The K‑Drama Invasion: Korean Content Now Commands 12% of Indian Streaming Hours—And Bollywood Never Saw It Coming

MUMBAI — May 30, 2026 — In 2019, a Korean‑language romantic drama called Crash Landing on You was released on Netflix to a global audience that was, at the time, primarily Asian and diasporic. It was subtitled in over 30 languages, but it was not expected to travel well in India—a market that had, for decades, been defined by the dominance of local‑language content, by the cultural primacy of Bollywood, and by an audience that was assumed to be resistant to foreign‑language entertainment. The assumption was wrong. Crash Landing on You became the most‑watched international series on Netflix in India in 2020, and it launched a wave of Korean‑content consumption that has, in the six years since, reshaped the Indian streaming landscape. By Q1 2026, Korean content—dramas, films, reality shows—accounted for approximately 12 percent of all streaming hours consumed in India, a figure that is larger than the combined share of all other non‑Indian content. The K‑drama, which was once a niche enthusiasm for a small, digitally connected audience, has become a mainstream cultural force—and Bollywood, which spent the past decade worrying about Hollywood, has discovered that the real competition was coming from Seoul.

The Licensing Economics

The most powerful force driving the K‑drama invasion is not cultural. It is economic. A Korean drama is dramatically cheaper for an Indian streaming platform to license than an Indian original series is to produce. The average licensing cost for a top‑tier Korean drama—a 16‑episode season of a series that has already aired in Korea and demonstrated its audience appeal—is between ₹8 crore and ₹15 crore, including subtitling and dubbing into major Indian languages. The average production cost of a comparable Indian original series—a star‑driven, high‑production‑value drama produced for Netflix or Amazon—is between ₹40 crore and ₹80 crore. The Korean drama delivers comparable engagement at a fraction of the cost, and the streaming platforms that are investing most aggressively in Korean content are the ones that are generating the highest returns on their content budgets.

The licensing economics are particularly compelling for the global platforms—Netflix and Amazon Prime Video—that have been struggling to compete with JioHotstar in the Indian market. The global platform that cannot match JioHotstar's content budget, its subscriber base, or its ecosystem integration can still compete on curation—by offering the Indian audience a selection of international content that is not available on the domestic platform. The Korean drama, which has a proven global appeal and a passionate fan base in every major market, is the most valuable category of international content for the global platforms—a way of differentiating their service from the domestic competition without the enormous capital commitment that Indian original production requires.

