A 19.2% rise in platform fees for Zomato is bad PR. An 8% market share in UPI for Paytm is a crisis. In 2021, Paytm was synonymous with 'Digital India'. Today, it's the awkward third wheel in a wedding between Google and Walmart. How did the first-mover advantage evaporate so completely? The answer is a masterclass in how to lose a market you created.

There was a time when "Paytm Karo" was a verb. It was the default—like Xerox for photocopies, or Google for searches. In the immediate aftermath of the 2016 demonetization, Paytm was the heartbeat of Indian fintech. The company's ubiquitous green and white QR codes were plastered on every chai stall, every vegetable cart, every kirana store from Kashmir to Kanyakumari. It was the poster child of India's digital payments revolution, and its founder Vijay Shekhar Sharma was its fiery, unapologetic face.

Fast forward to April 2026, and the pulse is barely detectable.

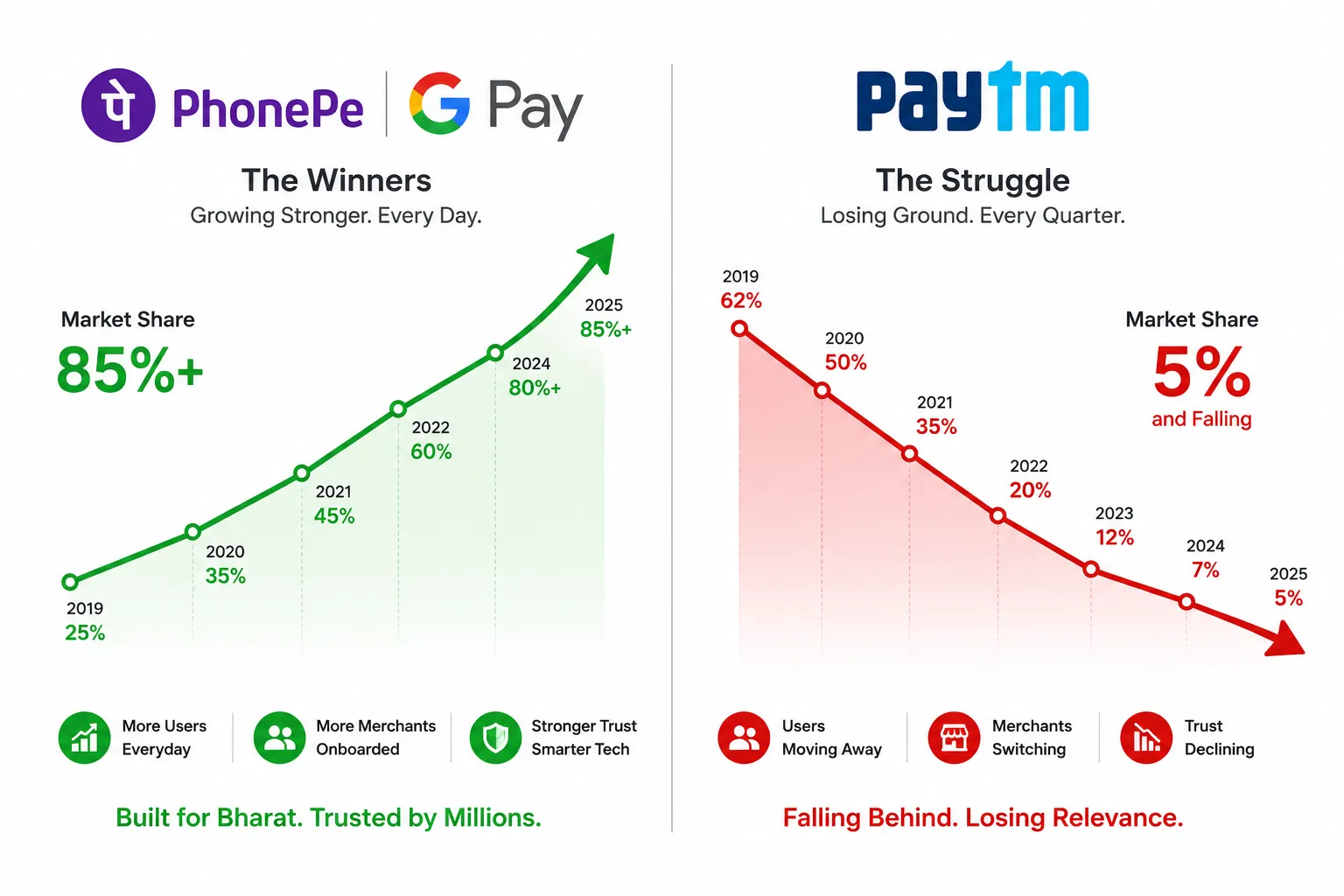

The National Payments Corporation of India (NPCI) released its monthly UPI data for April 2026, and the numbers painted a grim picture for the company that once dominated the ecosystem. Paytm processed roughly 1.77 billion transactions, representing a market share of just 8.10%. This is Paytm's lowest watermark in over four years. For context, at its peak in early 2020, Paytm controlled over 35% of the UPI market. The company has lost more than three-quarters of its relative market share in just six years.

