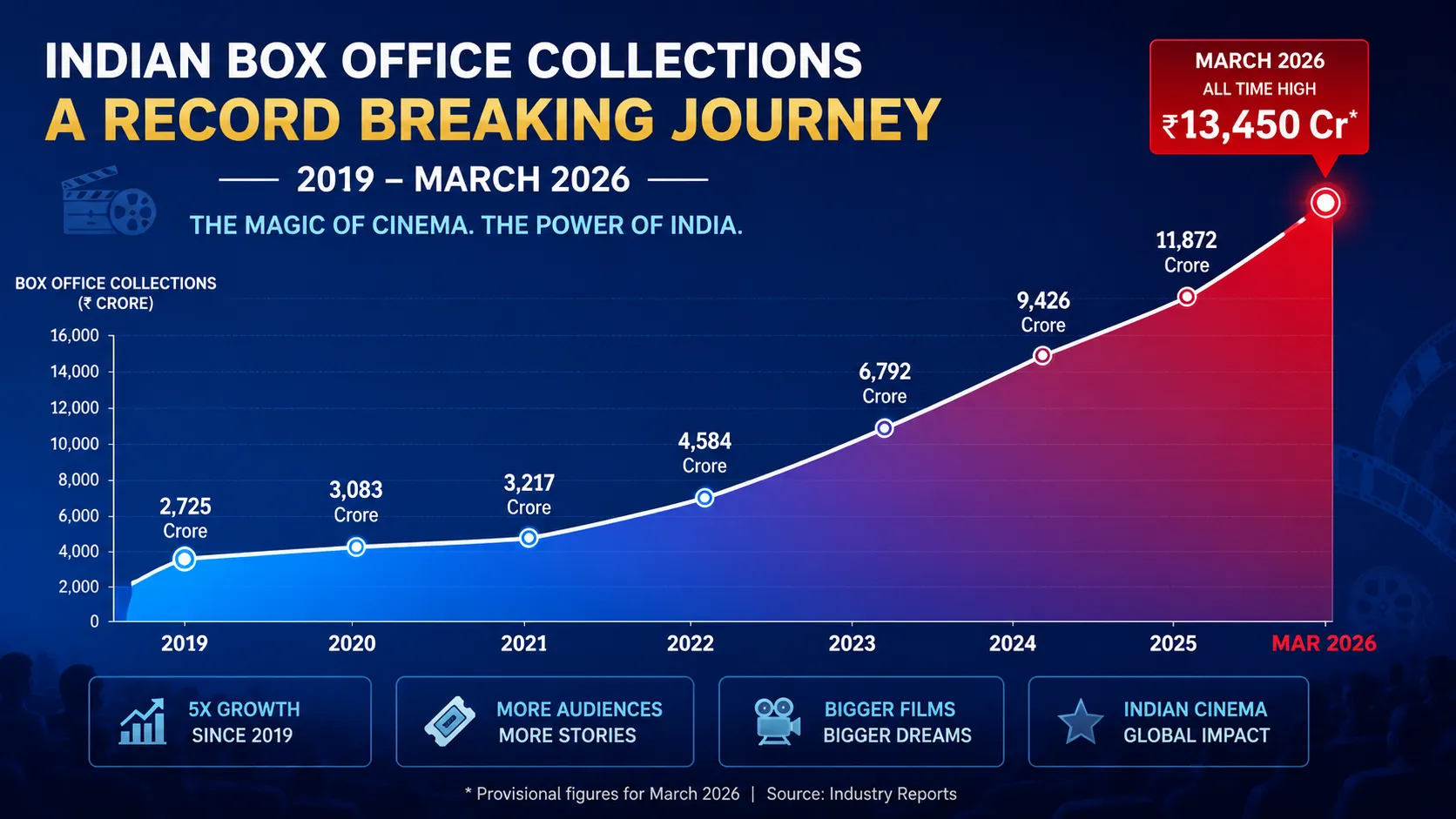

After years of pandemic pain, OTT panic, and doomsday predictions, India's box office is roaring back. March 2026 grossed ₹1,690 crore — the highest single month ever. The party isn't over. It's just getting started.

