The $725 Billion Fever: Inside the Greatest Infrastructure Bet in History — and the Quiet Evidence It May Already Be Overheating

SILICON VALLEY — May 18, 2026 — Some numbers are too large to feel. The human mind can grasp a hundred, a thousand, perhaps a million with effort. Beyond that, figures blur into abstraction. So when the four largest technology companies on Earth — Microsoft, Alphabet, Amazon, and Meta — disclose, in a single earnings week in late April, that their combined capital expenditures will reach approximately $725 billion in 2026, the number floats past comprehension. It is roughly the GDP of Switzerland and Sweden combined. It represents a 77 percent increase over last year's record $410 billion. It is, by any historical measure, the largest concentrated infrastructure buildout in the history of private industry — larger than the railroad boom, larger than the interstate highway system, larger than the original buildout of the internet itself in real terms.

And yet, beneath the headline, a quieter set of numbers is accumulating — numbers that suggest the boom may be less about physical expansion than about a supply chain that has quietly broken. Memory chip prices are on track to more than double in 2026. Component cost inflation is consuming a growing share of every capex dollar. And the debt markets that are funding the buildout are beginning to price in risks that the equity markets have not yet absorbed.

The AI infrastructure buildout is real. The question hanging over it is whether the spending is building capacity — or simply paying more for the same capacity, at prices the market cannot sustain.

The Numbers

The headline figures, broken down by company, tell a story of collective conviction that has no obvious parallel. Microsoft expects calendar-year 2026 capital expenditures to reach $190 billion, including $25 billion the company attributed solely to higher component pricing — a disclosure that echoes Meta's earlier guidance. Alphabet guided to $180 billion to $190 billion, with capex expected to increase "significantly" in 2027. Amazon held firm on a plan approaching $200 billion, spanning AI, custom chips, robotics, and low-Earth-orbit satellites. Meta raised its forecast to $125 billion to $145 billion, a $10 billion hike at both ends that sent the stock down 6 percent on the announcement. Oracle, the fifth major hyperscaler, brings the combined total toward $800 billion. Morgan Stanley analysts now project the Big 5 will collectively spend roughly that sum in 2026 before climbing toward $1.1 trillion in 2027.

The Dell'Oro Group, which tracks data center capital expenditure across the industry, reported that global data center capex surged 57 percent in 2025 to over $420 billion, and is projected to surpass $1 trillion in 2026 — a milestone the firm's analysts had not expected to arrive for at least three more years. "Last year, I thought it would take at least three years to get to that trillion-dollar mark," Baron Fung, senior research director at Dell'Oro, told Light Reading. By 2030, Dell'Oro expects cumulative global data center capex to reach $1.7 trillion.

The revenue is real, and it is growing. Google Cloud crossed $20 billion in quarterly revenue for the first time, up 63 percent year-over-year, with operating income tripling to $6.6 billion. Microsoft's AI business surpassed a $37 billion annual revenue run rate, up 123 percent year-over-year. AWS generated $14.2 billion in operating income at a 37.7 percent margin. These are serious businesses generating serious cash — but they are not yet generating cash at a pace that matches the spending. Microsoft alone sits on $80 billion in unfulfilled Azure orders because it cannot find enough electricity to power its GPUs.

The broader economic context makes the spending even more remarkable. The S&P 500 trades at roughly 23 times forward earnings, well above its historical average. The IPO market, dormant through 2024, has roared back: Cerebras debuted at $95 billion, SpaceX is targeting $1.75 trillion, Anthropic is expected to list near $900 billion. Capital is flooding into the AI infrastructure layer at a velocity that has no peacetime precedent, and the hyperscalers are at the center of the flood.

