For anyone tracking India's currency markets over the past several weeks, the story has been one of near-relentless pressure on the rupee, which has repeatedly tested fresh lows against the US dollar as an unusually stubborn combination of elevated crude oil prices, foreign portfolio outflows, and geopolitical uncertainty in West Asia has combined to weigh on the domestic currency. The rupee's slide is not an isolated event but rather the latest chapter in a months-long saga that traces its roots directly back to the closure of the Strait of Hormuz, one of the world's most critical maritime chokepoints for global energy trade.

**Tracking the recent slide**

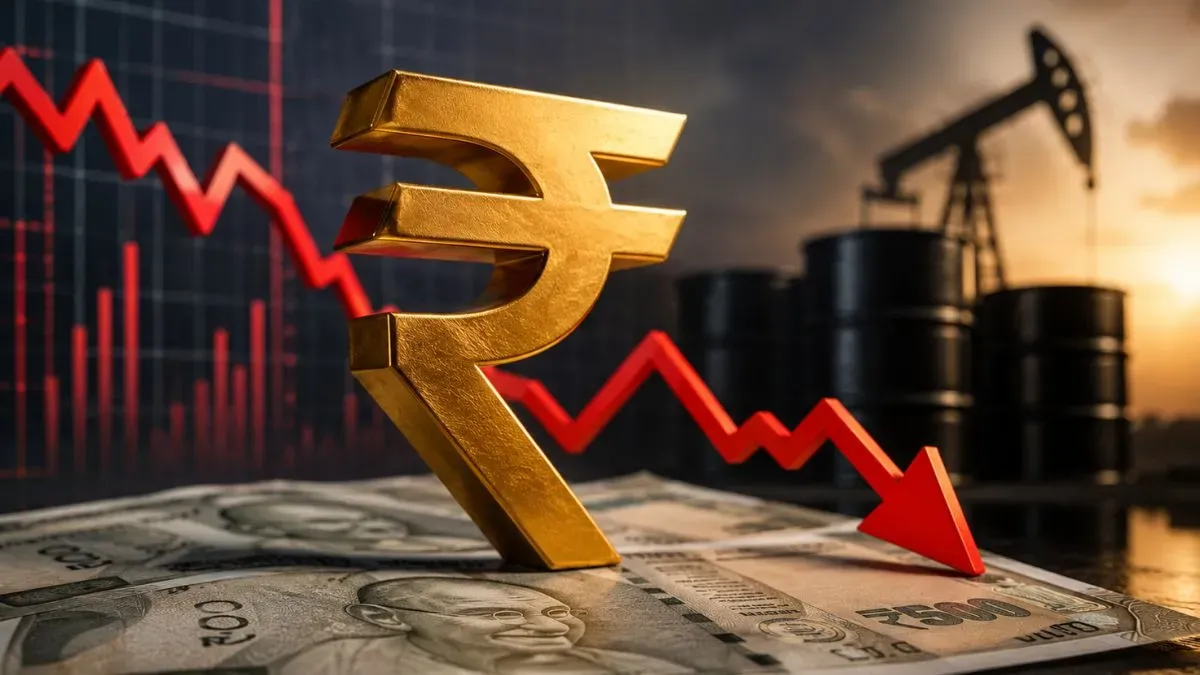

In the most recent trading sessions tracked by currency markets, the rupee depreciated 62 paise to close near 96.30 against the US dollar, opening at 95.95 before settling lower amid a fresh surge in crude oil prices and renewed geopolitical concerns. This continued a pattern that has played out repeatedly over recent weeks: the USD/INR pair posting fresh multi-week highs as surging oil prices and elevated US Treasury yields — themselves a reaction to the United States asserting a right to levy toll fees on vessels transiting the Strait of Hormuz — have collectively weakened the appeal of the Indian currency relative to the dollar. On the commodities side, MCX Crude Oil contracts have traded sharply higher, at one point opening more than 4 percent up to touch the highest levels seen in almost a month, a move that directly amplifies pressure on currencies of oil-importing economies like India that rely heavily on imported crude to meet domestic energy needs.

**Why oil prices move the rupee so directly**

The mechanical relationship between crude oil prices and the rupee's exchange rate is one of the more consistently reliable dynamics in Indian macroeconomics, and it is worth spelling out clearly for readers less familiar with currency market mechanics. India imports the vast majority of its crude oil requirements, meaning that every dollar increase in the price of a barrel of crude translates into a proportionally larger outflow of dollars required to pay for the country's energy imports. This dynamic widens India's trade deficit, increases demand for dollars in the domestic foreign exchange market relative to the supply of rupees being exchanged for dollars, and — all else being equal — pushes the rupee weaker against the dollar. When oil price spikes are sudden and sustained, as has been the case since the Strait of Hormuz closure disrupted a meaningful share of global crude flows, the resulting currency pressure tends to be correspondingly sharp and difficult for the Reserve Bank of India to fully offset through routine market interventions.

