Sanjiv Bajaj — The Man Who Demystified Financial Services for Middle-Class India

The Unlikely Fintech King

Sanjiv Bajaj was not groomed to run a financial company. He was the second son of Rahul Bajaj, the iconic industrialist who built Bajaj Auto into the world’s largest scooter manufacturer. Sanjiv studied engineering at Pune’s College of Engineering and then went to the University of Michigan for a master’s in industrial engineering. He worked at a software company in the US, then returned to India to join the family business — but in the auto division.

In 2007, his father asked him to take over Bajaj Auto Finance, a small division that offered loans for Bajaj scooters. It was a fraction of the size of Bajaj Auto, and it was bleeding. Traditional banks were eating its lunch.

Sanjiv decided to reinvent the business. He changed the name to Bajaj Finance, moved the headquarters from Mumbai to Pune (to stay away from the traditional banking culture), and recruited a young, aggressive team from non-banking backgrounds. His mantra: “Think like a startup, not like a bank.”

The Small-Ticket Loan Revolution

At that time, banks focused on large-ticket loans — home loans, car loans, business loans. They ignored small-ticket consumer loans (₹10,000–₹50,000) because the paperwork was the same but profits were smaller. Sanjiv saw an opportunity.

He launched consumer durable loans — a loan to buy a TV, refrigerator, or smartphone — with instant approval at the store. No income proof, no collateral, just a few documents and a credit check. The loan was repaid in 3-6 months with small EMIs. It was revolutionary.

