The Phoenix Rises: How upGrad, PhysicsWallah and AI Are Rebuilding Indian Edtech from the Ashes

The $22 Billion Implosion That Forced a Reckoning

In 2021, BYJU'S was the uncontested king of Indian edtech. Valued at $22 billion, backed by Tiger Global, Chan Zuckerberg Initiative, and Naspers, it was the most valuable startup in the country. The message to the world was clear: India was going to revolutionise education through technology, and BYJU'S would lead the charge.

By 2024, the king had no clothes. A collapsed merger with Aakash Educational Services, delayed financial audits, and a crushing debt burden of over $1.2 billion forced BYJU'S into insolvency proceedings. The parent company, Think & Learn, is now fighting to retain control while its US lenders battle over subsidiary Bond. The valuation has effectively evaporated. The once‑indomitable edtech giant is a cautionary tale.

But the phoenix rises from ashes, not from the flames alone. In the two years since the edtech funding winter began, a new ecosystem has emerged — leaner, more capital‑efficient, and finally profitable. In May 2026, upGrad announced an all‑stock acquisition of Unacademy valued at $218 million, consolidating two of the remaining giants. PhysicsWallah filed its draft red herring prospectus for an IPO. Vedantu and Classplus have pivoted to profitability. And across the sector, AI is being deployed not as a buzzword but as a genuine tool to reduce costs and personalise learning.

The Indian edtech sector raised just $249 million in 2025, down from a peak of over $4 billion in 2021. Funding fell by 56% year‑on‑year in 2025. That is a breathtaking contraction. But the startups that survived the bloodbath are now demonstrating something that the 2021 era never did: real, sustainable unit economics.

The Consolidation: upGrad + Unacademy = $218 Million All‑Stock Deal

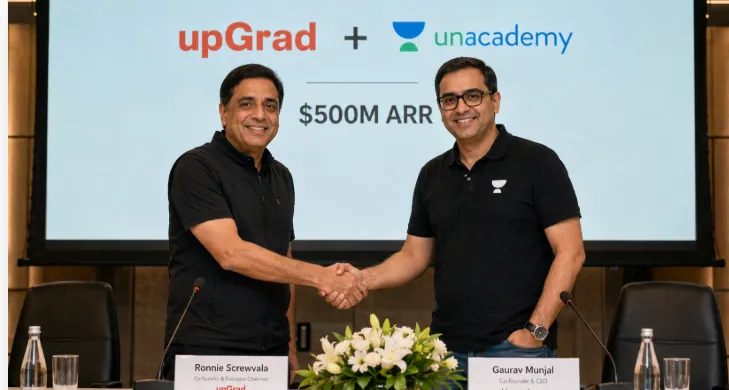

The biggest signal of the new edtech order came in May 2026. upGrad, the Ronnie Screwvala‑led higher education and upskilling platform, announced it would acquire Unacademy, the test‑prep and learning platform once valued at $3.4 billion, for $218 million in an all‑stock deal.

The numbers are stark. Unacademy's peak valuation of $3.4 billion, achieved in its $440 million Series H round led by Temasek, was one of the highest in Indian startup history. The $218 million acquisition price represents a decline of approximately 90% from that peak. But in the context of the post‑crash edtech landscape, the deal is seen as a smart, strategic merger that combines upGrad's strength in working professionals with Unacademy's reach in K‑12 and test preparation.

The combined entity will have an estimated annual recurring revenue of over $500 million, a user base exceeding 100 million registered learners, and a presence in over 50 cities across India. Importantly, both companies had cut their cash burn dramatically over the previous 18 months, with upGrad turning profitable and Unacademy approaching break‑even.

Ronnie Screwvala, reflecting on the acquisition, said: “The edtech winter is over. The survivors have emerged stronger, leaner, and more focused on unit economics than ever before. This merger is not about size — it is about creating a sustainable, profitable education platform for the next decade.”

Gaurav Munjal, Co‑founder and CEO of Unacademy, added: “When we started, we dreamed of democratising education. That dream is bigger than any valuation. upGrad gives us the scale and stability to return to our core mission without the distraction of fundraising.”

