The $3.44 Billion Wake-Up Call: How Ronnie Screwvala Is Consolidating the Rubble of India's Edtech Crash — and Building Something That Might Actually Last

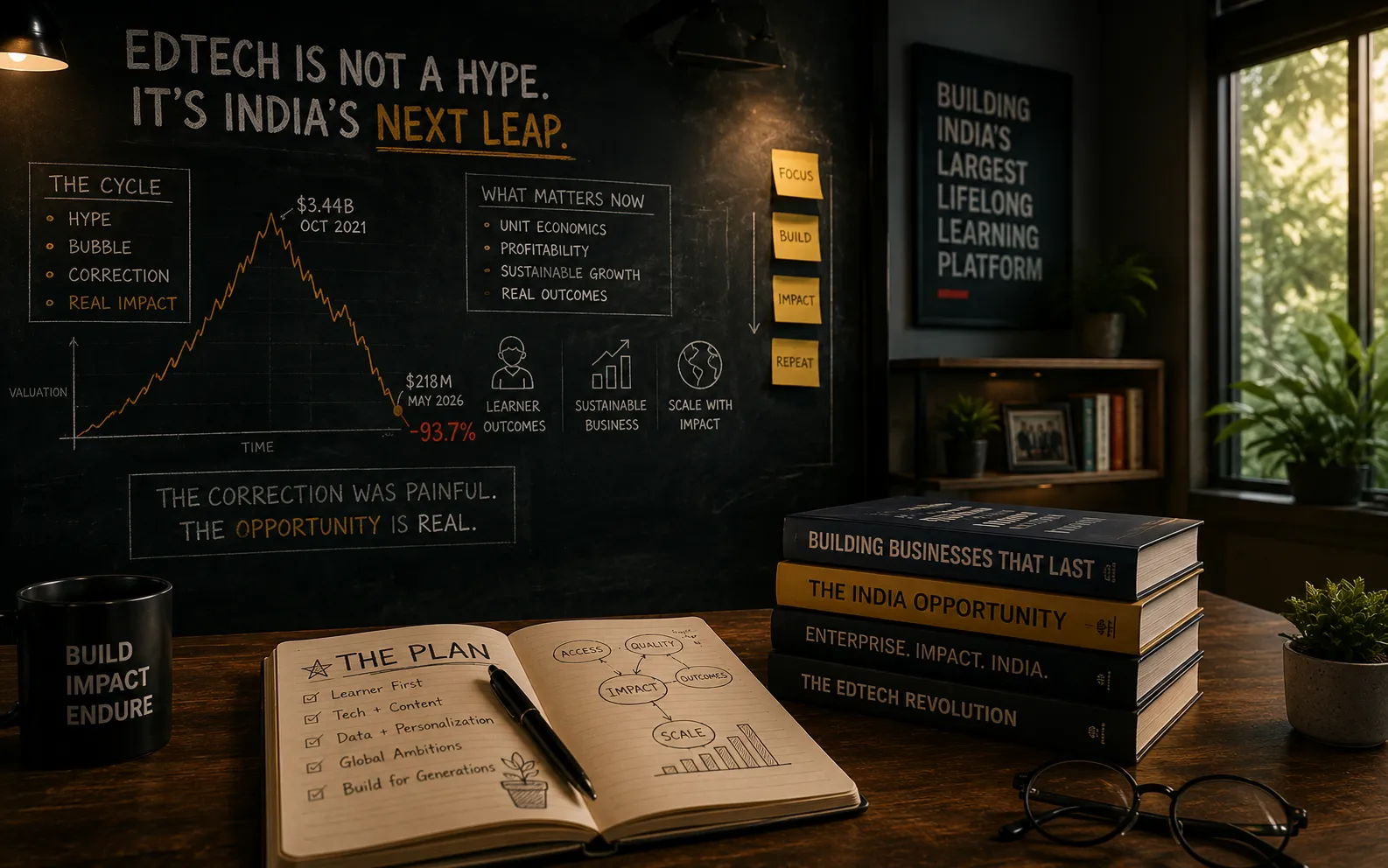

MUMBAI — May 20, 2026 — In the autumn of 2021, Unacademy was worth $3.44 billion. Its founder, Gaurav Munjal, was 27 years old. The company had raised nearly $900 million from SoftBank, Tiger Global, and Sequoia Capital. It had acquired a dozen startups, launched a graph-novel platform, opened a chain of physical coaching centers, and sponsored every major cricket tournament in India. The narrative was intoxicating: a young, aggressive founder building the Amazon of education, a generational company that would teach India everything it needed to know, from cracking the civil service exam to mastering code. The pandemic had accelerated online learning, and Unacademy was surfing the wave with the bravado of a company that believed the wave would never break.