The Memory Tax

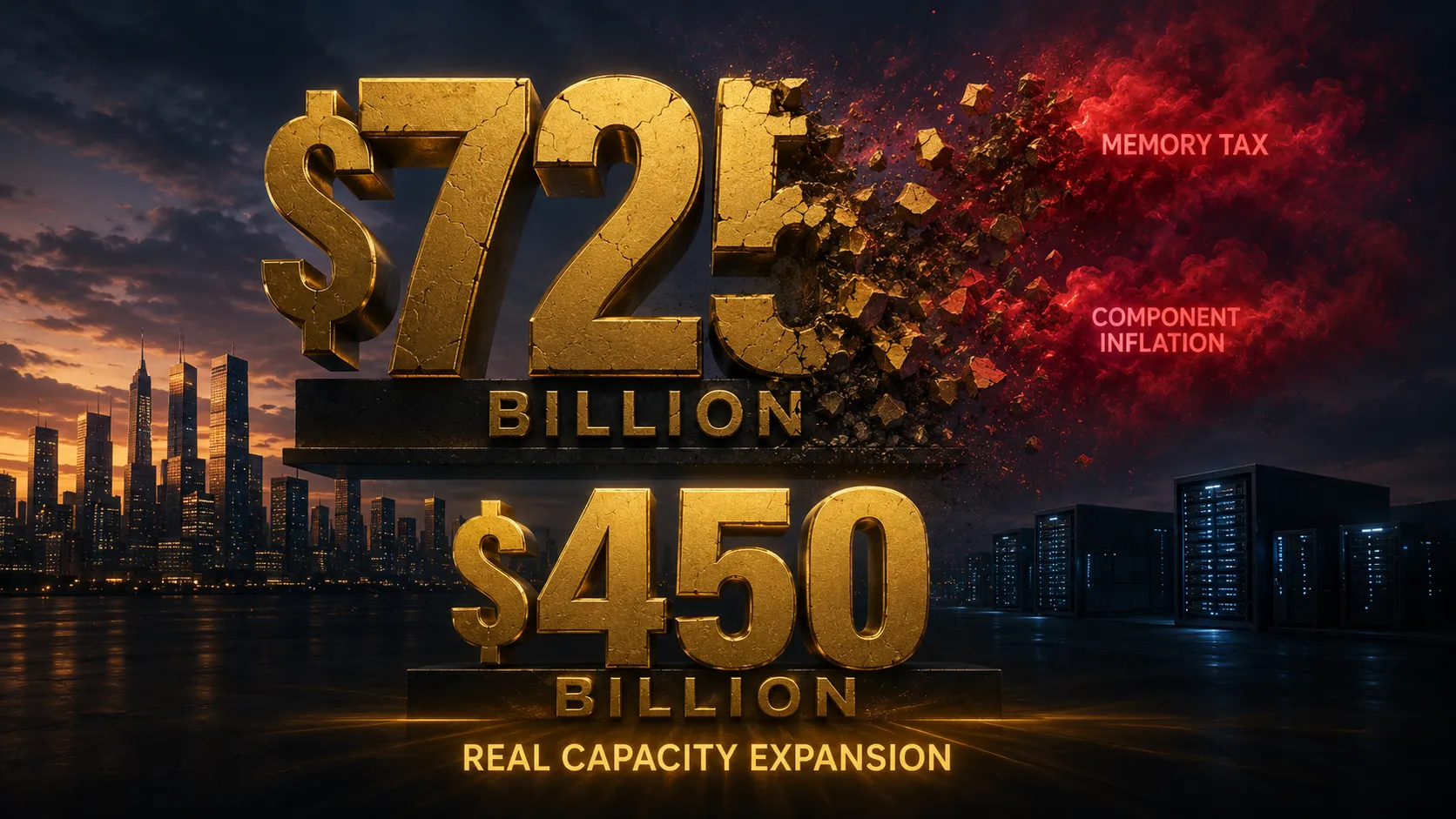

But embedded in the headline numbers is a quieter, more unsettling story — one that suggests a significant share of the $725 billion is being consumed not by building new capacity, but by paying higher prices for the same components.

Research firm TrendForce expects DRAM prices to jump as much as 63 percent in the second quarter of 2026 alone, while NAND flash prices could surge 75 percent. SemiAnalysis, a semiconductor research firm, estimates that memory will account for roughly 30 percent of total hyperscaler capex in calendar year 2026 — up from approximately 8 percent in 2023 and 2024, a near four-fold shift in just three years. The firm projects that share will climb further in 2027.

This is the memory tax. In 2023, for every dollar a hyperscaler spent on AI infrastructure, roughly eight cents went to memory. By 2026, that figure has jumped to thirty cents. The buildout is real — hyperscalers are genuinely deploying more servers, more GPUs, more networking equipment — but a growing share of every capex dollar is being absorbed by component price inflation rather than real capacity expansion. SemiAnalysis warns that the effect of memory inflation is only partly reflected in 2026 capex guidance; the repricing expected in 2027 has yet to be captured by Wall Street's current forecasts.

The dynamic is not unique to memory. Server average selling prices are increasing by high double digits in 2026, driven by escalating DRAM and storage costs, according to Dell'Oro. High-bandwidth memory — the specialized DRAM used in AI accelerators — is in particularly short supply, with lead times stretching and prices rising faster than any other semiconductor category. The physical constraints on AI expansion are more stubborn than the software industry is accustomed to, and the supply chain is proving less elastic than the demand forecasts that have driven the hyperscalers' spending plans.

The Debt-Fueled Furnace

The most important financial detail about the hyperscaler capex boom may not be its size. It is how it is being paid for. Historically, technology companies funded infrastructure out of operating cash flow. That tradition is fraying.

In 2025, hyperscalers raised approximately $108 billion in debt markets to fund AI capex. Bank of America has lifted its forecast for investment-grade bond issuance by hyperscalers by 25 percent to $175 billion for 2026. So far this year, hyperscalers have already issued about $110 billion of investment-grade debt, representing roughly 63 percent of that updated forecast. The pipeline remains active.