**The scale of foreign capital flight**

Compounding the oil-driven pressure has been a wave of foreign portfolio outflows from Indian equities that has, at various points earlier in 2026, already surpassed prior full-year outflow records. Foreign investors pulled more than $20 billion from Indian equities within just the first four months of 2026 alone, according to earlier tracking of the crisis, a pace of withdrawal that reflects how sensitive global institutional capital has become to the compounding effects of currency depreciation risk, elevated energy costs, and broader geopolitical uncertainty weighing on emerging market assets generally. When foreign investors sell Indian equities and repatriate the proceeds back into dollars or other currencies, that selling activity itself adds further downward pressure on the rupee, creating a reinforcing cycle that can be difficult to break without either a fundamental improvement in the external environment or decisive policy intervention.

**Oil marketing companies caught in the middle**

Perhaps the most immediate and consequential domestic impact of this currency and crude oil dynamic has fallen on India's oil marketing companies, the state-run entities responsible for refining and distributing petroleum products to consumers across the country. With the government keeping retail pump prices artificially suppressed to shield ordinary consumers from the full pass-through of elevated global crude costs, oil marketing companies have reportedly been absorbing losses estimated at up to ₹1,000 crore per day at the peak of the crisis — an unsustainable burn rate that economists have repeatedly warned cannot continue indefinitely without either fiscal support from the government, a moderation in global crude prices, or an eventual, politically difficult decision to raise retail fuel prices and pass at least part of the cost increase on to consumers.

**What economists are saying about the path ahead**

Economists tracking the situation have been fairly consistent in their assessment that some combination of fuel price hikes and continued rupee weakness is likely if the underlying Strait of Hormuz disruption persists. Analysts have pointed out that neither the government's fiscal buffers nor the balance sheets of oil marketing companies are deep enough to indefinitely absorb the current scale of losses, suggesting that a retail fuel price adjustment becomes increasingly likely the longer the Middle East conflict continues to disrupt global energy supply chains. India's broader GDP growth forecast has also come under pressure as a result, with projections for fiscal year 2026/2027 growth slowing to around 6.7 percent, down from the considerably stronger 7.7 percent pace recorded in the prior year — a deceleration that analysts attribute directly to the compounding drag of elevated energy costs, currency weakness, and the broader uncertainty the crisis has injected into business investment decisions across multiple sectors of the economy.

**The Reserve Bank of India's balancing act**

Throughout this period of sustained currency pressure, the Reserve Bank of India has faced an increasingly delicate balancing act in calibrating its monetary and foreign exchange policy response. Direct intervention in the foreign exchange market — selling dollars from its reserves to support the rupee — remains one of the RBI's primary tools for managing excessive currency volatility, but sustained intervention of this kind draws down the country's foreign exchange reserves, a buffer that policymakers are generally reluctant to deplete too aggressively given the importance of maintaining adequate reserves as a signal of financial stability to international investors and credit rating agencies. On the interest rate front, the central bank has generally maintained a cautious, steady policy stance, balancing the inflationary pressure coming from elevated oil-driven import costs against the risk that further monetary tightening could compound the drag on an already slowing growth trajectory.

**How the rupee's weakness ripples through the broader economy**

The consequences of sustained rupee depreciation extend considerably beyond the immediate foreign exchange market itself, rippling through nearly every corner of the Indian economy. Imported inflation is perhaps the most direct channel: as the rupee weakens, the domestic price of anything India imports — from crude oil and edible oils to electronics components and certain industrial inputs — rises correspondingly, adding to overall consumer price pressures at a moment when the RBI is already navigating a delicate inflation-growth trade-off. Corporates with significant dollar-denominated debt or import-heavy supply chains face rising costs that can compress margins unless they are able to pass those costs through to end consumers, a pass-through that itself contributes to broader inflationary pressure. On the other hand, a weaker rupee does offer some offsetting benefit to India's export-oriented sectors, including IT services and certain manufacturing exporters, whose dollar-denominated revenues translate into more rupees when repatriated — though this benefit has, in the current environment, generally been overshadowed by the broader drag from elevated energy import costs across the wider economy.