The wave broke. In the first week of May 2026, Ronnie Screwvala's upGrad closed its acquisition of Unacademy in an all-stock deal valued at approximately ₹2,055 crore — about $218 million. That is a 93.7 percent markdown from the peak. It is less than Unacademy raised. It is less than what the company spent on acquisitions during its expansion binge. It is, by any measure, one of the most dramatic valuation compressions in the history of Indian technology — and the man who engineered the acquisition is not a venture capitalist picking through the wreckage of a distressed asset. He is a 68-year-old media entrepreneur who built India's largest cable television company, sold it to Disney, and then decided, in his mid-sixties, that education was the most important unconquered frontier in Indian business.

The Rise and Fall of India's Edtech Prodigy

To understand what Screwvala has done, one must first understand what Unacademy was — and what it became.

Unacademy was founded in 2015 by Munjal, Roman Saini, and Hemesh Singh as a YouTube channel where educators could post free video lessons. It was simple, democratic, and genuinely useful. By 2019, it had evolved into a platform with thousands of paid subscribers and a growing roster of celebrity educators. Then the pandemic hit. Schools closed. Coaching centers shuttered. Millions of Indian students, trapped at home with smartphones and anxious parents, turned to online learning. Unacademy's user base exploded. Revenue surged. Venture capital — already flooding into Indian tech — turned into a firehose.

Between 2020 and 2022, Unacademy raised over $700 million at valuations that climbed from $500 million to $3.44 billion in roughly 18 months. The company went on an acquisition spree, buying up a test-prep platform here, a coding bootcamp there, a competitive exam app, a graph-novel startup — each acquisition expanding the empire, each one adding to the burn rate. At its peak, Unacademy employed over 12,000 people and was burning approximately $20 million a month. The strategy, articulated with the confidence of a founder who had never experienced a down cycle, was to capture market share at any cost. Profitability could wait. The addressable market was infinite.

The addressable market was not infinite. When schools reopened in 2022, students returned to classrooms. The demand for online test-prep — the core of Unacademy's business — contracted sharply. Revenue growth, which had been running at triple digits during the pandemic, slowed to a crawl. The burn rate, meanwhile, continued at pace. The company attempted multiple restructurings: layoffs, business shutdowns, a renewed focus on core operations. Between 2022 and 2025, Unacademy conducted at least five rounds of workforce reductions. The physical coaching centers were closed. The graph-novel platform was shuttered. The acquisitions were written down. Nothing stopped the bleeding.

By the time Screwvala and Munjal began talking in November 2025, Unacademy had become a cautionary tale — a company that had raised too much, spent too fast, and built a cost structure that was fundamentally misaligned with the post-pandemic reality of Indian education. The deal that emerged from those talks, after months of on-again, off-again negotiations and at least one near-collapse over valuation differences, valued Unacademy at roughly $218 million — less than one-fifteenth of its peak. The all-stock structure meant that Unacademy's investors, including SoftBank and Tiger Global, would receive upGrad equity rather than cash. The exit, if it could be called that, was a paper exit at a price that would have been unthinkable three years earlier.

And yet, in the broader context of Indian edtech, Unacademy got lucky. Byju's, once valued at $22 billion, has effectively collapsed, its founder mired in legal battles, its investors writing down their stakes to zero. Vedantu, Toppr, and a dozen smaller edtech startups have either shut down, been acquired for fractions of their peak valuations, or retreated to niche segments. The edtech sector, which attracted over $4 billion in venture funding during the pandemic frenzy, has experienced a correction so severe that it has become a case study in the dangers of growth-at-all-costs capitalism. Unacademy, at $218 million, at least survived.

The Media Mogul Who Saw It Coming

Ronnie Screwvala is not a venture capitalist. He is not a career edtech executive. He is a media entrepreneur who built UTV, one of India's largest television and film production companies, from scratch, sold it to The Walt Disney Company in a deal that valued UTV at over $1 billion, and then — rather than retiring to a life of philanthropy and board seats — founded upGrad in 2015, at the age of 58, with a conviction that higher education and professional upskilling were the largest underserved markets in India.

Screwvala's approach to edtech has always been distinct from the venture-funded model that produced Unacademy and Byju's. upGrad did not chase mass-market test-prep. It focused on higher education — degree programs, study-abroad offerings, enterprise skilling, professional certification — where the ticket sizes are larger, the customer acquisition costs are more rational, and the unit economics are, in theory, sustainable. The company did not burn capital to acquire users. It built partnerships with universities, developed its own content, and grew at a pace that was deliberate rather than explosive.

That discipline, which looked conservative during the pandemic frenzy, now looks prescient. upGrad is not profitable — few Indian edtech companies are — but it is solvent, it is growing, and it has a capital pool that will, once the Unacademy deal closes and the internal funding round is complete, approach ₹1,260 crore. The ₹360 crore internal round, closed in mid-May 2026, saw Screwvala himself contribute ₹300 crore — a personal commitment that signals both his conviction in the consolidation thesis and his willingness to put his own capital at risk alongside his investors.

