Ask most people to name the Tata Group's most valuable business, and the answer will come quickly and confidently: Tata Consultancy Services, the information technology services giant that has anchored the conglomerate's market value for years and become, in the process, one of the most recognizable Indian brands in global enterprise software and consulting. Ask the same people to name the group's second most valuable company, and the confidence tends to evaporate. Few would guess correctly that the answer is Titan Company — a business that began its life selling wristwatches, and now commands a market capitalization approaching ₹3.6 lakh crore.

That gap between Titan's actual financial significance and its comparatively modest public profile is, in its own way, the whole story worth telling here. Titan has spent decades building one of Indian corporate history's more instructive reinvention narratives largely out of the media spotlight that tends to follow India's more conspicuously dramatic business stories — the Ambani-Adani wealth rivalry, the high-profile startup unicorns, the headline-grabbing mergers and acquisitions that dominate the business press week after week. Titan's rise has been quieter, slower, and in many respects more difficult to replicate precisely because it depended on decades of patient category expansion rather than any single transformative deal or founder-led bet made in a single dramatic moment.

A Modest Beginning

Titan's origin story is, by the standards of India's largest companies, almost deliberately unglamorous. It began as a joint venture aimed at bringing quartz watch technology to the Indian market at a time when the country's watch industry was dominated by older, less precise mechanical technology and largely served by a fragmented landscape of smaller manufacturers. The bet was narrow and specific: that Indian consumers, as disposable incomes rose, would be willing to pay a premium for more accurate, more reliably manufactured time

pieces bearing a trusted brand name — in this case, the Tata name, already associated with quality and reliability across the group's other businesses.