Morgan Stanley expects $250 billion to $300 billion of debt issuance in 2026 from hyperscalers and related joint ventures alone. Off-balance-sheet project finance structures — backed by long-term leases — are emerging as a key mechanism to fund massive data-center projects without overwhelming corporate balance sheets. "It'll take all the markets to fund AI spending," Apollo Global Management president Jim Zelter said in early May, adding that debt funding for AI capital expenditures will remain healthy at least until 2028. Consensus forecasts for hyperscaler capex have risen by nearly $80 billion since the start of the earnings season alone, Goldman Sachs strategists noted.

The logic is clear. The hyperscalers are betting that the AI infrastructure they are building today will generate returns over the next decade that justify the debt. But the scale of the borrowing is beginning to attract scrutiny. CNBC reported in February that the AI debt binge had "shattered hyperscalers' unspoken contract with investors" — a reference to the fact that big tech companies have historically been viewed as "asset-light" cash-flow machines, not capital-intensive industrial enterprises. UBS data indicates that aggregated capex spend among AI hyperscalers could top $770 billion in 2026, some 23 percent higher than previously expected.

The most sobering comparison, raised by multiple analysts, is to the fiber optic boom of 1998–2001, when a similar conviction that internet traffic would grow exponentially forever led to massive overinvestment, a glut of capacity, and a devastating bust that wiped out trillions in market value. The parallels are imperfect — AI infrastructure serves a different and arguably more durable demand than the fiber networks of the dot-com era — but the dynamics of capital-intensive buildouts fueled by debt are universal. The hyperscalers have historically pristine balance sheets, and their ability to raise debt at favorable rates remains intact. But the scale of the borrowing is unprecedented, and the question of whether the revenue will catch up to the spending before the debt markets lose patience is not yet answered.

The Power Constraint

Even if the financial questions are resolved favorably, a physical constraint looms that no amount of capital can easily overcome: electricity. BlackRock estimates that approximately 148 gigawatts of additional power capacity will be needed in the United States by the end of the decade to satisfy data center demand. The firm projects that AI data centers could consume as much as 24 percent of U.S. electricity by 2030. BlackRock CEO Larry Fink said in early May that a single one-gigawatt data center now costs $50 billion to $75 billion to build — figures that would have seemed absurd just three years ago.

The power constraint is already binding. Microsoft sits on $80 billion in unfulfilled Azure orders because it cannot secure enough electricity to power the GPUs those orders require. Data center developers are increasingly concentrated in a handful of states — Virginia, Texas, Oregon — where power development is feasible and politically supported, creating geographic bottlenecks that compound the supply constraints. McKinsey projects that global data center capacity demand could triple by 2030, with 70 percent coming from AI workloads, and that cumulative investment in data center and AI computing infrastructure could reach $6.7 trillion to $7 trillion by the end of the decade.

The power industry, for its part, is scrambling to respond. NRG Energy has embarked on a "bring your own power" strategy, building dedicated natural-gas generation alongside hyperscaler data centers. The broader energy sector is being reshaped by AI demand in ways that are only beginning to be understood. But the timelines are mismatched: a data center can be built in 18 to 24 months; a new natural-gas power plant takes four to six years; a new nuclear plant takes a decade or more. The power constraint is not a financial problem. It is a physics problem, and it will not be solved by higher capex budgets.

What Comes Next

The AI infrastructure boom is simultaneously the most exciting and most anxiety-inducing story in the global economy. It is exciting because the technology being built — the GPUs, the ASICs, the fiber networks, the liquid-cooled data centers — will underpin a generation of economic growth and productivity improvement that may rival the internet itself. It is anxiety-inducing because the spending has outpaced the revenue, the debt has outpaced the cash flow, and the supply chain has outpaced the physical capacity of the industries — power, memory, construction — that must deliver the infrastructure.

The most likely outcome is neither a straightforward boom nor a catastrophic bust, but a sorting. The hyperscalers with the strongest revenue growth — Microsoft, with its $37 billion AI run rate; Google, with its 63 percent cloud growth — will be able to sustain elevated capex longer than those whose AI monetization is less advanced. The memory price inflation that is currently consuming a growing share of every capex dollar will eventually ease as new fabrication capacity comes online, but the timing of that easing is uncertain. And the power constraint, which is the most fundamental bottleneck of all, will determine the pace of deployment regardless of how much capital is available.

For the American entrepreneur and investor, the hyperscaler capex boom offers a clear signal amid the noise. The infrastructure layer of artificial intelligence — the chips, the data centers, the power plants, the cooling systems, the networking equipment — is absorbing capital at a rate that has no peacetime precedent. The companies that supply that layer are the primary beneficiaries of the buildout, and they will remain so regardless of which AI models or applications ultimately capture the most value. The picks and shovels, in this gold rush, are being bought by the trillion.

But the boom also carries a warning. Infrastructure buildouts fueled by debt have a history of ending badly when the revenue fails to materialize at the pace the spending requires. The $725 billion figure is real, but a growing share of it is being consumed by memory prices, component inflation, and power constraints — forces that no hyperscaler can control. The fever is high. The patient is strong. The question that will define the next chapter of the AI economy is whether the fever breaks before the patient does.