The UPI Express: How India’s Payment Rail Became Faster Than Visa (And What America Can Learn)

The most disruptive financial technology in the world today doesn't live in Silicon Valley. It doesn't carry a Visa or Mastercard logo. And its headquarters aren't in New York or London, but in Mumbai.

That technology is UPI—the Unified Payments Interface, a public digital infrastructure that has quietly reshaped how over a billion people transact, and now threatens to reshape global finance itself.

In May 2026, UPI processed a staggering ₹29.90 lakh crore (approximately $36 billion) in transactions, comprising over 23.2 billion individual transactions, fueled largely by summer travel, IPL spending, and seasonal consumption. This represents a year-on-year growth of 19% in value and 24% in volume, underscoring strong organic demand and a maturing digital payment ecosystem. Just as impressively, UPI is now within striking distance of overtaking Visa in daily transaction volumes.

This is the story of how a state-backed initiative from a developing economy built a payment rail that is faster, cheaper, and more inclusive than anything the Western private sector has produced. It is a story with profound lessons for global fintech, and for any nation seeking to build the digital public goods of the 21st century.

The Billion-Person Habit

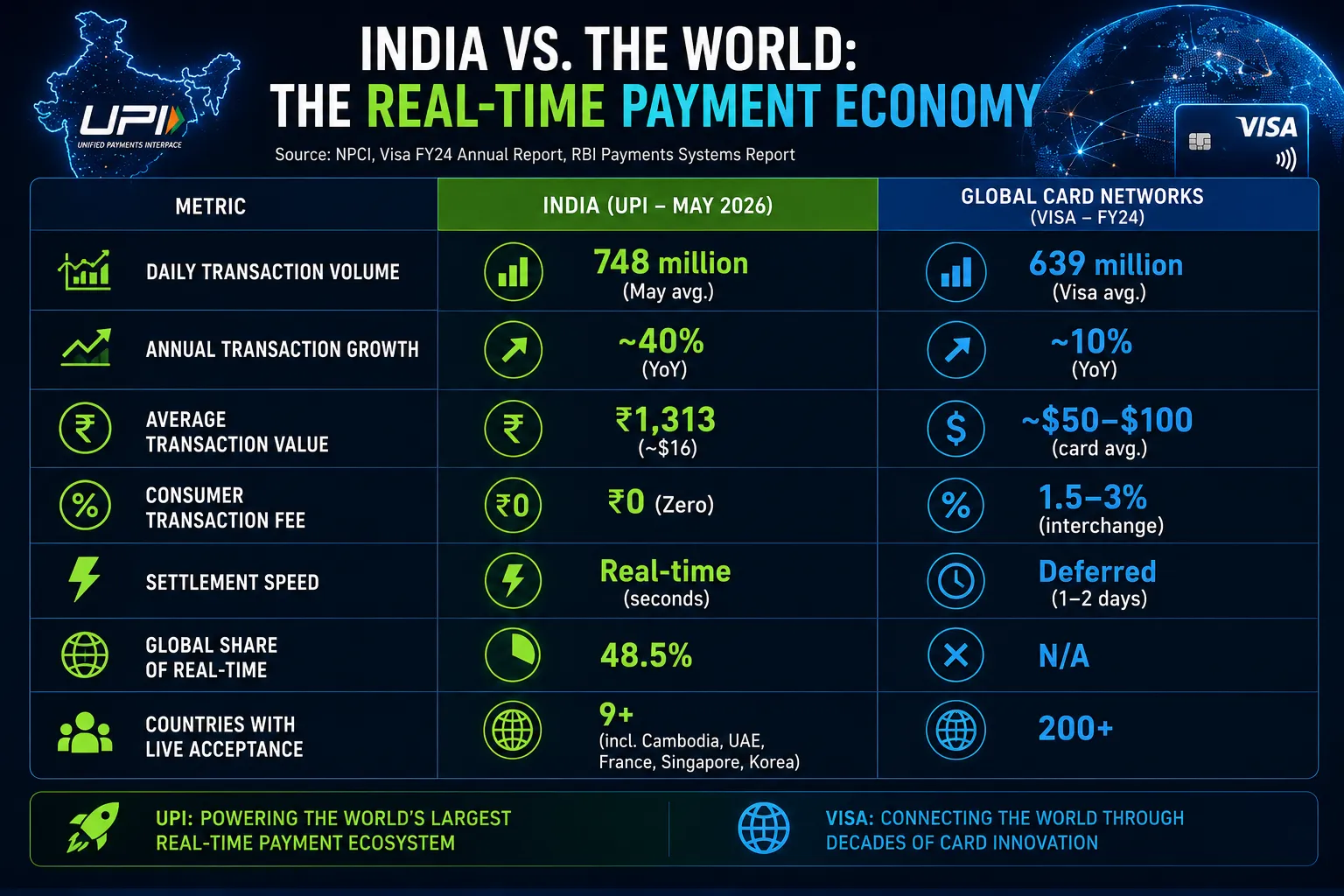

To truly appreciate UPI, one must understand its scale. In a single day in May, the system handled an average of 748 million transactions with a total value exceeding ₹96,000 crore. In April, 713 banks were live on the platform. The ecosystem continues to be dominated by PhonePe and Google Pay, which together command more than 80% of the market by volume.

But the most telling statistic might be the declining average ticket size, which has fallen from ₹1,848 in 2021 to ₹1,313 in 2025. This isn't a sign of weakness—it's a sign of maturity. As Cashfree Payments CEO Akash Sinha notes, “This is not a concern; it is a sign of a maturing ecosystem. High-value transactions are increasingly being handled by credit cards, whose transaction value has grown from ₹8.9 lakh crore in 2021 to ₹23.2 lakh crore in 2025. UPI, meanwhile, has become the default rails for India’s everyday economy, including payments to local merchants, transit and quick commerce”.

