The ₹100 Revolution: How a Former BCG Partner Is Building India's First Financial OS for 300 Million Shopkeepers — One Day at a Time

DELHI — May 18, 2026 — Anugrah Jain spent a decade inside the machinery of Indian finance before he understood what was broken. As a partner at Boston Consulting Group, he advised two of India's largest non-banking financial companies as they scaled their combined loan books past ₹14,000 crore. He sat in boardrooms. He built models. He became, by any standard, an expert in how money moves through the Indian economy. And somewhere in that decade, he came to a conclusion that has since become the founding thesis of one of India's most closely watched fintech startups: the modern financial system was not built for the people who actually run India.

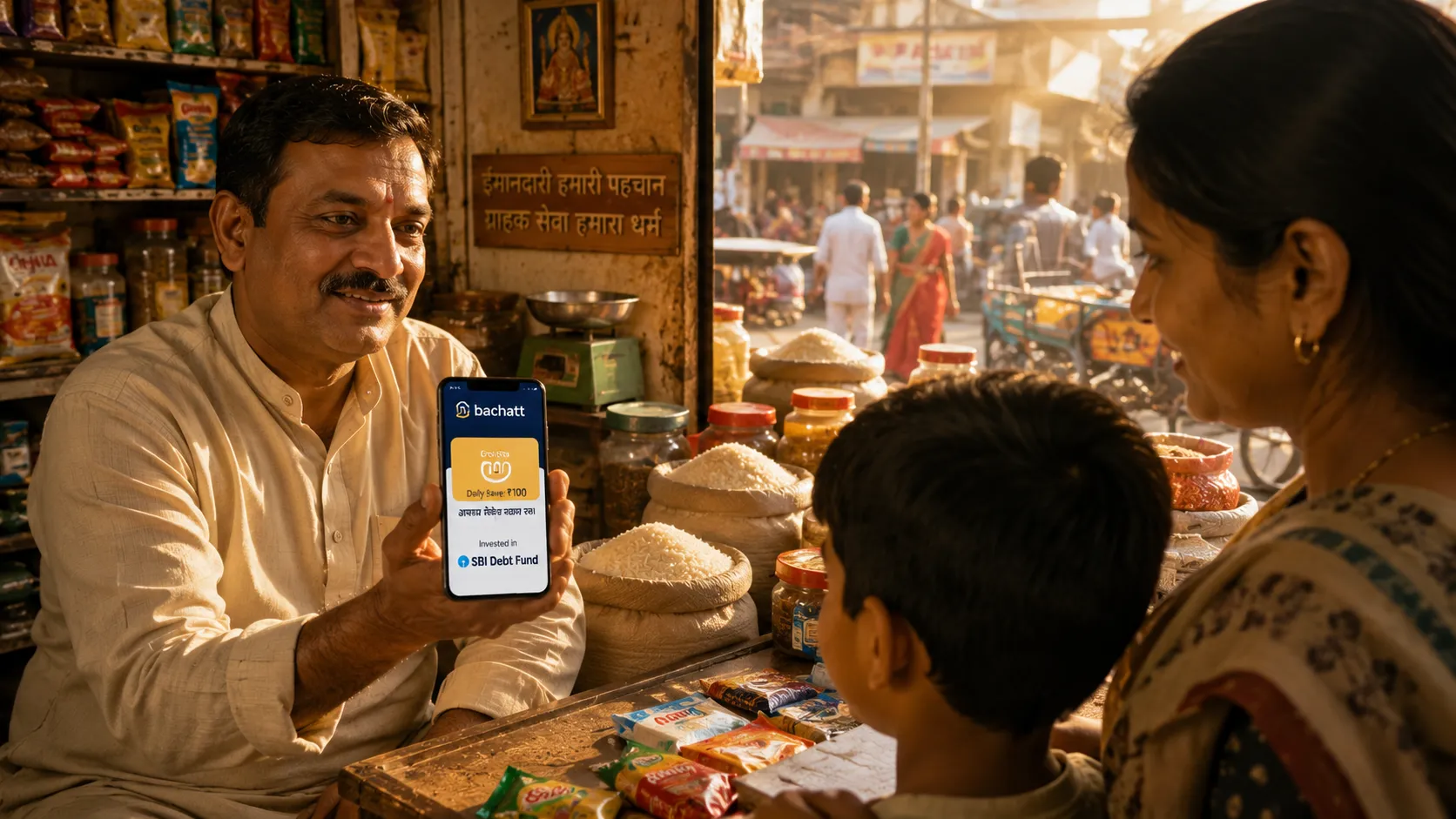

On March 31, 2026, the company Jain built to fix that — Bachatt, meaning "savings" in Hindi — announced a $12 million Series A funding round led by Accel, with participation from Lightspeed Venture Partners and Info Edge Ventures. The round, which brought total funding to $16 million across two rounds, will bankroll an expansion from a single core product — daily debt mutual fund savings starting at ₹100 — into a multi-product financial platform spanning AI-led wealth advisory and near-instant working capital credit. The company has already acquired over 3 million users since its public launch in May 2025, processed more than 2 million mutual fund transactions in February 2026 alone, and is targeting 30 million users within the next 12 to 24 months. The numbers are impressive. The strategic architecture behind them — a rethinking of what a financial product actually is when the customer does not have a salary — is what has drawn some of the sharpest investors in Indian technology to Jain's door.