So, where did the users go? They migrated to the duopoly. Walmart-backed PhonePe now commands a staggering 46%+ market share, while Google Pay sits comfortably at around 33.5%. Together, these two American-backed titans control almost 80% of India's UPI ecosystem. Paytm isn't just losing; it's being squeezed out of existence by a pincer movement of American capital and aggressive merchant acquisition. The third spot, which once belonged to Paytm with pride, has been relegated to a distant, almost irrelevant also-ran.

The decline has been dramatic and multifaceted. In early 2024, the Reserve Bank of India (RBI) delivered a body blow to the company by imposing severe restrictions on Paytm Payments Bank, effectively barring it from accepting fresh deposits, conducting credit transactions, and onboarding new customers. While the company scrambled to comply and pivot to third-party banking partners like Axis Bank, the damage to consumer trust was already done. Users, unsure if their money was safe, switched to the more "stable" alternatives offered by Google and PhonePe. The trust, once Paytm's greatest asset, never fully returned.

The cashback wars have been the final nail in the coffin. PhonePe, fueled by Walmart's deep pockets, and Google Pay, backed by Alphabet's limitless treasury, have been aggressively subsidizing merchant discounts and user cashbacks. Every time a user scans a QR code, they are bombarded with offers: "5 rupees cashback on PhonePe," "10 rupees off on Google Pay." Paytm, which has struggled to turn a consistent profit and has never had the luxury of a bottomless corporate war chest, simply cannot afford to burn cash at the same rate. Every time a Paytm user switches to PhonePe for a 5-rupee cashback on a chai purchase, another tiny piece of Paytm's user base erodes.

The merchant network battle is equally brutal. PhonePe and Google Pay have been aggressively deploying armies of sales agents to sign up small retailers exclusively. They offer subsidized QR code stickers, free soundboxes, and even small cash incentives to merchants who agree to display their QR code more prominently than competitors. Paytm, once the undisputed king of merchant acquisition, is being outflanked in its own territory. The result is a vicious cycle: fewer users mean fewer merchants want to use Paytm; fewer merchants mean fewer users want to open Paytm. The network effects that once worked in Paytm's favor are now working against it.

But is there a strategy behind the fall? Some analysts argue that Paytm is deliberately retreating from the low-margin UPI battlefield to focus on the higher-yield "Super App" strategy—offering wealth management, loans, and insurance. The theory is that UPI is a loss-leader, and Paytm is sacrificing volume for value. Sharma himself has hinted at this, telling employees in a recent town hall: "We are not competing for the 10-rupee transaction. We are competing for the 10,000-rupee financial relationship."

However, that argument only holds water if the user stays on the platform. If users are leaving the Paytm ecosystem entirely—because they open PhonePe for payments and stay there for investments—then Paytm is hemorrhaging the data and engagement it needs to cross-sell high-margin products. A user who doesn't open the Paytm app is a user who won't see the wealth management offer, the loan advertisement, or the insurance policy. The entire cross-sell strategy collapses without an active user base.

The stock market has already delivered its verdict. Paytm's share price, which debuted at a disastrous IPO in 2021, has tanked further in 2026, hitting record lows. Investors are betting that Paytm will be relegated to a niche player, or worse, acquired for pennies on the dollar by a competitor looking to scoop up its remaining user base. The company's market capitalization has evaporated by over 80% from its peak, a staggering destruction of shareholder value.

The company's response has been a mix of denial and desperate action. Paytm has launched new features, including a dedicated merchant app and enhanced lending products. It has also been aggressively marketing its soundbox and card machine offerings to retain its merchant base. But these moves seem reactive rather than strategic, a series of last-ditch efforts to slow an inexorable decline.

Vijay Shekhar Sharma, however, remains defiant. In a recent town hall, he reportedly told employees: "We have been counted out before. We will be counted out again. But we are still standing. We are still fighting. This is not the end of Paytm. This is the end of the beginning." It's a bold, noble vision. But in the brutal world of Indian fintech, you can't have a 10,000-rupee relationship if your user has already deleted your app and moved on.

The question now is not whether Paytm can regain its former glory—that ship has almost certainly sailed. The question is whether Paytm can survive at all. Can it carve out a profitable niche in the lending and wealth management space before its UPI user base erodes to irrelevance? Or will it become a cautionary tale of how first-mover advantage, squandered through regulatory missteps and a failure to match the firepower of global giants, can turn a national champion into a distant third?

One thing is certain: the days of Paytm as the undisputed king of Indian payments are over. The king is dead. Long live the new kings. And they are American.