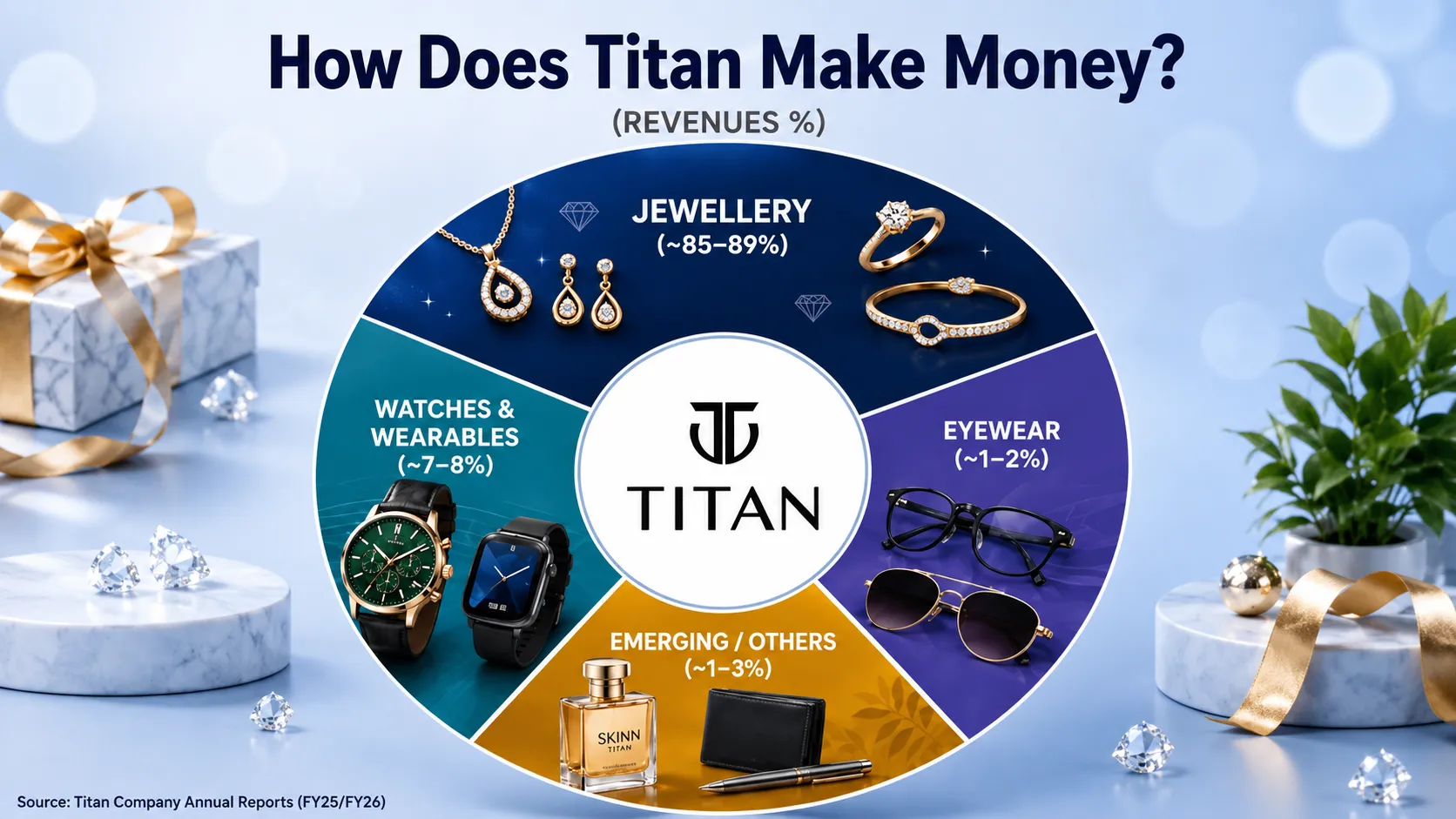

That narrow initial bet on watches proved durable enough to establish Titan as a credible consumer brand, but it was the subsequent, deliberate decision to expand well beyond watches — into jewellery, eyewear, and eventually fragrances — that transformed Titan from a successful niche manufacturer into one of India's most valuable diversified consumer businesses. Each expansion followed a similar underlying logic: identify a category where Indian consumers were underserved by fragmented, often unreliable local competition, and bring the same combination of trusted branding, consistent quality, and organized retail presence that had worked for watches into an entirely new product line.

Tanishq and the Jewellery Bet

Of Titan's category expansions, none has proven more consequential than its move into jewellery through the Tanishq brand. India's jewellery market, dominated for generations by small, often family-run local jewellers operating with limited standardization around purity, pricing transparency, and design consistency, represented an enormous and largely untapped opportunity for an organized retail player willing to bring the same trust-building playbook that had worked in watches to a category with far larger transaction values and far deeper cultural and emotional significance for Indian consumers, for whom jewellery purchases are frequently tied to weddings, religious festivals, and other major life events.

That bet required years of patient investment before it began paying off at scale, in part because jewellery purchases in India carry an unusually heavy weight of family tradition, trust, and often multi-generational relationships with specific local jewellers that a new entrant, however well-capitalized, could not simply purchase or replicate overnight. Tanishq's eventual success in building a genuinely national, trusted jewellery brand — one now significant enough to move Titan's overall financial results meaningfully — stands as one of the more remarkable examples in Indian retail history of an organized, professionally managed brand successfully displacing entrenched, deeply trusted local incumbents across an enormous and culturally significant product category.

Growth Without a Founder's Name Attached

Titan's trajectory offers a useful counterpoint to the kind of business story that typically dominates Indian financial media coverage. Where Reliance Industries and the Adani Group grew substantially through founder-led aggression — rapid diversification, enormous individual capital commitments, and, in Reliance's case, entirely new business lines built from scratch under Mukesh Ambani's direct personal direction — Titan's rise has been comparatively unglamorous: patient, professionally managed category expansion inside a large conglomerate, without any single founder-owner whose personal net worth tracks the company's share price the way Ambani's or Adani's does.

That distinction matters enormously for how India's business press tells its wealth and success stories. A conglomerate-owned success story like Titan rarely produces the kind of individual net-worth headline that a Hurun or Forbes rich list depends on for its own narrative appeal, even when the underlying business achievement — turning a modest watch venture into one of India's most valuable listed companies — is every bit as remarkable in its own right as any founder-led empire. Titan's success belongs, in a meaningful sense, to a professional management team and to the broader Tata Group ecosystem rather than to any single identifiable individual, which may partly explain why its ₹3.6 lakh crore milestone generated comparatively modest coverage relative to its genuine financial significance.

Navigating a Difficult Moment for Indian Industry

Titan's current spotlight arrives at a moment when Indian industry more broadly is navigating considerable turbulence: volatile commodity prices affecting input costs across manufacturing and retail, shifting consumer behavior as spending patterns evolve amid economic uncertainty, and broader geopolitical disruptions to global energy markets and supply chains that have forced Indian companies across sectors to balance growth ambitions against genuine near-term uncertainty. Against that backdrop, Titan's steady long-term reinvention has been held up as something of a model — evidence that patient, category-by-category expansion, sustained over decades rather than compressed into a handful of dramatic strategic moves, can produce financial outcomes that rival or exceed the more headline-grabbing growth strategies pursued elsewhere in Indian industry. Precious metal prices in particular have swung considerably over the past several years, a variable that directly affects Titan's jewellery margins and inventory costs, and the company's ability to navigate that volatility without abandoning its long-term brand-building strategy has itself become a case study cited approvingly by analysts covering the broader Indian retail sector.