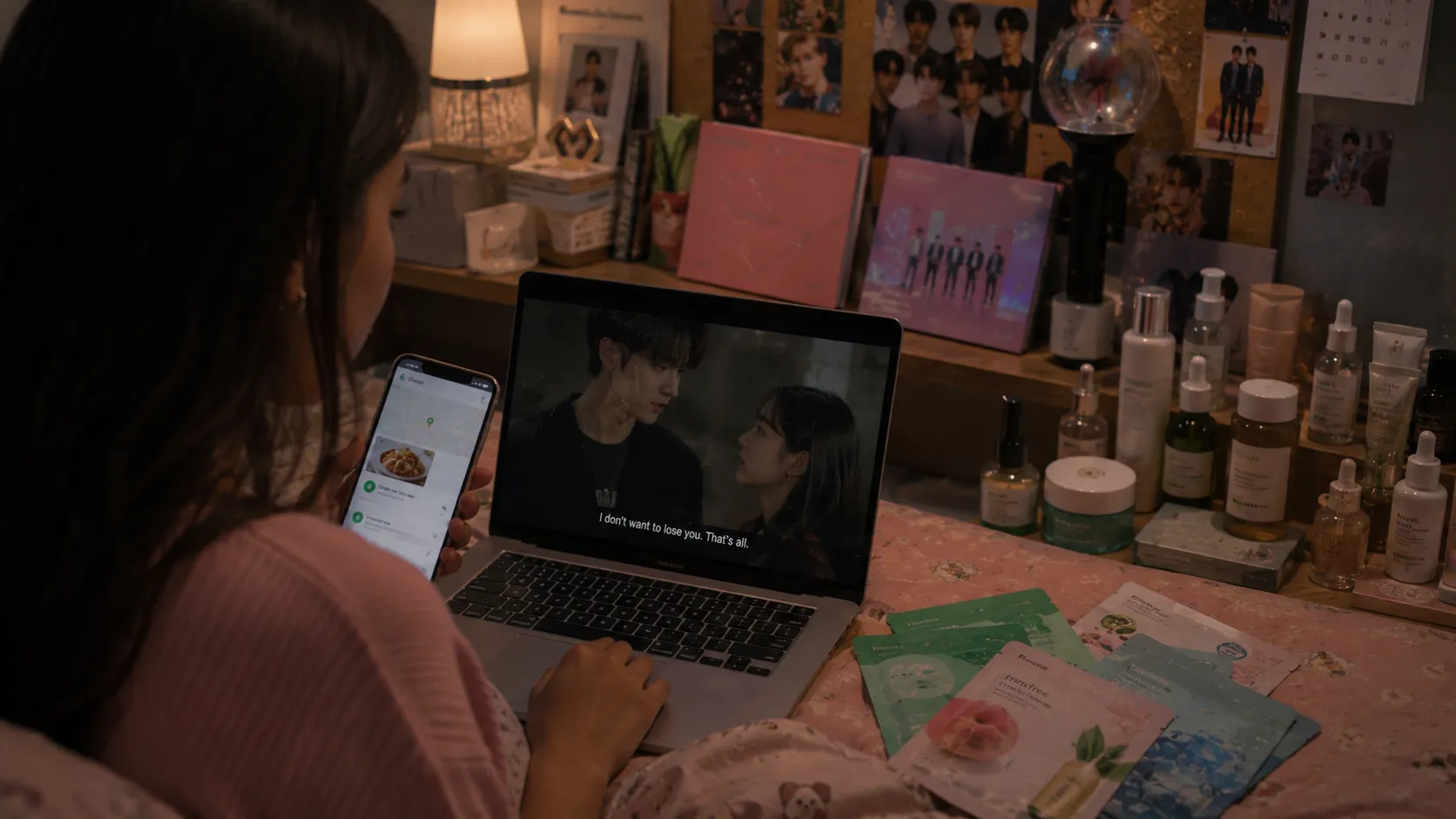

The dubbing revolution has accelerated the K‑drama takeover. The AI‑powered dubbing tools that have transformed the Indian regional‑cinema market are now being applied to Korean content, allowing the platforms to offer Hindi, Tamil, and Telugu dubbed versions of Korean dramas at a cost that is a fraction of what human dubbing would require. The audience that was once limited to the subset of Indian viewers who were comfortable reading English subtitles is now being exposed to Korean content in their own languages—and the engagement data suggests that the dubbed versions are performing significantly better than the subtitled originals. The language barrier, which was supposed to protect the Indian market from foreign competition, is being dismantled by the same technology that is dismantling the language barriers between Indian states. The K‑drama that is dubbed into Hindi is, for the Indian viewer, no more foreign than a Bollywood film—and it is often cheaper, and more engaging, than the domestic alternative.

The Demographic Surge

The K‑drama audience in India is disproportionately young, female, and urban—a demographic that is among the most valuable in the advertising market, and that has been underserved by the Indian entertainment industry for decades. The Bollywood film, with its emphasis on male stars, action spectacle, and mass‑audience appeal, has historically treated the young‑female audience as a secondary concern. The Indian television industry, with its long‑running soap operas and its conservative cultural framing, has served the female audience but not engaged it with the same intensity that the best international content commands. The K‑drama, by contrast, is built for the female gaze—the romantic narratives, the emotionally expressive male leads, the emphasis on relationships over spectacle. The audience that was hungry for this kind of content, and that was not getting it from the domestic industry, has migrated to the international platforms—and the platforms are responding by acquiring more of the content that the audience wants.

The demographic surge is visible in the data. A 2026 survey of Indian streaming‑platform users found that Korean content accounted for approximately 18 percent of viewing hours among women aged 18 to 34—the highest share of any non‑Indian content category—and that the figure was growing at a compound annual rate of approximately 40 percent. The same survey found that Korean‑content viewers were significantly more likely than the average streaming‑platform user to be paid subscribers, to engage with the platform daily, and to recommend the platform to friends. The K‑drama audience is not merely large. It is loyal, engaged, and commercially valuable—and the platforms that are investing in Korean content are capturing a disproportionate share of that audience's attention and spending.

The cultural impact of the K‑drama invasion extends well beyond the streaming platforms. The Indian beauty and fashion industries have been reshaped by Korean aesthetics—the "glass skin" skincare trend, the K‑pop‑influenced streetwear, the growing market for Korean cosmetics and personal‑care products. The Indian travel industry has seen a surge in tourism to South Korea, driven by fans who want to visit the locations where their favourite dramas were filmed. The Indian food industry has seen the proliferation of Korean restaurants, Korean grocery products, and the home‑cooking trend sparked by the food‑centric narratives of many Korean dramas. The K‑drama is not merely a content category. It is a cultural export engine—a way of projecting Korean soft power into the Indian market, and of creating a consumer base for Korean products that extends well beyond the screen.