The combined entity is expected to pursue a public listing within 24‑36 months, likely in India, bypassing the SPAC route that many edtechs attempted during the boom years.

PULL QUOTE #2 “When we started, we dreamed of democratising education. That dream is bigger than any valuation.” — Gaurav Munjal, Co‑founder and CEO, Unacademy, May 2026

PhysicsWallah: The IPO‑Bound Profit Machine

If upGrad and Unacademy represent consolidation, PhysicsWallah (PW) represents the opposite: organic, profitable growth without the hype.

In April 2026, the Noida‑based test‑prep unicorn filed its draft red herring prospectus (DRHP) with SEBI, proposing an initial public offering comprising a fresh issue of shares worth ₹1,250 crore (approximately $150 million) and an offer‑for‑sale of up to 80 million equity shares by existing shareholders.

The financials are remarkable. For the nine months ending December 2025, PW reported:

Revenue from operations: ₹1,424 crore

Profit after tax: ₹113 crore

EBITDA margin: 18%

Run‑rating those numbers suggests annual revenue approaching ₹1,900 crore ($230 million) and annual profit over ₹150 crore ($18 million) — making PW one of the few profitable edtech unicorns globally.

PW's journey is the stuff of Indian startup legend. Founded by Alakh Pandey, a former physics teacher, the company began as a YouTube channel offering free coaching for JEE and NEET aspirants. The pivot to a paid subscription model (PW App, PW Vidyapeeth offline centres) was executed with surgical precision. Unlike BYJU'S, which spent billions on celebrity endorsements and aggressive sales, PW grew through word of mouth, teacher‑led instruction, and an obsessive focus on student outcomes.

The company's offline‑online hybrid model is particularly notable. PW now operates over 200 Vidyapeeth offline centres across 150 cities, with a gross merchandise value of ₹1,000 crore in FY25 — nearly half its total revenue. This hybrid approach provides a natural hedge against the volatility of pure‑play online learning.

The IPO is expected to value PW at $2‑2.5 billion, lower than its post‑Series B peak of $3 billion but reflective of the current market's preference for profitable businesses over high‑growth loss‑makers.

Vedantu and Classplus: The Profitable Pivots

Even players that were once bleeding cash have found their footing.

Vedantu, a live tutoring platform, restructured aggressively in 2024‑2025, cutting its workforce by over 60% and pivoting from 1:1 live classes to a more scalable group‑class model. In 2025, Vedantu turned EBITDA‑positive for the first time, with revenue crossing ₹300 crore. The company is not yet profitable at the PAT level but is widely expected to be so by the end of FY26.

Classplus, a B2B platform that digitises coaching centres, raised $55 million in 2024 and has since grown to serve over 100,000 educators across 1,500 cities. The company is reported to be operationally profitable and is exploring a public listing in 2027.

The AI Inflection: How Artificial Intelligence Is Reshaping Edtech

The most profound change in edtech, however, is not consolidation or profitability — it is artificial intelligence.

During the boom years, AI was a marketing buzzword. Today, it is a genuine lever for cost reduction and personalisation.

AI‑powered tutoring assistants are enabling platforms to reduce reliance on expensive human tutors. PhysicsWallah has deployed an AI bot that answers basic JEE and NEET questions with 85% accuracy, freeing up human teachers for more complex queries. upGrad uses AI to grade coding assignments instantly, reducing turnaround time from days to minutes.

Personalised learning paths are finally becoming real. Instead of a one‑size‑fits‑all curriculum, AI systems analyse a student's performance in real time and adjust the difficulty, pacing, and topic focus dynamically. This was the promise of edtech in 2021; it is the reality of edtech in 2026.

Automated content generation is another frontier. Generative AI tools can now create practice questions, video scripts, and even complete lesson plans in multiple languages. For a country like India, with 22 official languages and a massive shortage of quality teachers, this is a game‑changer.