That framing has taken on additional significance this year as Indian business media has increasingly turned its attention toward questions of corporate sustainability and long-term resilience, rather than focusing exclusively on quarterly growth figures or short-term market movements. Titan's evolution — from a single-category manufacturer into a genuinely diversified consumer lifestyle business spanning multiple product categories, each contributing meaningfully to overall revenue rather than depending on any single dominant business line — offers a template for the kind of diversified resilience that many Indian companies are now actively trying to build into their own long-term strategies, particularly as global trade tensions and commodity price volatility make single-category dependence an increasingly risky proposition.

What Titan's Milestone Actually Signals

It would be easy to read Titan's ₹3.6 lakh crore market capitalization purely as a financial statistic, another entry in the ongoing scorecard of which Indian companies are worth the most on any given trading day. The more useful reading treats the milestone as evidence of something considerably harder to achieve than a single blockbuster year of growth: sustained relevance across multiple consumer categories and multiple economic cycles, built through a management approach that prioritized patient brand-building over the kind of rapid, headline-generating expansion that characterizes many of India's most closely watched corporate growth stories.

It is also worth noting how Titan's ascent has reshaped the internal hierarchy of the Tata Group itself, a conglomerate whose various businesses have historically taken turns as the group's most closely watched growth story. For years, that role belonged almost exclusively to Tata Consultancy Services, whose scale and global enterprise relationships made it the obvious flagship whenever analysts discussed the group's overall trajectory. Titan's rise to become the group's second most valuable company represents a meaningful diversification of where the Tata Group's financial strength actually resides — no longer concentrated almost entirely in information technology services, but increasingly distributed across a genuinely diversified portfolio spanning software, consumer retail, and beyond, a structural resilience that may prove increasingly valuable as different sectors face different cyclical pressures at different times.

A Story Without a Singular Hero

Perhaps the most instructive thing about Titan's rise is precisely what it lacks: a singular founder whose personal biography can be woven into the company's success story the way Mukesh Ambani's biography is woven into Reliance's, or Gautam Adani's into the Adani Group's. Titan's story belongs instead to a succession of professional managers, brand-builders, and category strategists working within the broader institutional framework of the Tata Group — a conglomerate whose various businesses collectively span software services, steel, automobiles, hospitality, and now, through Titan, watches and jewellery, without concentrating identity or narrative around any single dominant personality.

That institutional character connects to a broader feature of how the Tata Group as a whole has historically operated, distinguishing it from many of India's other major business houses. Where several of India's largest conglomerates remain closely identified with the founding family that continues to hold significant ownership stakes and exercise direct strategic control, Tata Sons has, for decades, operated under a governance structure that places genuine authority in the hands of professional boards and chief executives, with the Tata family's own direct ownership stake considerably diluted relative to the group's total value. Titan's success is, in that sense, a demonstration of what that governance model can produce when executed patiently over multiple decades: a business capable of world-class category-by-category expansion without requiring the kind of singular, founder-driven vision that dominates the popular imagination of what makes an Indian business great.

Lessons for the Next Generation of Indian Retail

Titan's playbook — identify a category where Indian consumers are underserved by fragmented, often unreliable local competition, then bring organized retail discipline, consistent quality, and trusted branding to that category over a sustained multi-year investment horizon — has become something of a template that other Indian consumer businesses have consciously or unconsciously followed in the years since Titan first proved it could work at scale. The playbook is not unique to Titan; it echoes strategies pursued across organized retail, from supermarket chains displacing neighborhood kirana stores to organized furniture and home goods retailers displacing fragmented local carpenters and craftsmen. What distinguishes Titan is the sheer scale and duration over which it has successfully executed that playbook, first in watches, then far more consequentially in jewellery, and now across eyewear and fragrances as well.

For younger Indian consumer companies studying Titan's trajectory closely, the most transferable lesson may be less about any specific category choice and more about the underlying patience the strategy demands from investors, management, and boards alike. Tanishq's jewellery business did not become a meaningful contributor to Titan's overall financial results overnight; it required years of sustained investment in brand-building, retail footprint expansion, and the slow, difficult work of earning consumer trust in a category where trust had traditionally been built through multi-generational relationships with local jewellers rather than through national advertising campaigns or organized retail chains. That kind of patience is difficult to sustain in an investment climate that often rewards faster, more dramatic growth narratives, which may be precisely why Titan's reinvention, however successful, has rarely received the same attention as India's more headline-friendly business stories.

Whatever comes next for Titan — further category expansion, continued growth in its existing jewellery and watch businesses, or new strategic bets not yet publicly disclosed — the company's ₹3.6 lakh crore milestone stands as a reminder that India's most consequential business stories do not always announce themselves with the drama of a rich-list ranking or a headline-grabbing acquisition. Sometimes they accumulate quietly, decade after decade, until a single market-capitalization figure forces even casual observers to notice what patient, professionally managed reinvention can eventually build, long after the original bet on quartz watches has faded into little more than a footnote in the company's much larger and much more valuable present-day story.