The Fastest $100M in SaaS History

Eight months. That's all it took. Mukund Jha, a founder from Bihar, launched Emergent—an AI-powered "vibe coding" platform—just eight months ago. In February 2026, the Bengaluru-and-San Francisco-based startup announced it had crossed $100 million in Annual Recurring Revenue (ARR). Not only that, it had nearly doubled this metric in the past month alone, now boasting over 5 million users across 190 countries and millions of apps built on its platform. To put that in perspective: Salesforce took seven years to hit $100M ARR. Atlassian took six. Emergent did it in eight months by letting non-technical users build full-stack apps using natural language prompts—what the industry now calls "vibe coding." No code, just AI. But Emergent is not an anomaly. It is the new face of a quietly exploding sector. According to the JM Financial report released in July 2025, India's SaaS sector had already crossed $15 billion in annual revenue in FY24, with more than 36 companies topping $100 million in ARR. These aren't aspirational numbers—they are delivered, recurring, profitable dollars. And the momentum has only accelerated since.

The Centaur Club: From 14 to 36 and Counting

Let's rewind just three years. In 2022, according to a Bain & Company report, only 14 Indian SaaS companies had exceeded the $100M ARR mark. Five years before that, that number was one or two. Today, the "Centaur Club" (the SaaS industry's term for $100M+ ARR companies) has exploded past 36, according to the latest estimates. The JM Financial report from July 2025 explicitly states that more than 36 Indian SaaS companies have now crossed this threshold. What changed?

Global-first product mindset: Unlike the first generation of Indian software companies that built for domestic IT services, today's SaaS founders build for the world from day one. 85% of top Indian SaaS firms have expanded to the lucrative US market.

Capital efficiency: Indian SaaS companies are notoriously lean. The famous "Zoho model"—bootstrapped, profitable, and global—has inspired a generation of founders who prioritize unit economics over vanity metrics.

The AI inflection point: According to Bessemer Venture Partners, 92% of Indian SaaS companies have adopted AI features in the past year, using AI not as a gimmick but as a core driver of product value and customer retention. PULL QUOTE #2 “India’s SaaS centaurs and unicorns are projected to generate $20–25 billion in revenue by 2030. The quiet army is becoming a global force.” — Bessemer Venture Partners Report 2024

The Giants Leading the Charge

Who are these 36+ centaurs? While the full list is deliberately quiet (many bootstrapped firms avoid PR), the known heavyweights set the benchmark:

Zoho: The bootstrapped behemoth from Chennai serves 80+ million users globally and has never raised a dollar of VC funding. With over 60 products spanning CRM, finance, and productivity, Zoho's ARR is estimated well north of $1 billion.

Freshworks (NASDAQ: FRSH): The poster child of Indian SaaS, Freshworks has a $10+ billion market cap and serves 60,000+ customers worldwide. Its IT service management product, Freshservice, alone achieved $540 million ARR in 2025, growing in the "mid-20% range," with AI adoption accelerating enterprise deals.

Postman: The API development platform, valued at $5.6 billion, counts 20+ million developers globally among its users. It has become the de facto standard for API testing and collaboration.

Icertis: The contract lifecycle management leader, headquartered in Bellevue but with massive R&D in Pune, crossed $400 million ARR in 2025. Its AI-powered contract intelligence is used by 40% of the Fortune 100.

Chargebee: The subscription management platform, now valued at $3.5 billion, serves over 4,000 businesses globally and has quietly become the billing backbone for thousands of digital brands.

BrowserStack: The web and mobile testing platform, bootstrapped until 2020, now has over 50,000 customers and is estimated to have crossed $200M ARR, profitable every single year. These are not unicorns in the traditional sense (valuation > $1B). They are centaurs—sustainable, capital-efficient, and built to last.

The Tier-2 Surprise: SaaS from Indore, Jaipur, and Coimbatore

The most exciting trend is the decentralization of SaaS talent. No longer is Bengaluru the only hub.

Indore: Keka HR, a bootstrapped HRMS platform, reportedly crossed ₹200 crore ARR (~$24M) in 2025, growing at 80% YoY, serving 8,000+ SMEs. Founder Vijay Yalamanchili famously refused VC money to retain control.

Jaipur: Wingify, maker of the A/B testing tool VWO, has been profitable for over a decade, serving 7,000+ customers including Microsoft and Target. Estimated ARR ~$50M+.

Coimbatore: Zoho itself has a massive campus there, but smaller firms like Zomentum (sales acceleration for IT channel partners) raised $13M and are scaling.

Ahmedabad: Simform (engineering services + SaaS) and Krayonnz (peer-to-peer learning) are building quietly but globally. What enables this? Cheap bandwidth, UPI for cross-border payments, and a decade of remote-work culture. A founder in Indore can hire from Mumbai, sell to New York, and get paid in USD—all while paying tier-2 rents.

The $50 Billion Horizon

According to Bessemer Venture Partners' 2024 State of the Cloud India Report, Indian SaaS is poised to reach $50–70 billion in annual recurring revenue by 2030, up from $15 billion in FY24. That's a CAGR of approximately 25-30%. The report highlights that Indian SaaS companies have a unique advantage: they can build for the West at a fraction of the cost, then expand to the emerging world (Southeast Asia, Middle East, Africa) with culturally adapted products. No other geography has that dual fluency. Moreover, the public market reception has been encouraging. Freshworks and Newgen Software trade at healthy multiples. Matterport (merged with a SPAC) and MapmyIndia (Mappls) have shown that Indian SaaS can list and thrive.

The Silent Exit Problem (And Why It's Changing)

Historically, Indian SaaS had an "exit problem"—most companies were acquired by US giants (e.g., Citrix acquired Zoho's early competitor, or Uber acquired Restaurant Brands). But that is shifting. 2025–2026 saw a flurry of IPOs and direct listings:

Unicommerce (SaaS for e-commerce fulfillment) listed successfully.

