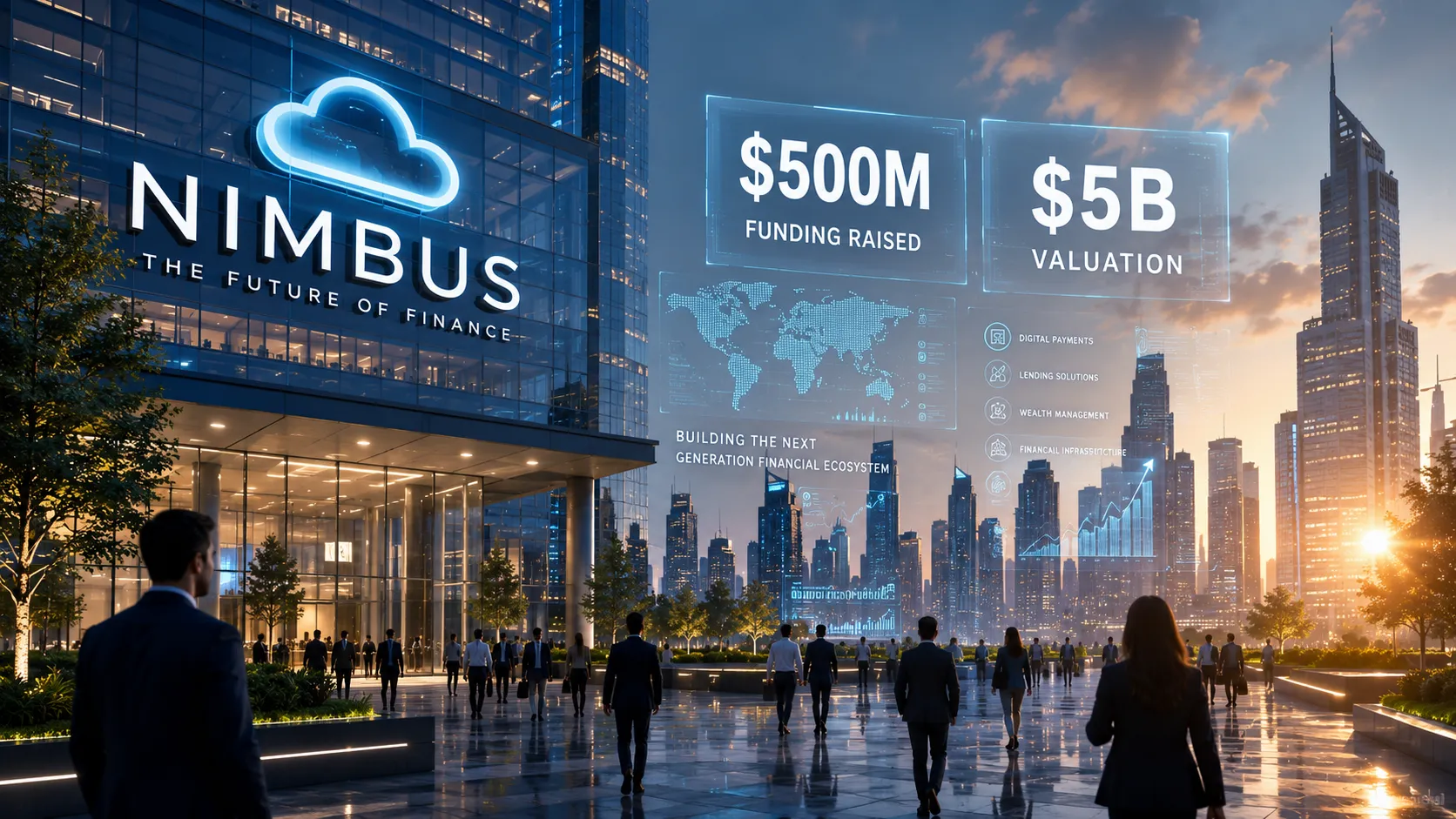

In a year when venture capital has been anything but predictable, one startup just proved that the freelance economy is still red hot. Nimbus, a neo‑banking platform built specifically for freelancers and gig workers, has raised $500 million in a Series D round led by Sequoia Capital and Stripe, catapulting the company to a $5 billion valuation. The round also included participation from Andreessen Horowitz, Shopify, and existing backer Tiger Global. It is one of the largest fintech raises of 2026 and a clear signal that investors are betting big on the future of work.

Nimbus now serves over 5 million freelancers across 30 countries. Its product suite includes a checking account, debit card, invoicing, automated tax withholding, and cross‑border payments in 40 currencies. Revenue grew 300% year‑over‑year to $120 million, and the company says it will reach profitability by Q4 2027. The new funding will be used to expand into Latin America and Southeast Asia, where freelance work is growing at 40% annually.