The Cost of Free

Why have Indians moved so rapidly to UPI? The answer is simple: it's almost free. For consumers, UPI carries zero transaction fees. For merchants, fees are negligible, especially when compared to the burdensome interchange fees of card networks. In the US and Europe, card networks have built extraordinarily profitable businesses extracting 1.5% to 3% from every transaction. UPI has effectively made that model unsustainable in its home market.

This is not merely a competition for market share; it is a competition of operating systems. India has bet on a model where payments are a public good, facilitated by a state-owned corporation (NPCI) that collaborates with private players like PhonePe and Google Pay. The US has largely left payments to private card networks.

The results are stark. While Visa grew at approximately 10% annually, UPI surged by a staggering 40% last year. At its current growth trajectory, UPI is not just catching Visa; it is poised to leave it behind.

The Second Act of UPI: Credit

If the first act of UPI was about replacing cash, the second act is about replacing credit cards. The Reserve Bank of India has permitted the introduction of the Credit Line on UPI (CLOU). This allows banks to extend pre-sanctioned credit lines directly through UPI applications.

Fintechs are already moving aggressively. BharatPe launched a new product, BharatPe Flex, in partnership with YES Bank in June 2026, offering eligible users up to 45 days of interest-free credit on purchases via UPI, with fully digital onboarding. This product allows users to make payments at millions of merchants for everyday transactions without directly debiting their bank accounts. The behavioural shift is profound: credit is no longer a separate product with its own friction—it's simply another payment option in the familiar QR flow.

Early data shows CLOU products have achieved Non-Performing Asset (NPA) rates under 2% for standard small-ticket credit usage, and acquisition costs that are nearly one-fifth of traditional credit cards. Small Finance Banks (SFBs) have emerged as the earliest and most aggressive adopters, reaching “new-to-credit” users and low-income households that traditional credit cards have bypassed.