Temasek, the Singaporean sovereign wealth fund, invested ₹45 crore in the internal round. The International Finance Corporation and 360 One contributed the balance. The Unacademy deal, once approved by the Competition Commission of India, will add nearly ₹900 crore in cash to upGrad's balance sheet — the cash that Unacademy had on hand, accumulated from its pandemic-era fundraising, now transferred to the acquirer. The combined entity will have the financial firepower to invest in AI-led learning products, expand into offline formats, deepen its presence in overseas markets, and — critically — consolidate a sector that is still fragmented, still reeling, and still in need of rationalization.

The AI Bet

The most interesting dimension of the upGrad-Unacademy combination is not the financial engineering. It is the thesis that the merged entity can use artificial intelligence to do what neither company could do alone: deliver personalized, high-quality education at a cost that Indian students can afford, across every format from test-prep to professional certification to study-abroad counseling.

Screwvala has been explicit about his AI ambitions. In interviews and investor communications, he has described AI as the "connective tissue" that will link upGrad's diverse business lines — higher education, enterprise skilling, global talent mobility, and now test-prep — into a single integrated platform. The vision is ambitious: an AI tutor that can adapt to a student's learning style, identify knowledge gaps, and deliver customized instruction across subjects as diverse as UPSC history, JEE mathematics, and Python programming. The same AI infrastructure that powers the test-prep platform, the thesis goes, can also power upGrad's university partnerships, its enterprise training programs, and its study-abroad advisory services.

The technical challenges are substantial. Building an AI tutor that works across the linguistic and educational diversity of India — a country with 22 official languages and a student population that spans elite urban schools to rural classrooms without reliable electricity — is a problem that no company in the world has solved. But the opportunity is correspondingly large. India's education market is projected to exceed $300 billion by 2030. The company that can use AI to deliver personalized, high-quality instruction at a fraction of the cost of human teachers will have a market measured in the hundreds of millions of students — and a competitive moat that no amount of venture capital can replicate.

Screwvala, at 68, is making a bet that many younger founders would find intimidating: that the future of Indian education belongs not to the company with the most viral marketing or the largest venture round, but to the company with the most patient capital, the most disciplined execution, and the deepest integration of AI into the learning experience. The Unacademy acquisition gives him the test-prep platform he needs to reach the mass market. The internal funding round gives him the capital to build the AI infrastructure. The next three years will determine whether the bet pays off.

What This Signals for Indian Entrepreneurship

The upGrad-Unacademy deal is not merely a story about two companies. It is a story about the maturation of Indian entrepreneurship — and about the structural forces that will separate the winners from the casualties in the post-boom era.

The first signal is about consolidation. The pandemic-era funding frenzy created a generation of Indian startups that were overcapitalized, overstaffed, and optimized for growth at the expense of sustainability. As the funding environment has tightened — Indian startups raised $10.1 billion in FY26, down from $11.3 billion in FY25 — those companies are being forced to confront the structural flaws in their business models. The ones that cannot adapt are being acquired, shut down, or written down. The ones that survive will be consolidated into larger, better-capitalized platforms with the resources to invest in AI, expand into adjacent markets, and build sustainable businesses. The upGrad-Unacademy deal is the most significant consolidation event in Indian edtech. It will not be the last.

The second signal is about founder behavior. Gaurav Munjal, at 27, was the face of India's pandemic-era startup boom — young, aggressive, and unconstrained by the caution that comes from surviving a down cycle. His decision to accept an all-stock acquisition at a 93.7 percent markdown is, in some respects, an act of maturity. He could have continued to fight, continued to burn, continued to chase a turnaround that might never materialize. Instead, he chose to combine his platform with a better-capitalized partner, continue as CEO, and focus on the online education products that were always Unacademy's core strength. The decision is a recognition that survival, in the current environment, is a form of success — and that the next phase of Indian edtech will be built not by the founders who raised the most, but by the founders who adapted the fastest.

The third signal is about Ronnie Screwvala himself. At an age when most entrepreneurs of his generation have retired to philanthropy and board seats, Screwvala is doubling down on one of the most difficult, competitive, and structurally challenged markets in Indian business. He is putting his own capital at risk — ₹300 crore in the internal funding round alone. He is building a platform that spans higher education, enterprise skilling, global mobility, and mass-market test-prep. And he is doing it with the patience of someone who has built and sold a billion-dollar company before — who knows that real businesses take years to construct and decades to mature, and that the valuations that matter are not the ones assigned by venture capitalists in a bull market, but the ones earned by companies that generate real revenue, real profit, and real impact.

The Indian edtech crash of 2022–2025 was a brutal correction. It destroyed billions in notional wealth, erased thousands of jobs, and exposed the structural fragility of companies built on venture-funded hypergrowth. But it also cleared the field for a different kind of entrepreneur — the kind who builds with patience, who consolidates with discipline, and who understands that the most valuable companies are not the ones that grow fastest, but the ones that last.

Ronnie Screwvala is 68 years old. He just bought the most famous edtech startup in India for less than a fifteenth of what it was once worth. He is building an AI-powered education platform that could reach hundreds of millions of students. And he is doing it with his own money. That is not a venture capital story. That is an entrepreneurial story — the kind that doesn't need a $3.44 billion valuation to matter.