Unlike traditional neobanks that chase mass‑market consumers, Nimbus has carved out a narrow but deep moat: the 1.5 billion freelancers worldwide, according to World Bank estimates. These workers are often underserved by traditional banks, which struggle to underwrite income that comes from multiple platforms and in multiple currencies. Nimbus solves this with an API‑first approach that integrates directly with freelance marketplaces. A freelancer on Upwork, for example, can see their Nimbus balance and move money without ever leaving the Upwork interface. The same goes for Fiverr, Uber, DoorDash, and 50 other platforms.

“We’re building the financial operating system for the independent economy,” said Nimbus CEO and co‑founder Anjali Mehta in an interview. “Freelancers shouldn’t have to wait 30 days for payment, pay 5% in currency conversion fees, or spend weekends doing their own taxes. We automate all of that.”

The Stripe investment is particularly strategic. Under the new partnership, Nimbus will become the default payout partner for Stripe Connect in 12 countries, including India, Brazil, and Mexico. That means millions of sellers on Stripe‑powered platforms will automatically be offered a Nimbus account when they sign up. It’s a distribution channel that would have taken Nimbus years to build on its own. Stripe’s own Treasury product is similar, but Stripe has chosen to back Nimbus rather than compete head‑on – a sign of confidence in the startup’s execution.

Sequoia partner Roelof Botha, who led the round, said: “Nimbus has the potential to become the operating system for freelance work. The team has built a product that freelancers genuinely love, and the unit economics are already best‑in‑class. We’re thrilled to double down.”

The numbers back him up. Nimbus’s customer acquisition cost is $12, while the average customer generates $45 in annual revenue – a 3.75x payback in under four months. The debit card interchange alone contributes 40% of revenue. The rest comes from currency conversion fees (2% on international transfers), premium features (like instant payouts for a 1% fee), and a forthcoming lending product that will offer advances against outstanding invoices at a 2% flat fee.

The lending product is a key part of the growth story. Freelancers often face “feast or famine” cash flow – paid $5,000 today, nothing for the next 45 days. Nimbus will allow them to borrow against unpaid invoices at rates far lower than credit cards. The company has secured a $1 billion credit facility from Goldman Sachs to fund the loans.

Competitors are taking notice. Payoneer, a public company with a $2 billion market cap, has long served cross‑border freelancers but lacks Nimbus’s modern API integrations. Deel, a $12 billion unicorn focused on global payroll for remote employees, is moving downstream into freelancer payments. And traditional banks like JPMorgan are piloting “gig economy” accounts. But Nimbus’s first‑mover advantage and deep integrations give it a head start.

The Series D round also includes a secondary component: early employees and angel investors sold $100 million worth of shares, providing liquidity while keeping the company’s primary focus on growth. “We wanted to reward the team that built Nimbus from nothing,” said Mehta. “No one should have to wait for an IPO to buy a house.”

Nimbus was founded in 2019 by Anjali Mehta and Rohan Desai, both former Stripe employees who saw firsthand how complex cross‑border payments were for creators. The company bootstrapped for two years, then raised a $10 million Series A in 2021. The Series B ($50 million at a $500 million valuation) and Series C ($150 million at a $1.8 billion valuation) followed in quick succession. The latest round values the company at nearly triple its previous valuation, despite a challenging macro environment.

The expansion into Latin America and Southeast Asia will be Nimbus’s first major test outside its core markets of North America and Europe. In Brazil, for example, over 15 million people work as freelancers, but few have access to US dollar accounts. Nimbus will offer a multi‑currency wallet that allows them to hold, exchange, and withdraw in Brazilian reais, dollars, and euros. Local partnerships with Brazilian fintechs and banks are already in place.

The company also plans to launch a “freelancer credit score” that aggregates income data from multiple platforms to help users qualify for mortgages and car loans – products that are currently out of reach for most gig workers. It’s a bold vision, and it will require careful regulatory navigation. But Nimbus has already obtained money transmitter licenses in 48 US states and is applying for banking charters in the UK and Australia.

Not everyone is bullish. Critics point out that Nimbus’s revenue is still heavily dependent on interchange fees, which could be pressured if regulators cap debit card fees. The company also faces execution risk as it scales to new countries with different regulatory regimes. And the lending product is unproven; default rates could spike if the economy turns.

Mehta acknowledges the risks but remains confident. “The freelance economy is not going away. If anything, it’s accelerating. Our job is to build the financial rails that make it work for everyone – the freelancer in Bangalore, the graphic designer in Buenos Aires, the driver in Detroit. That’s a multi‑trillion‑dollar opportunity.”

For now, the $500 million check gives Nimbus a long runway. The company plans to double its headcount from 400 to 800 by the end of 2027, with most new hires in engineering and compliance. It will also open offices in São Paulo, Jakarta, and Nairobi.

As the Series D announcement hit the wires, Nimbus’s app saw a 40% spike in new signups – most of them word‑of‑mouth. One freelancer tweeted: “I’ve been using Nimbus for two years. They’ve never let me down. This funding means they’re not going anywhere. Finally, a bank that works for us.”

The freelance economy has long been the underdog of financial services. With Nimbus, that story is being rewritten. The operating system for the independent worker is coming online, and it just got a $500 billion vote of confidence.