The Global Unbundling

UPI's ambitions, however, extend far beyond India’s borders. The NPCI's international arm is methodically weaving a global network of QR-based payments. In June 2026, UPI went live in Cambodia through a linkage with its KHQR system, giving Indian travellers access to over 4.5 million merchant touchpoints. In February 2026, the NPCI signed an agreement with Malaysia's PayNet to link UPI with DuitNow QR, enabling seamless payments for millions of tourists and fostering two-way economic activity. The linkage will give Indian travellers access to over 2.9 million DuitNow QR merchants across Malaysia.

Beyond Asia, UPI is now accepted for merchant payments in Bhutan, France, Mauritius, Nepal, Qatar, Singapore, Sri Lanka, and the UAE. Agreements have been signed to take UPI live in Israel and South Korea, with South Korea alone welcoming nearly 200,000 Indian travellers in 2025.

Yet the most audacious expansion involves not just acceptance but emulation. NIPL has signed deals with the central banks of Peru and Namibia to help them build real-time payment systems based on the UPI blueprint. Brazil and Namibia are expected to launch their systems by late 2026 or early 2027. Trinidad and Tobago is also developing UPI-like digital payments infrastructure with NIPL's assistance. This marks a historic reversal of financial technology flows: a developing nation is now exporting its public digital infrastructure to other countries and continents.

The Next Frontier

The pace of innovation shows no signs of slowing. NPCI is actively developing multiple frontiers to expand UPI's reach:

Voice Payments: NPCI is deepening AI integration across India's payments stack, from agentic interfaces and conversational payments to domain-specific LLMs designed to streamline disputes. Voice is emerging as the next interface for financial inclusion.

Interoperable Soundboxes: NPCI is rolling out a unified, interoperable Soundbox system that will allow merchants to accept UPI payments from any QR code—PhonePe, BharatPe, Paytm—using a single device, dramatically reducing costs for small businesses.

UPI Circle: This groundbreaking feature allows users to delegate payment rights to up to five trusted individuals, with real-time transaction oversight via UPI PIN. It is now available across major apps including BHIM, PhonePe, and Google Pay, enabling families to share financial access securely. A primary user can set monthly limits (capped at ₹15,000) and durations from one month to five years, controlling the process without sharing sensitive information.

What America Can Learn

So, what can the United States—home of Silicon Valley, PayPal, and the world's most sophisticated card networks—learn from a technology born in Mumbai?

First, interoperability is destiny. One of the greatest achievements of UPI is that anyone with a bank account can transact with anyone else, regardless of their chosen app. The US's fragmented banking system, lack of a real-time settlement layer, and proprietary network silos appear increasingly antiquated.

Second, the state can be a good architect of infrastructure. UPI was not a market invention; it was a policy invention. The RBI and NPCI built the rails and invited private innovation on top of them.

Third, price drives adoption. The zero-cost model for consumers was not an accident; it was a strategic choice to onboard a billion users. By eliminating friction, UPI created a network effect that is now self-sustaining.

Finally, real-time is the only speed that matters. While the US debates instant settlement, India processes nearly half of the world's real-time transactions, making cashless payments a seamless reality for hundreds of millions. The next decade of global finance will not be decided in boardrooms of card networks, but in the feedback loops of public infrastructure that prioritizes inclusion over intermediation. And that is a race India is already winning.

Chart: "India vs. The World: The Real-Time Payment Economy"

Source: NPCI, Visa FY24 Annual Report, RBI Payments Systems Report

Metric | India (UPI - May 2026) | Global Card Networks (Visa - FY24) |

|---|---|---|

Daily Transaction Volume | 748 million (May avg.) | 639 million (Visa avg.) |

Annual Transaction Growth | ~40% (YoY) | ~10% (YoY) |

Average Transaction Value | ₹1,313 (~$16) | ~$50–$100 (card avg.) |

Consumer Transaction Fee | ₹0 (Zero) | 1.5–3% (interchange) |

Settlement Speed | Real-time (seconds) | Deferred (1–2 days) |

Global Share of Real-Time | 48.5% | N/A |

Countries with Live Acceptance | 9+ (incl. Cambodia, UAE, France, Singapore, Korea) | 200+ |