Two years ago, the consensus was that Indian cinema was dying. Streaming had killed the theatre habit. Production houses were slashing budgets. Multiplex chains were trading at all‑time lows. Film critics wrote obituaries for the big‑screen experience. Then something unexpected happened. Audiences came back. Not tentatively, not cautiously, but in waves so large that March 2026 grossed ₹1,690 crore at the domestic box office — the highest single month in Indian cinema history. Bollywood collections surged 55% year‑on‑year in FY26. And the industry that was supposed to be dead is suddenly the most exciting story in Indian entertainment.

The numbers are staggering across every segment. Hindi films, once written off as irrelevant to younger audiences, have delivered back‑to‑back hits. Regional cinema — Tamil, Telugu, Malayalam, Kannada, Bengali, Marathi — is experiencing its own renaissance, with local blockbusters outperforming national releases in their home markets. The multiplex chains (PVR INOX, Cinepolis, Miraj) have reported their highest footfalls since 2019, with average ticket prices up 12% due to premium formats like IMAX and 4DX.

What changed? The answer is not simple, but three factors stand out.

First, content quality has improved dramatically. During the pandemic, when theatres were closed, producers were forced to rethink their scripts. The old formula — a big star, a foreign location, a few item songs, and a weak story — no longer worked. Streaming had exposed audiences to global content, and they demanded better. The films that succeeded in 2025 and 2026 are the ones that invested in writing, production values, and originality. The Dhurandhar franchise proved that a well‑made action drama could cross ₹3,000 crore worldwide. Mid‑budget films like Bandar and Bhay showed that you don't need a ₹200 crore budget to win.

Second, the window between theatrical and streaming has widened. During the pandemic, many films went directly to OTT or had a very short theatrical window (two to three weeks). Audiences learned to wait. In 2025, producers began extending the window to eight weeks or more, creating a sense of urgency. "If you don't see it in theatres, you'll have to wait two months" became a effective marketing message. The result: more people went to theatres, and those who waited for streaming still watched eventually — so the producers won twice.

Third, regional strength became national strength. For years, Bollywood dominated the conversation while South Indian cinema was treated as a niche. That flipped. RRR and KGF were the early signals, but the trend has continued. Tamil and Telugu films now regularly release in dubbed Hindi versions and perform well across the country. In turn, Hindi films have learned to market themselves more effectively in the South. The result is a truly national market, where a film's success is no longer limited by language.

The recovery is not uniform. Smaller films still struggle for screens. Single‑screen theatres in small towns are closing faster than multiplexes can open. The cost of production, especially for VFX‑heavy films, remains high. And the competition from streaming — while less threatening than before — has not disappeared.

But the trajectory is unmistakably upward. Analysts project that 2026 will end with domestic box office collections exceeding ₹14,000 crore, surpassing the pre‑pandemic peak of ₹12,500 crore (2019). If that happens, it will be the first time Indian cinema has fully recovered from COVID‑19 — not just in revenue, but in confidence.

The multiplex chains are investing again. PVR INOX has announced 150 new screens over the next 18 months, with a focus on tier‑2 and tier‑3 cities where cinema culture is reviving. Cinepolis is expanding its presence in South India. Miraj is retrofitting older properties with premium formats.

Production houses are also bullish. The major studios — Yash Raj, Dharma, Red Chillies, T‑Series — have announced ambitious slates for 2027 and 2028. New players, including streaming platforms that have moved into theatrical distribution, are adding to the competition. The result is a healthy, dynamic market where good films succeed and bad films fail — the way it should be.

The audience has also changed. Post‑pandemic moviegoers are more discerning. They check ratings, watch trailers multiple times, and make a conscious decision to spend ₹500‑1,000 on a ticket, snacks, and parking. They are not casual. They want an experience. That is why premium formats (IMAX, 4DX, Dolby Atmos) are growing faster than standard screens. That is why event films like Dhurandhar are breaking records.

For the industry, the lesson is clear: audiences never stopped loving cinema. They stopped loving bad cinema. Give them something worth leaving the house for, and they will come. That is what March 2026 proved. That is what the rest of 2026 will continue to prove.

The great Indian comeback is not a one‑month wonder. It is a structural shift. After years of uncertainty, fear, and doomsaying, Bollywood and its regional cousins have found their footing again. The screens are lit. The cash registers are ringing. And the only question left is: what will they show us next?