The Daily Variable Problem

To understand why Bachatt exists, one must first understand the architecture of Indian employment — and the quiet violence it does to standard financial products.

India has approximately 300 million self-employed workers: kirana shopkeepers, jewellery retailers, automobile dealers, tea stall owners, tailors, drivers, small-scale manufacturers. They earn money daily, not monthly. Their cash flows are variable, surging during festivals and contracting during monsoons. They do not receive a pay stub. They do not have a human resources department. They are, by any measure, the productive backbone of the Indian economy — and the financial products designed to serve them are built around a structure of monthly fixed income that bears almost no relationship to their economic reality.

The Systematic Investment Plan, or SIP, is the crown jewel of India's mutual fund industry. It allows salaried investors to contribute a fixed amount monthly into a diversified portfolio, smoothing out market volatility through rupee-cost averaging. It has brought millions of Indians into the formal investment system. It is also, for the 300 million self-employed, a fundamentally alien construct. A kirana shopkeeper does not have a payday. She has a good Tuesday and a bad Wednesday. Her cash flow is daily, variable, and seasonal. Asking her to commit to a fixed monthly contribution — and penalizing her if she misses it — is like asking a farmer to commit to a fixed amount of rainfall. The financial product does not fit the financial life it is supposed to serve.

Jain saw this gap from inside the machine. During his decade at BCG, working with NBFCs that lent to the self-employed, he gained what he calls a "granular understanding" of how this population interacts with financial instruments. What he found was not a lack of savings behavior — the self-employed save, often more diligently than the salaried — but a lack of savings infrastructure. A large majority of shopkeepers, he discovered, relied on cooperative societies: informal, community-based institutions that accept deposits but offer low interest rates, low flexibility, and penalties for early withdrawal. Despite these drawbacks, the self-employed stayed with them — because there was no alternative that matched their cash flow patterns.

"For the non-salaried category or self-employed people, Indian businesses have not really focused on creating financial products conducive for them," Jain told Inc42 after his seed round. "Just like the salaried population, this category of customer also requires products that are coherent and congruent with their cash flows." The insight was not about technology. It was about empathy. The financial system had not failed the self-employed because it was malicious. It had failed them because it had never really seen them.

The Daily SIP

Bachatt's flagship product is, on its surface, almost absurdly simple. A user can invest as little as ₹100 — roughly $1.20 — in debt mutual funds from SBI, ICICI, and Axis AMC. They can save daily, weekly, or monthly. They can pause during lean periods. They can top up during festivals. They can withdraw instantly when a supplier needs to be paid. There are no lock-in periods designed for salaried employees with predictable paychecks. There are no penalties for irregular contributions. There is just a savings vehicle that bends, as Jain puts it, "to the shape of a real economic life."

The simplicity is deceptive. Building a daily SIP that works within India's mutual fund infrastructure required navigating a thicket of operational challenges that Jain and his co-founders — Ankur Jhavery, formerly of OYO, and Mayank Agarwal, formerly of Urban Company — spent months solving. Mutual funds were not designed for daily contributions of ₹100. Know Your Customer verification was not optimized for kirana shopkeepers who open their stores at 6 a.m. and close at 11 p.m. Registrar and transfer agents — the backend plumbing of the fund industry — operated on batch processing cycles incompatible with real-time, low-value daily transactions.

The company partnered directly with the asset management companies — SBI Mutual Fund, ICICI Prudential, Axis AMC — and their registrars to build "numerous industry-first features," as the company's press release describes them: easy digital KYC, instant top-ups and top-downs, pause savings, weekend savings, and instant withdrawals. The partnership with Decentro, a banking API platform, helped automate verification flows, cut onboarding time to five minutes, and achieve 95 percent verification accuracy while reducing customer acquisition costs by 60 percent. The technical infrastructure was built to process high volumes of low-value transactions without breaking the unit economics.

The results validated the design. Since launching publicly in May 2025 — roughly a year after the company's founding in late 2024 — Bachatt has acquired over 3 million users. In February 2026 alone, it processed more than 2 million mutual fund transactions. The debt mutual fund product became, in Jain's words, "an instant hit." The uptake suggests a market that was not difficult to capture — because it had never been served in the first place.

From Savings to Wealth to Credit

Bachatt's ambitions extend well beyond daily savings. The Series A funding will finance the rollout of two new products: an AI-led wealth advisory platform and an instant working capital credit solution for merchants. Together with the core savings product, they form what Jain describes as "5–6 financial solutions, specially curated and tailored" for the self-employed segment.

