The ₹193 Crore Bet: How Plum, Acko and Zopper Are Insuring India's Billion‑Dollar Future

The Hook: The Insurtech Tipping Point

For decades, buying insurance in India meant filling out endless forms, waiting weeks for claims approval, and hoping your agent hadn't forgotten your name. The industry was a byword for friction, opacity, and customer indifference.

That era is ending faster than anyone predicted.

In the first half of 2026 alone, the Indian insurtech sector has witnessed a cascade of landmark funding rounds: Plum's ₹193 crore Series B from Peak XV Partners, Acko's $65 million Series C backed by Binny Bansal and Intact Ventures, and Zopper's $25 million Series D co‑led by Elevation Capital and Dharana Capital — all within a span of months. Even the early‑stage pipeline is electric: Turtlemint is now valued north of $900 million, InsuranceDekho raised $70 million, and niche players like RenewBuy and Toffee have secured seed cheques.

According to a Boston Consulting Group (BCG) and India InsurTech Association (IIA) report, the Indian insurtech sector has raised over USD 2.5 billion and is expected to attract more investment due to significant growth opportunities. India is now home to around 150 insurtech companies, including 10 unicorns and over 45 "minicorns," with revenue increasing twelve times in the past five years to reach USD 750 million. The India insurtech market is projected to exhibit a CAGR of 28.79% during 2026‑2034, reaching a value of USD 12,052.7 Million by 2034 from USD 1,161.9 Million in 2025.

The insurtech tipping point has arrived. And three very different companies — Plum, Acko, and Zopper — are leading the charge.

Plum: Reimagining the ₹25,000 Claim

Every HR professional knows the old insurance pain. An employee files a ₹25,000 reimbursement claim. The insurer takes 25 days to process it. The HR team spends hours chasing updates. The employee gets frustrated. The agent has vanished.

Plum was founded to kill that workflow.

In March 2026, the Bengaluru‑based employee health benefits platform raised ₹193 crore (approximately $20.6 million) in a Series B round led by Peak XV Partners, with participation from existing investor Tanglin Venture Partners and new investor GMO Venture Partners, a Japan‑based global technology investor. This brought the company's total funding to over $32 million.

The numbers behind Plum's growth are striking. The platform is now trusted by over 6,000 organizations to deliver insurance and healthcare benefits to more than 600,000 employees. Founded in 2019 by Abhishek Poddar and Saurabh Arora, Plum has reduced claim filing time to under two minutes through its app — a move that has significantly increased claim activity, especially for smaller amounts. Nearly 20% of claims processed on the platform are below ₹5,000, a segment traditionally underutilised due to cumbersome legacy processes. Plum now processes over 100,000 claims annually, with cashless claims resolved in minutes and reimbursements settled within days.

The company also claims to have reported its first year of cash flow profitability, supported by growth in gross written premium, net revenue retention, and overall revenue. Healthcare services now contribute around 20% of Plum's total revenue.

Abhishek Poddar, Co‑founder and CEO, captured the philosophy: “We made a decision on day one that our north star would be the claims experience, and that everything else would follow from getting that right. Six years in, that belief has shaped the product, the business, and the outcomes we have delivered for customers.”

GV Ravishankar, Managing Director at Peak XV Partners, added: “Plum has reimagined employee health insurance by focusing on one of the moments that matters most to users: the claim. The team has built a fundamentally better product and customer experience, from onboarding and coverage design to claims resolution and preventive care.”

With fresh capital, Plum plans to accelerate expansion and reach 10 million users through partnerships with employers, invest in product development (particularly in automation and AI‑led workflows), strengthen enterprise‑grade security, and build deeper integrations with HR and payroll systems.

PULL QUOTE #2 “Technology‑led insurance is expected to play a significant role in the growth of the underpenetrated insurance sector in India.” — Binny Bansal, Flipkart Co‑founder, on investing in Acko, May 2026

Acko: The Digital‑Native General Insurer Headed for a $2.5 Billion IPO

If Plum is reimagining corporate health insurance, Acko is reimagining everything else — motor, health, travel, and embedded insurance. And it is doing so at a scale that justifies a blockbuster IPO.

In May 2026, the Mumbai‑based digital‑first general insurer raised $65 million (approximately ₹452.3 crore) in a Series C round from a clutch of new and existing investors. New investors included Flipkart co‑founder Binny Bansal (who invested $25 million in his personal capacity), RPS Ventures (managed by former SoftBank managing partner Kabir Misra), and Intact Ventures (the strategic venture arm of Canada's largest provider of property and casualty insurance). Existing investors — Amazon, Accel, SAIF, and TechPro Ventures — also participated, bringing Acko's total raised to $583 million and reportedly valuing the company at $300 million post‑round.