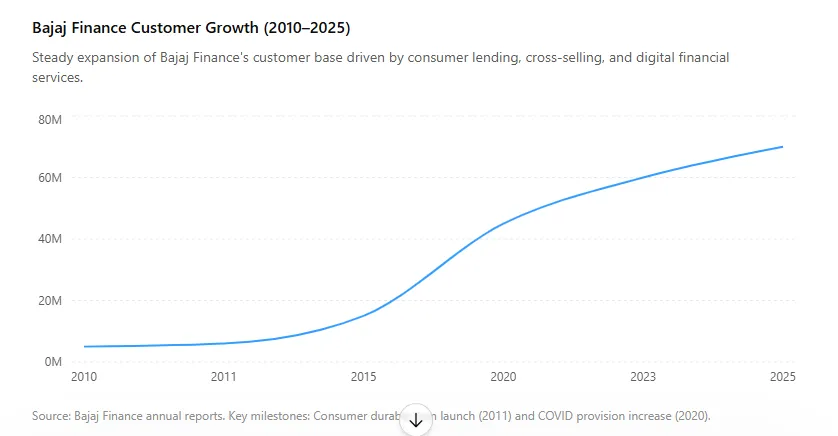

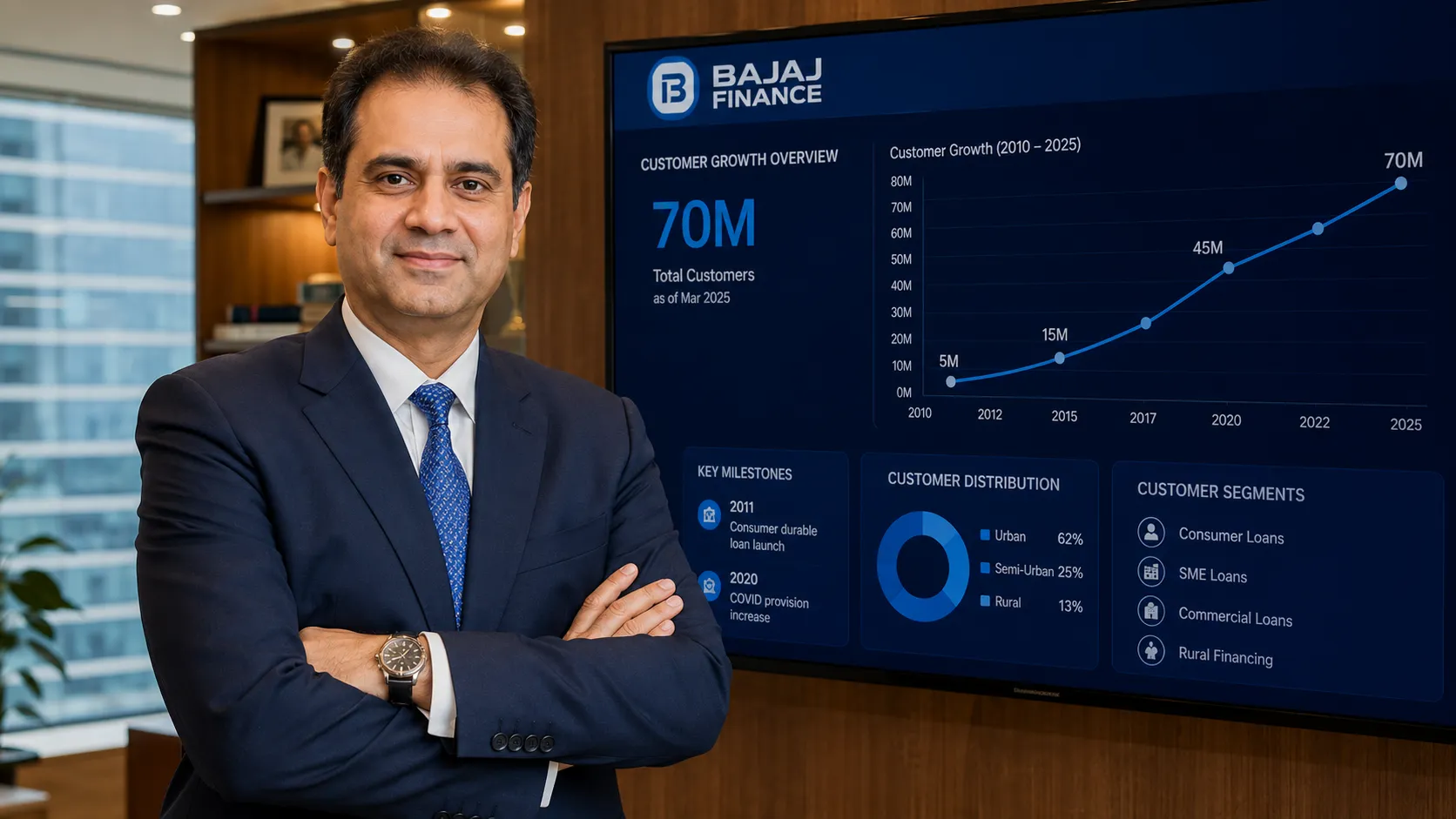

Retailers loved it because it boosted sales. Customers loved it because they could buy expensive items without saving for months. Bajaj Finance grew at 40% annually for a decade. By 2020, it was India’s largest consumer finance company, with over 50 million customers and a market capitalization that briefly surpassed its parent, Bajaj Auto.

Sanjiv also expanded into:

SME lending (loans to small businesses for equipment and working capital)

Two-wheeler loans (direct competitor to his family’s auto division, but he didn’t shy away)

Credit cards (Bajaj Finserv co-branded cards with RBL Bank)

Wealth management and insurance (through Bajaj Allianz and Bajaj Capital)

The Startup Within a Legacy

Sanjiv built Bajaj Finance like a startup, even within a 90-year-old conglomerate. He:

Decentralized decision-making: Branch managers had authority to approve loans up to ₹10 lakh without referring to headquarters.

Invested heavily in technology: He built a proprietary credit underwriting engine that used alternative data (mobile bills, utility payments) to assess customers without credit scores.

Hired young talent: The average age of his leadership team was under 40. He poached from banks and tech companies.

He also embraced digital before most traditional banks. Bajaj Finance’s app allowed customers to apply for a loan, get approval, and receive the money in 30 minutes — a process that took weeks in public sector banks.

The Competition with Fintech Startups

By 2020, fintech startups like Paytm, Razorpay, and CRED were offering similar products. But Sanjiv was not afraid. He argued that Bajaj Finance had three advantages:

Low cost of capital (because of its credit rating)

Physical reach (over 3,000 branches across India, including small towns)

Customer trust (the Bajaj name carried weight)

He also launched his own fintech initiatives: a digital-only lending platform called Bajaj Finserv Direct, and a UPI-enabled payments app called Bajaj Pay. While these didn’t match Paytm’s scale, they served as defensive moats.

By 2025, Bajaj Finance had over 70 million customers and was generating a return on equity of over 20% — among the highest in the world for a large lender.

Leadership Philosophy: Obsess Over the Customer

Sanjiv is known for his detailed, analytical approach. He reads customer complaint emails every morning. He visits branches unannounced and talks to customers waiting in line. He famously said: “The customer does not care about our internal problems. They care about getting their loan in one day.”

He is also frugal. Bajaj Finance’s headquarters in Pune is functional, not lavish. He flies economy on domestic trips and drives a modest car. Employees say he is approachable and listens more than he speaks.

Challenges and Critiques

Asset quality: Small-ticket loans are risky during economic downturns. During the COVID-19 moratorium, Bajaj Finance’s loan defaults spiked. Sanjiv took a conservative approach, increasing provisions and reducing new lending until confidence returned.

Regulatory scrutiny: The RBI has questioned Bajaj Finance’s aggressive growth and high interest rates on consumer loans. Sanjiv has engaged constructively but had to slow down lending in certain segments.

Family dynamics: Being the younger son of Rahul Bajaj, there were always questions of succession. Sanjiv’s older brother Rajiv handles Bajaj Auto. The two have a cordial but competitive relationship.