The $600 Billion Machine: Inside the AI Infrastructure Boom That's Reshaping the Global Economy—and Flirting With a Bust

SILICON VALLEY — May 2026 – Some numbers are too large to feel. The human mind can grasp a hundred, a thousand, perhaps a million with effort. Beyond that, the figures blur into abstraction. So when the five largest technology companies on Earth—Amazon, Microsoft, Alphabet, Meta, and Oracle—announce that their combined capital expenditures will exceed $600 billion in 2026, a 36% increase over 2025, the number floats past comprehension. It is roughly the GDP of Sweden. It is more than the world spends on primary education. It is, by any historical measure, the largest concentrated infrastructure buildout in the history of private industry.

But the number is real, and it is reshaping the global economy in ways that are only beginning to be understood. According to Dell'Oro Group, data center capital expenditures jumped 57% in 2025, reaching over $420 billion among the top hyperscalers. The four largest U.S. cloud providers—Amazon, Microsoft, Alphabet, and Meta—collectively spent over $340 billion, with Amazon alone accounting for $125 billion. And the spending is not slowing. It is accelerating.

Roughly 75% of the 2026 capex, or approximately $450 billion, is tied directly to AI infrastructure—servers, GPUs, data centers, networking equipment. The rest goes to traditional cloud infrastructure, which is also growing, but at a much slower pace. The AI buildout is not a feature of the technology industry. It is the industry.

The Debt-Fueled Furnace

The most important financial detail about the hyperscaler capex boom is not its size. It is how it is being paid for. Historically, technology companies funded infrastructure out of operating cash flow. That tradition is ending.

In 2025, hyperscalers raised $108 billion in debt markets to fund AI capex, according to Introl research. Projections suggest as much as $1.5 trillion in total debt issuance over the coming years as the gap between capex commitments and free cash flow widens. Calcbench analysis shows that combined capex for the big five hyperscalers is now approaching—and in some cases exceeding—their combined operating cash flow. Amazon's capex came "dangerously close" to exceeding operating cash flow in 2025, the firm noted. Oracle, a company that was not historically capital-intensive, saw its capex soar beyond cash flow in 2024 and accelerate further in 2025.

The logic is clear. The hyperscalers are betting that the AI infrastructure they are building today will generate returns over the next decade that justify the debt. But the scale of the bet is unprecedented. It assumes that AI demand will not plateau, that the current generation of models will not be obsoleted by a more efficient architecture, and that the hyperscalers can maintain pricing power in a market that is attracting enormous competition. None of these assumptions are guaranteed.

The most striking comparison is to the fiber optic boom of 1998–2001, when a similar conviction that internet traffic would grow exponentially forever led to massive overinvestment, a glut of capacity, and a devastating bust. The parallels are imperfect—AI infrastructure serves a different and arguably more durable demand—but the dynamics of capital-intensive buildouts fueled by debt are universal.