The financial trajectory has been impressive. In FY25, Acko reported revenue of ₹2,837 crore (approximately $340 million), a 35% increase over the previous fiscal year — significantly above the sub‑10% growth recorded by India's broader insurance sector. Net losses fell 37% year‑on‑year. The company is not yet profitable, but the combination of strong top‑line growth and meaningful loss reduction is exactly the trajectory that Indian tech‑oriented businesses need to access the public market at a premium valuation.

That valuation could be substantial. Acko is targeting a $2 to $2.5 billion valuation in its planned initial public offering, having formally hired Kotak Mahindra Capital, ICICI Securities, and Morgan Stanley as book‑running lead managers. The IPO is expected to raise as much as $350 million, comprising a mix of fresh share issuance and an offer‑for‑sale component from existing investors. Acko plans to file its draft red herring prospectus with SEBI via the confidential pre‑filing route in the second half of 2026, with a listing targeted for the first half of 2027.

What makes Acko fundamentally different from traditional insurers? Distribution. Unlike ICICI Lombard or Digit Insurance — which rely substantially on agents and intermediaries — Acko built a direct‑to‑consumer model from the outset, eliminating the distribution layer and selling motor, health, and travel insurance exclusively through its own digital channels and embedded partnerships. The company is embedded within platforms including Amazon India and Ola, which expose its products to large captive user bases without requiring a traditional agent network.

Acko has also pioneered the direct‑to‑consumer auto insurance space in India and has one of the largest market shares in embedded insurance products like mobility and gadget insurance, in partnership with 35+ leading players in the internet ecosystem such as Ola, Oyo, redBus, Zomato, HDB Financial Services, and Urban Company.

In a further signal of maturity, Acko appointed industry veteran Sanjeev S (former MD & CEO of Bharti AXA General Insurance) as part of its leadership team and to its Board of Directors. The company also plans to enter the health insurance business and has announced a Series D fundraise upwards of $250 million, led by General Atlantic and Multiples Private Equity, making it India's latest unicorn.

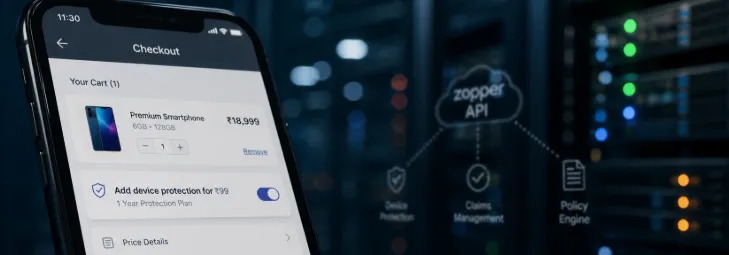

Zopper: The Unseen Infrastructure Behind ₹12,000 Crore in Premiums

While Plum and Acko are customer‑facing brands, Zopper operates in the invisible layer — the API infrastructure that lets other businesses sell insurance seamlessly.

In May 2026, the Noida‑based insurtech platform raised $25 million (approximately ₹211 crore) in a Series D funding round, co‑led by Elevation Capital and Dharana Capital, with participation from existing investor Blume Ventures. This marked the company's first funding event in over two years, bringing its total raised to date to over $100 million.

What does Zopper actually do? It provides an insurance infrastructure API platform that allows banks, NBFCs, e‑commerce platforms, and other enterprises to embed insurance products into their own customer journeys. The company works with insurance providers to create byte‑sized, personalised products that it then supplies to distribution partners — everything from gig worker health coverage for ₹69 per month to device protection at e‑commerce checkout.

The scale is formidable. Zopper processes over ₹12,000 crore in gross written premiums and has distributed insurance to over 100 million customers across India. It has partnerships with 30+ insurers and powers insurance distribution for 600+ enterprise clients, including major banks, NBFCs, and digital platforms.

Zopper's unique position in the ecosystem lies in its "invisible" integration: the end customer often has no idea that Zopper is the engine behind their policy purchase. This B2B2C model has proven highly scalable and capital‑efficient. The company is already profitable, according to PitchBook data.

The company will use this fresh funding to ramp up its digital technology infrastructure, strengthen its insurance distribution platform, invest in data science, AI, and machine learning capabilities, accelerate growth in bancassurance solutions, and enhance the post‑sales and servicing capabilities of its device and appliance protection businesses.

The Ecosystem Beyond the Big Three

Plum, Acko, and Zopper are the headline‑grabbers, but the insurtech pipeline is deep.

Turtlemint, an online insurance distribution platform, is now valued at more than $900 million and is widely expected to join the unicorn club soon. InsuranceDekho raised $70 million in a round led by Mitsubishi UFJ, BNP Paribas Cardif's Insurtech Fund, and Beams Fintech, using the capital to expand its presence and enhance tech‑driven offerings. RenewBuy raised $500,000 in an angel round, while Toffee, a micro‑insurance startup focused on gig workers, raised $1.5 million in seed funding.