RateGain (travel tech SaaS) hit a $1 billion market cap.

Innovaccer (healthcare SaaS) filed confidentially for a US IPO. And the secondary market for SaaS equity is now robust. QIPs (Qualified Institutional Placements) and pre-IPO placements are common.

The Global Indian Takeaway

For the Indian diaspora, SaaS represents a rare asset class:

Invest directly via platforms like Rainmatter, LetsVenture, or through VC funds like Accel India, Matrix, and Sequoia (now Peak XV).

Join as an operator – Indian SaaS companies desperately need US-based sales and marketing leaders who understand enterprise procurement.

Partner as a reseller – Many Indian SaaS firms lack US channel partners. A diaspora professional with a network can earn 20-30% commissions. The quiet club of $100M centaurs is not so quiet anymore. And the next Emergent—the one that will go from zero to $100M ARR in six months—is probably being coded right now, in a small apartment in Indore or Coimbatore, by a founder you've never heard of.That's the power of Indian SaaS: silent, profitable, and inevitable.

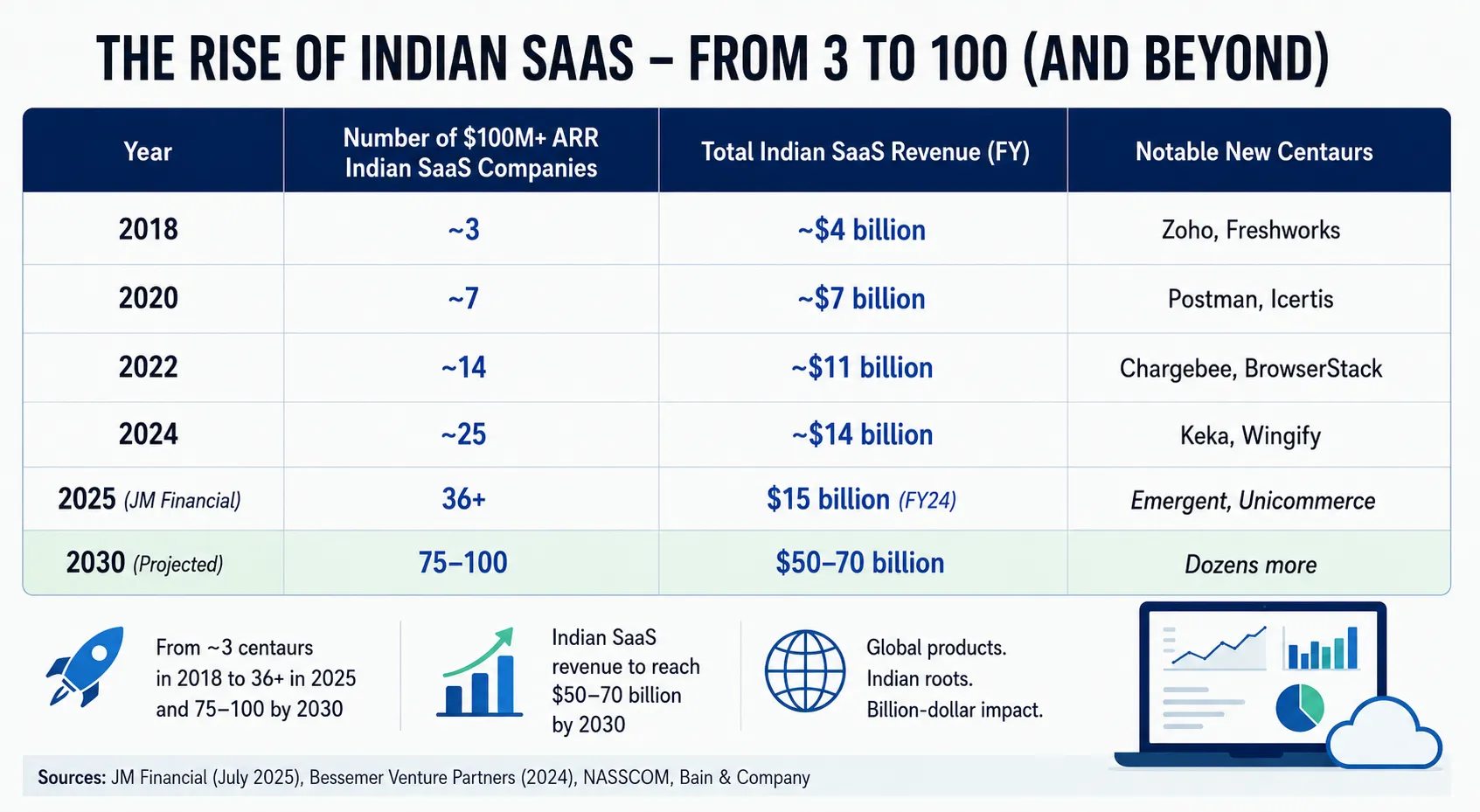

CHART: "India's SaaS Centaur Explosion (2018–2026)"

Year | Number of $100M+ ARR Indian SaaS Companies | Total Indian SaaS Revenue (FY) | Notable New Centaurs |

|---|---|---|---|

2018 | ~3 | ~$4 billion | Zoho, Freshworks |

2020 | ~7 | ~$7 billion | Postman, Icertis |

2022 | ~14 | ~$11 billion | Chargebee, BrowserStack |

2024 | ~25 | ~$14 billion | Keka, Wingify |

2025 (JM Financial) | 36+ | $15 billion (FY24) | Emergent, Unicommerce |

2030 (Projected) | 75–100 | $50–70 billion | Dozens more |