The wealth product leverages a proprietary AI engine that monitors over 4,000 mutual fund schemes and market patterns. It is designed to identify investment opportunities and make personalized recommendations in "a simple and non-complex way" — a direct response to the fact that most self-employed Indians lack access to professional financial advice. The wealth advisory market for non-salaried Indians is effectively greenfield: the banks and brokerages that serve salaried professionals have not built distribution channels that reach the kirana shopkeeper or the jewellery retailer. Bachatt's existing user base — 3 million people who already trust the platform with their daily savings — provides a warm distribution channel.

The credit product addresses a structural market failure that Jain understands intimately from his BCG years. India's self-employed face an estimated credit gap exceeding $300 billion. Traditional banks cannot underwrite them effectively because standard tools — salary slips, employment verification, credit scores — do not capture the reality of their financial lives. A kirana shopkeeper who saves ₹100 every day for six months, pauses for Diwali, and resumes in November is demonstrating discipline and income stability that a static credit report would never capture. Bachatt's data advantage is its visibility into those cash flows. By observing daily savings patterns, withdrawal behavior, and seasonal income rhythms, the platform can build a credit profile that is far more predictive than a conventional score — and can extend working capital loans within minutes, rather than the weeks required by traditional banks.

"We want to be a trusted financial partner, for the large 300 million merchants and self-employed segment of the country," Jain said. The word "partner" is deliberate. Bachatt is not trying to sell a single product to a single need. It is trying to become the financial operating system for a population that has never had one.

The combination of savings, wealth, and credit on a single platform creates a flywheel. Users start with savings — a low-friction, high-trust entry point. They build a transaction history. They become eligible for credit. They eventually graduate to wealth products. Each product deepens the relationship and generates data that improves the next product. The flywheel is a classic fintech architecture — credit cards built it, digital wallets refined it — but Bachatt is applying it to a user base that has been locked out of the flywheel entirely.

The Competitive Landscape

India's wealthtech and embedded finance space is among the most competitive in the world. Groww, the decacorn investment platform, and Zerodha, the discount brokerage giant, have captured millions of salaried investors. PhonePe and Google Pay are embedding financial services into their payments ecosystems. A new generation of startups — Curie Money, Jar, Niyo — is targeting adjacent segments of the personal finance market. The regulatory environment for mutual fund distribution and digital lending is evolving, and compliance costs will rise as the platform scales.

Bachatt's differentiation is not its technology stack — which is sophisticated but not unique — but its distribution thesis. The company is building for a population that the incumbents have not prioritized: the self-employed who earn ₹30,000 to ₹70,000 per month, who save in ₹100 increments, and whose financial lives do not fit the templates that Groww and Zerodha have optimized for salaried users. Jain's decade at BCG, Jhavery's experience scaling OYO's operations, and Agarwal's background at Urban Company give the founding team a combination of financial expertise, operational discipline, and marketplace sensibility that is unusual in the Indian fintech landscape.

Pratik Agarwal, Partner at Accel, described the combination as "rare to find." Kitty Agarwal, Partner at Info Edge Ventures, pointed to the team's "solid execution with rapid scale to serve millions of consumers within a short period." Ishaan Preet Singh of Lightspeed framed the opportunity more abstractly: "Bachatt is building solutions that massively improve the financial lives of India's self-employed user base, by first understanding that user base extremely well, and then partnering closely with financial institutions to create innovative solutions that just work."

The Road Ahead

Bachatt's target — 30 million users within 12 to 24 months — is ambitious by any standard. It represents a tenfold increase from the current 3 million base. Achieving it will require sustained product execution, disciplined customer acquisition, and the operational infrastructure to handle the surge in transaction volume that will accompany user growth. The company will also need to navigate India's evolving regulatory landscape for digital lending and mutual fund distribution — areas where the Reserve Bank of India and the Securities and Exchange Board of India have both signaled increased scrutiny.

But the structural tailwinds are powerful. India's mutual fund industry manages over ₹60 trillion in assets, and penetration among the self-employed remains in the single digits. The credit gap is measured in hundreds of billions of dollars. The wealth advisory market for non-salaried Indians is essentially greenfield. And the broader macroeconomic context — rising financial literacy, deepening digital payments penetration, increasing smartphone adoption — creates a substrate on which a daily-savings-led platform can scale in ways that would have been impossible even five years ago.

Bachatt's name is a Hindi word that means "savings." But the company's ambition, as articulated by Jain, is larger than the word implies. "We want to be a trusted financial partner," he said. "We want to build 5–6 financial solutions, specially curated and tailored for them." The "them" is 300 million people — roughly the population of the United States — who have been buying vegetables, selling jewellery, repairing automobiles, and stitching clothes for decades, building the Indian economy from the ground up, without ever having a financial product that understood how they actually lived.

The ₹100 note that a kirana shopkeeper invests on a good Tuesday is not a transaction. It is a vote of confidence in the idea that the formal financial system can finally see people like her. Bachatt has taken that vote 3 million times already. The $12 million from Accel, Lightspeed, and Info Edge is a bet that tens of millions more are waiting to cast the same vote — not because they were convinced by a marketing campaign, but because someone finally built a product that met them where they actually stood.