The India EdTech Market, valued at approximately USD 6.9 billion in 2025, is projected to reach USD 12.8 billion by 2031, growing at a CAGR of 10.85%. AI‑driven platforms are expected to capture the fastest‑growing segment.

The Structural Shift: From Growth‑at‑Any‑Cost to Profitability‑First

The most important lesson of the BYJU'S collapse has been cultural. Investors, founders, and even employees now prioritise unit economics over vanity metrics.

In 2021, the typical edtech sales pitch was: “We are growing 3X year‑on‑year; ignore the losses.” In 2026, the pitch has flipped: “We are profitable, with a 20% EBITDA margin and a net revenue retention of 120%.”

This shift has had three tangible effects:

Reduced cash burn: Most surviving edtechs have cut their monthly burn from tens of crores to near zero.

Longer runways: Even profitable startups are raising smaller, more efficient rounds to fund specific expansions rather than indefinite growth.

Realistic valuations: The $22 billion unicorn is dead; long live the $500‑800 million profitable centaur.

The Global Indian Takeaway

For the diaspora, the post‑crash edtech landscape offers three distinct opportunities.

First, invest in the IPO pipeline. PhysicsWallah's ₹1,250 crore IPO is the most anticipated. upGrad (post‑Unacademy merger) will likely list in 24‑36 months. Early access to these offers (via anchor or pre‑IPO placements) could generate significant returns.

Second, partner for cross‑border expansion. Indian edtechs are now eyeing international markets — PhysicsWallah in the Middle East, upGrad in Southeast Asia. Diaspora professionals with education distribution networks can become local partners.

Third, acquire distressed assets at a discount. The BYJU'S insolvency has left a trail of under‑monetised brands (Osmo, WhiteHat Jr, Aakash) that may be sold piecemeal. A diaspora consortium could acquire these assets at a fraction of their peak cost and relaunch them with a leaner model.

The Final Word

The BYJU'S implosion was painful. Thousands of employees lost jobs. Billions in investor capital were wiped out. The founders went from heroes to cautionary tales.

But out of that wreckage, a healthier edtech ecosystem has emerged. The survivors — upGrad, PhysicsWallah, Vedantu, Classplus — have learned the most valuable lesson in business: growth without unit economics is not growth; it is debt.

With upGrad and Unacademy merging, PhysicsWallah filing for an IPO, AI reducing costs, and the entire sector pivoting to profitability, Indian edtech is not merely recovering — it is rebuilding on a sustainable foundation.

The phoenix has risen. And this time, it is fireproof.

CHART: “Indian Edtech: Fall and (Potential) Rise – At a Glance (2026)”

Metric | Data | Source |

|---|---|---|

BYJU'S peak valuation (2021) | $22 billion | Various |

BYJU'S current status | Insolvency proceedings | NCLT |

Indian edtech peak annual funding (2021) | $4 billion+ | Inc42 / Tracxn |

Indian edtech funding 2025 | $249 million (‑56% YoY) | Inc42 |

upGrad + Unacademy deal value | $218 million (all‑stock) | Inc42, May 2026 |

Unacademy peak valuation | $3.4 billion (2021) | YourStory |

Unacademy valuation decline | ~90% from peak | Calculated |

Combined entity ARR | $500 million+ | upGrad/Unacademy statement |

PhysicsWallah DRHP fresh issue | ₹1,250 crore ($150M) | DRHP filing |

PW 9‑month revenue (Dec 2025) | ₹1,424 crore | DRHP |

PW 9‑month profit (Dec 2025) | ₹113 crore | DRHP |

PW run‑rate annual profit | ₹150 crore+ ($18M) | Calculated |

PW offline centres | 200+ Vidyapeeth centres, 150 cities | Inc42 |

PW offline GMV (FY25) | ₹1,000 crore | Inc42 |

PW IPO target valuation | $2‑2.5 billion | Industry estimates |

India EdTech market (2025 → 2031) | $6.9B → $12.8B (10.85% CAGR) | Industry reports |

Classplus educators served | 100,000+ across 1,500 cities | Company data |

Vedantu EBITDA‑positive (2025) | Yes (first time) | Inc42 |