Even niche players like Riskcovry and Assurekit are gaining traction, leveraging data analytics to offer customised embedded insurance products, addressing risks like return‑to‑origin and fraudulent orders.

The Structural Drivers: Why Now?

Why is insurtech suddenly booming in 2026? Four structural drivers.

First, underpenetration. India's insurance penetration remains below 4%, with a significant protection gap. The runway for growth is enormous.

Second, regulatory tailwinds. The 100% FDI in insurance proposed in the Union Budget 2025 is expected to spawn new insurance companies and bring global best practices. Regulatory initiatives like NHCX and Bima Sugam are fostering digital innovation.

Third, embedded insurance. The integration of insurance products into e‑commerce platforms, fin‑tech solutions, and ride‑hailing services is creating new accessibility. IRDAI introduced a framework to expand insurance distribution by embedding coverage into consumer platforms, enhancing accessibility and driving market growth.

Fourth, AI‑driven underwriting. Startups are leveraging AI and big data to enhance underwriting, fraud detection, and policy customization. Machine learning algorithms are being utilized to precisely calculate risk profiles and create hyper‑personalized policies.

The Global Indian Takeaway

For the Indian diaspora, the insurtech wave offers three clear opportunities.

First, invest via late‑stage vehicles. Acko's pre‑IPO round and Zopper's Series D are accessible to accredited investors through syndicates and secondary platforms. The $900 million valuation of Turtlemint suggests that the unicorn creation cycle in insurtech is still accelerating.

Second, partner as an enterprise customer. If you run a business in India — or have a portfolio company that does — platforms like Plum offer radically better employee health benefits at competitive premiums. The switch from traditional insurers to insurtech platforms can reduce administrative overhead while improving employee satisfaction.

Third, build distribution bridges. Indian insurtech startups need US and European reinsurance partners, risk modelling expertise, and cross‑border expansion support. Diaspora professionals with experience in global insurance markets can serve as strategic advisors, joint venture partners, or board members.

The Final Word

The ₹193 crore bet on Plum, the $583 million war chest at Acko, the ₹12,000 crore in premiums flowing through Zopper — these are not isolated successes. They are proof points of a larger structural shift: the transformation of Indian insurance from a bureaucratic, agent‑driven industry to a digital, transparent, customer‑centric ecosystem.

Plum is fixing the claim experience for millions of employees. Acko is building a direct‑to‑consumer general insurance powerhouse that is IPO‑bound at a multi‑billion‑dollar valuation. Zopper is laying the API infrastructure that will power insurance distribution for the next decade.

The insurtech tipping point has arrived. And the companies leading it are no longer upstarts — they are the new establishment.

Insurance, for the first time in Indian history, is finally becoming painless. The billion‑dollar future is already underwritten.

CHART: “India’s Insurtech Wave — At a Glance (2026)”

Company | Latest Funding | Round | Lead Investor(s) | Key Focus |

|---|---|---|---|---|

Plum | ₹193 crore ($20.6M) | Series B | Peak XV Partners | Employee health benefits |

Acko | $65 million | Series C | Binny Bansal, Intact Ventures | Digital‑first general insurance |

Zopper | $25 million | Series D | Elevation Capital, Dharana Capital | Insurance infrastructure API |

Turtlemint | (previous) | Growth | — | Online insurance distribution (valued $900M+) |

InsuranceDekho | $70 million | Series B | Mitsubishi UFJ, BNP Paribas Cardif | Insurance distribution |

Other Key Metrics:

Metric | Value | Source |

|---|---|---|

Indian insurtech sector total funding | Over $2.5 billion | BCG‑IIA report |

India insurtech companies | ~150 (10 unicorns, 45+ minicorns) | BCG‑IIA report |

Insurtech revenue growth (5 years) | 12× to $750 million | BCG‑IIA report |

India insurtech market CAGR (2026‑2034) | 28.79% | IMARC Group |

India insurtech market value (2034) | $12.05 billion | IMARC Group |

India insurance penetration | Below 4% | IRDAI / BCG‑IIA |

Plum organizations served | 6,000+ | Avendus |

Plum employees covered | 600,000+ | Avendus |

Plum claims processing time (app) | Under 2 minutes | VCCircle |

Plum claims under ₹5,000 | 20% of total claims | VCCircle |

Acko FY25 revenue | ₹2,837 crore (35% YoY growth) | Bloomberg / TNW |

Acko net loss reduction (YoY) | 37% | Bloomberg / TNW |

Acko total funding | $583 million | Bloomberg / TNW |

Acko IPO target valuation | $2‑2.5 billion | Bloomberg / Reuters |

Acko IPO size | Up to $350 million | Bloomberg / Reuters |

Zopper gross written premiums | ₹12,000 crore+ | Industry reports |

Zopper customers covered | 100 million+ | Startup Chronicle |

Zopper profitability | Yes (PitchBook) | PitchBook |

Turtlemint valuation | $900 million+ | Business Standard |