The Bollywood Response

Bollywood's response to the K‑drama invasion has been, so far, a mixture of denial and adaptation. The denial is familiar: the argument that Indian content is culturally specific, that the Indian audience will always prefer stories in its own languages, that the K‑drama fad will pass. The adaptation is more interesting, and it is happening primarily at the level of the streaming platforms, which are commissioning Indian original series that borrow the narrative structures, the aesthetic sensibilities, and the demographic targeting of Korean dramas. The Netflix original Heeramandi—a period drama with a female‑centric narrative, a visually opulent aesthetic, and a focus on relationships over action—was, in its conception, an attempt to create an Indian equivalent of the Korean historical drama. The Amazon original The Married Woman—a slow‑burn romance between two women, set against a backdrop of social conservatism—was similarly influenced by the Korean model. The Indian streaming industry is learning from the K‑drama, even as the Bollywood theatrical industry continues to dismiss it.

The Bollywood theatrical industry's response has been constrained by the structural limitations of the theatrical format. The K‑drama is a serialised, long‑form narrative that is designed for binge‑watching—a format that the theatrical film, with its two‑hour running time and its single‑release cadence, cannot match. The audience that has become accustomed to the emotional depth, the character development, and the narrative complexity of a 16‑hour Korean drama is an audience that may find the conventional Bollywood film unsatisfying—not because the film is bad, but because the format cannot deliver the experience that the audience has learned to expect. The Bollywood studios that are investing in streaming‑platform originals—the Dharma‑Netflix deal, the YRF‑Amazon partnership—are adapting to the format shift. The studios that are still focused exclusively on theatrical production are betting that the audience will return to the cinema once the K‑drama fad passes. The bet is not irrational, but it is risky—because the evidence, so far, suggests that the fad is not a fad. It is a structural shift in consumption, and the audience that has migrated to Korean content is not coming back.

The Global Streaming Chessboard

The K‑drama invasion is not an Indian story. It is a global one, and its implications extend well beyond the Indian market. Netflix, which has invested over $2.5 billion in Korean content over the past five years, has used K‑dramas as a spearhead for its international expansion strategy—a content category that travels across linguistic and cultural boundaries with an ease that no other non‑English content can match. The platform's global top‑10 lists are, in most weeks, dominated by Korean titles—a dominance that reflects not just the size of the Korean‑content audience, but the intensity of its engagement. The K‑drama fan is not a passive consumer. They are an evangelist—someone who recommends the content to friends, who participates in online fan communities, who generates the social‑media buzz that drives the platform's recommendation algorithms. The K‑drama is the most viral content category in the world, and the platform that controls the best Korean content controls the most powerful engine of audience growth in the global streaming market.

The global chessboard is also being reshaped by the entry of the Korean studios themselves into the international market. The major Korean production companies—CJ ENM, JTBC Studios, Studio Dragon—have been building their own direct‑to‑consumer streaming platforms, their own international distribution networks, and their own relationships with the global platforms that license their content. The Korean studios are no longer merely suppliers of content to Netflix and Amazon. They are becoming competitors—platforms that are building their own relationships with the global audience, and that are increasingly reluctant to license their most valuable content to the platforms that are competing with them for that audience. The global streaming chessboard is becoming more complex, more competitive, and more Korean‑centric—and the Indian platforms that are not investing in Korean content are the ones that will be left behind as the chessboard shifts.

What This Signals

The K‑drama invasion is not primarily a story about Korean content. It is a story about the structural transformation of the Indian media industry—a shift from a market that was defined by the primacy of local‑language content to a market that is increasingly integrated into the global content economy, from an audience that was assumed to be resistant to foreign‑language entertainment to an audience that is actively seeking it, and from a competitive landscape that was dominated by Bollywood to a competitive landscape in which Bollywood is competing not just with Hollywood, but with every content‑producing country on Earth. The K‑drama is the leading edge of that transformation—the first foreign‑language content category to achieve mainstream scale in the Indian market. It will not be the last. The Spanish, Turkish, Japanese, and Thai content industries are all watching the K‑drama invasion, and they are preparing their own entries into the Indian market. The Indian streaming audience is being integrated into the global content economy, and the integration is irreversible. Bollywood never saw it coming. It should have.