and consumers, which became profitable. By 2025, Paytm had turned a net profit for the first time.

The stock has recovered partially, but not to IPO levels. Vijay’s personal wealth is a fraction of what it was, but he remains determined. In a rare interview in 2025, he said: “I’ve been counted out many times. I’m still here.”

Leadership Philosophy: Relentless Optimism

Vijay is known for his sheer grit. He works 18-hour days, sleeps in his office, and personally reviews customer complaints. He is also a showman – he once rode a horse to a company event to make a point about “charging ahead.” His optimism is infectious but can cross into overconfidence, as the IPO proved.

He has also been criticized for being a poor manager. Many senior executives have left Paytm, citing his micromanagement and abrupt decisions. But he has kept the company going through multiple crises.

Challenges and Critiques

IPO disaster: The stock crash burned thousands of retail investors who trusted Vijay’s vision.

Regulatory battles: Paytm Payments Bank has faced multiple RBI restrictions. Vijay’s confrontational style with regulators hasn’t helped.

Competition: UPI is now dominated by Google Pay and PhonePe. Paytm’s market share has fallen from 80% in 2016 to under 15% in 2025.

Profitability: Despite the turnaround, Paytm’s margins are thin, and lending is risky in an economic downturn.