**A currency story tied to a geopolitical resolution**

Ultimately, market participants tracking the rupee's trajectory have converged on a fairly consistent view: the currency's near-term path is likely to remain closely tethered to developments in the Strait of Hormuz situation rather than to purely domestic economic factors. Periods when shippers have reported partial reopening or easing of restrictions through the Strait have historically coincided with brief rupee recoveries, only for renewed tensions or fresh disruptions to push the currency back toward weaker levels. This pattern underscores just how directly India's currency markets have become hostage to a geopolitical situation unfolding thousands of miles away, a reminder of the country's continued structural vulnerability to global energy shocks even as it has spent the past decade building out renewable energy capacity and diversifying its import sources. Until there is a durable resolution to the Hormuz disruption — whether through diplomatic de-escalation, alternative shipping route arrangements, or a broader normalisation of the underlying regional conflict — the rupee is likely to remain one of the more closely watched and volatile major emerging market currencies through the remainder of 2026.

**How the rupee compares to regional peers**

One useful lens for assessing the severity of the rupee's recent decline is to compare its performance against other major emerging market and Asian currencies navigating the same global environment of elevated oil prices and dollar strength. Currency strategists have periodically noted that the rupee has, at various points over the past year, underperformed several of its Asian peers on a real effective exchange rate basis, a divergence attributed in part to India's particularly heavy dependence on imported crude relative to some regional neighbours with more diversified energy import baskets or greater domestic production capacity. This relative underperformance has occasionally prompted views among currency analysts that the rupee's overvaluation on certain metrics had been meaningfully corrected through the recent depreciation cycle, with some strategists suggesting the currency should, over a longer horizon, track more closely with broader Asian currency movements — including the Chinese yuan — once the acute phase of the current oil price shock eventually passes.

**The equity-currency feedback loop**

A particularly important dynamic for retail and institutional investors alike to understand is the tight, self-reinforcing feedback loop that has developed between rupee weakness and Indian equity market performance during this period. As the currency depreciates, foreign investors holding rupee-denominated Indian equities see the dollar value of their holdings erode even before accounting for any change in the underlying stock prices themselves — a dynamic that can accelerate selling pressure among foreign portfolio investors seeking to limit further currency-driven losses, which in turn adds to the very equity outflows that contribute to additional rupee weakness. Breaking this cycle typically requires either a clear signal of currency stabilisation, which can encourage foreign investors to view rupee-denominated assets as attractively valued again, or sufficiently compelling equity market fundamentals — such as strong corporate earnings growth — to offset investors' currency-related concerns. This quarter's mixed but broadly resilient corporate earnings season, including strong results from bellwethers like Reliance Industries, may offer some counterbalancing support to foreign investor sentiment even as the currency itself remains under pressure.

**What everyday Indians can expect**

For ordinary households and businesses less directly engaged with currency and equity markets, the practical implications of sustained rupee weakness are likely to show up gradually but tangibly across household budgets over the coming months. Beyond the direct impact on fuel prices, a weaker rupee tends to push up the cost of a wide range of imported goods, from consumer electronics and certain pharmaceutical inputs to edible oils and other commodities India imports in bulk. Households with members working abroad or receiving remittances may see some offsetting benefit, as remittances denominated in stronger foreign currencies convert into more rupees — though this benefit has, during the current episode, been complicated by reports of reduced business activity and disruptions across parts of the Gulf region directly affected by the broader regional conflict, which has weighed on remittance flows even as the currency conversion rate itself has moved favourably for those still able to send money home.

**Sectors positioned to benefit versus those under pressure**

Not every corner of the Indian economy experiences rupee weakness identically, and understanding this divergence helps explain why market reaction to currency moves is rarely uniform across sectors. India's large IT services exporters, along with pharmaceutical companies with substantial US and European export revenue, have historically been among the more direct beneficiaries of rupee depreciation, since their dollar-denominated revenues translate into a larger rupee sum upon repatriation, providing a natural earnings tailwind even as their domestic cost base remains largely rupee-denominated. Conversely, sectors with heavy import dependence — including oil marketing companies, gold and jewellery retailers, electronics assemblers, and airlines that pay for jet fuel and aircraft leases substantially in dollars — tend to see margins compressed as the same volume of imports now costs more in rupee terms. For a diversified economy like India's, this divergence means that currency weakness, while broadly disruptive, does not translate into uniformly negative outcomes across every listed company or sector, a nuance investors are likely to continue weighing carefully as they position portfolios through the remainder of this volatile currency cycle.