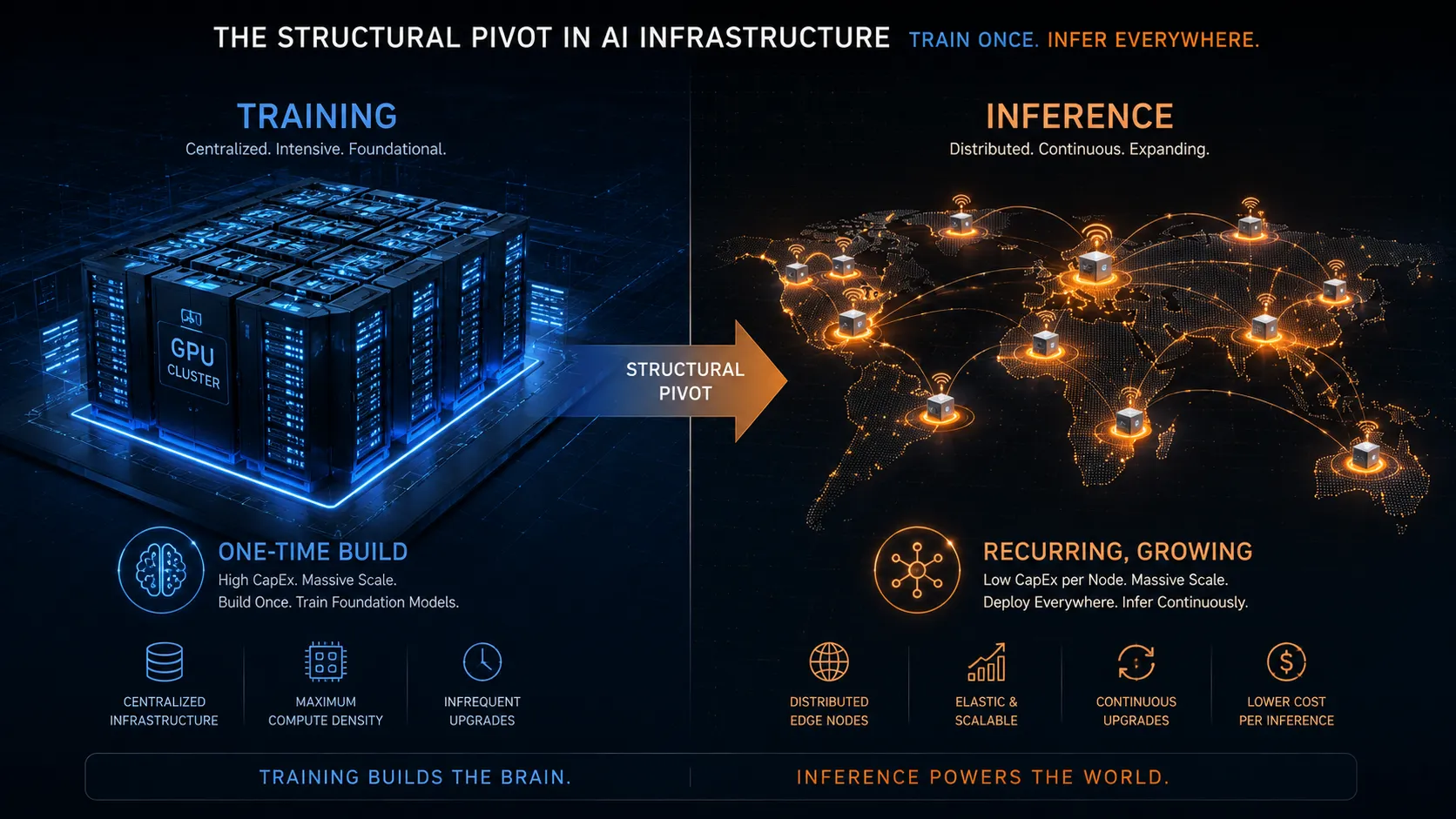

From Training to Inference

Beneath the headline capex numbers, a significant structural shift is underway. Through 2025, the vast majority of AI infrastructure spending was directed at training—the process of building large language models from scratch using enormous datasets. Training is extraordinarily compute-intensive, requiring tens of thousands of GPUs running continuously for months.

Dell'Oro Group noted in March 2026 that AI investments are now shifting focus from training to inferencing, especially as models become more complex and "token-hungry." Reasoning models—which generate step-by-step chains of thought before producing an answer—consume far more compute at inference time than simpler models. As these models proliferate, the infrastructure demand profile shifts. Training is a one-time cost. Inferencing is recurring, growing with every user query, every API call, every AI-generated email or image.

This shift has profound implications for the economics of the capex boom. If inference becomes the dominant workload, the hyperscalers will need to deploy AI infrastructure not just in a few centralized data centers, but at the edge, close to users, to reduce latency. That means more data centers, more networking equipment, more spending. The capex boom may not be a temporary spike. It may be the new baseline.

The Overcapacity Risk

Not everyone is confident that the hyperscaler spending spree will end well. Dell'Oro's Baron Fung noted that "this heightened level of investment raises the potential for overcapacity in AI infrastructure, although hyperscalers are taking proactive measures to mitigate risks and optimize costs." The qualification is diplomatic. The concern is real.

The risk of overcapacity stems from a fundamental uncertainty: nobody knows how much AI compute the world will actually need five years from now. The hyperscalers are building as though demand will grow exponentially, following the trajectory of the past three years. But technology adoption curves do not always follow smooth exponentials. They plateau. They are disrupted by new architectures. They are constrained by physical limits—power, land, cooling, supply chains—that software does not respect.

A more immediate concern is component price inflation. Memory chip costs, particularly for the high-bandwidth memory used in AI accelerators, have surged as supply struggles to keep pace with demand. These cost increases are directly inflating hyperscaler capex without necessarily delivering commensurate capacity expansion. A significant share of the $600 billion is being consumed by higher component prices, not by more servers. The buildout is real, but it is also being artificially inflated by supply constraints that may ease.

The debt markets are watching. The hyperscalers have historically pristine balance sheets, and their ability to raise debt at favorable rates remains intact. But the scale of the borrowing is beginning to attract scrutiny. If the revenue from AI infrastructure does not materialize as quickly as the spending, the financial engineering that is funding the boom could become a constraint rather than an enabler.

What Every Entrepreneur Can Learn

The hyperscaler capex boom offers lessons that extend well beyond the companies writing the checks.

First, infrastructure booms create ecosystems, not just winners. The hyperscalers are spending $600 billion, but the bulk of that money flows to suppliers—Nvidia for GPUs, Arista for networking gear, Vertiv for power and cooling equipment, and a growing army of startups solving specific infrastructure bottlenecks. The entrepreneurs who profit most from the capex boom are not those trying to compete with Amazon. They are those building the picks and shovels that Amazon needs.

Second, the shift from training to inference is a market signal. As AI workloads pivot toward inference, the competitive landscape shifts. Inference is more distributed, more latency-sensitive, and more price-sensitive than training. It creates opportunities for edge computing, specialized inference chips, and software platforms that optimize inference costs. Entrepreneurs should follow the workload, not the hype.

Third, debt-funded buildouts eventually face a reckoning. The fiber optic boom of the late 1990s and the cleantech manufacturing boom of the late 2000s both ended when debt markets lost patience with revenue trajectories that failed to match capex commitments. The AI infrastructure boom is not immune to this dynamic. The entrepreneurs who survive the cycle will be those who build capital-efficient businesses that do not depend on the boom continuing indefinitely.