NEW DELHI, June 1, 2026 — The Indian government has revised export duties on petrol, diesel, and aviation turbine fuel (ATF) for the fortnight beginning June 1, marking the latest recalibration since the SAED/RIC mechanism was activated on March 27, 2026. The move reflects a moderation in global gasoline crack spreads — and a carefully calibrated political strategy to protect 1.4 billion consumers from a 50%-plus surge in global crude prices, while the nation's three state-run Oil Marketing Companies silently absorb losses of a scale not seen since the subsidy era.

The revised rates — Rs 1.5/litre on petrol, Rs 13.5/litre on diesel and Rs 9.5/litre on ATF — represent a significant reduction from the levels imposed two fortnights prior. Analysts warn the recalibration does little to address the structural haemorrhage in OMC finances, now estimated at a combined Rs 1 lakh crore since the crisis began.

“Export levies were introduced to ensure domestic availability by disincentivising exports in the backdrop of the West Asia crisis.” — Ministry of Finance, June 1, 2026 |

How We Got Here: The Timeline

India's export duty mechanism for petroleum products is the latest evolution of a playbook first deployed in July 2022. What makes 2026 qualitatively different is the geopolitical trigger, the scale of OMC losses, and the speed of policy recalibration.

The March 27 Shock

When the West Asia crisis escalated in late February 2026, Brent crude crossed $100/barrel in early March and continued climbing above $120. The government's response on March 27 was swift: a Rs 10/litre cut in central excise duty on petrol and diesel for domestic consumption, coupled with export levies of Rs 21.5/litre on diesel and Rs 29.5/litre on ATF.

The Fortnightly Review Mechanism

The SAED/RIC mechanism is explicitly linked to average international prices since the last review. The June 1 revision, which slashed the Road Infrastructure Cess to zero across all three fuels while reducing SAED rates, reflects international gasoline crack spreads narrowing.

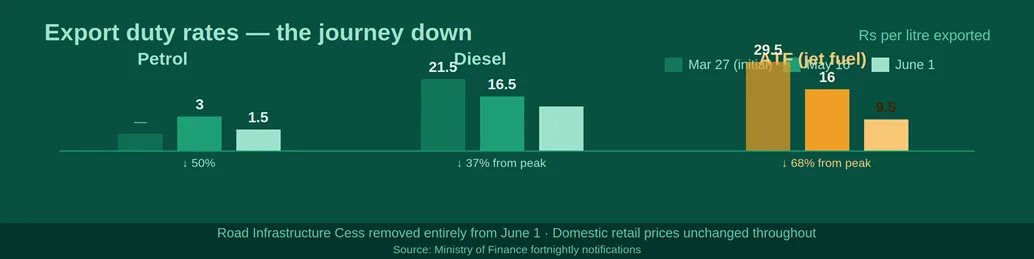

The Numbers: Revised Duty Rates at a Glance

The following table summarises the evolution of export levies since the mechanism was introduced:

Fuel | Mar 27 (initial) | May 16 | June 1 | Net change |

Petrol | — | Rs 3/L | Rs 1.5/L | ↓ 50% |

Diesel | Rs 21.5/L | Rs 16.5/L | Rs 13.5/L | ↓ 37% |

ATF (jet fuel) | Rs 29.5/L | Rs 16/L | Rs 9.5/L | ↓ 68% |

Road Infra Cess | Applied | Applied | Nil | Removed |

Note: Removal of the Road Infrastructure Cess signals the government views it as a temporary emergency measure, retaining SAED as the primary calibration lever going forward.

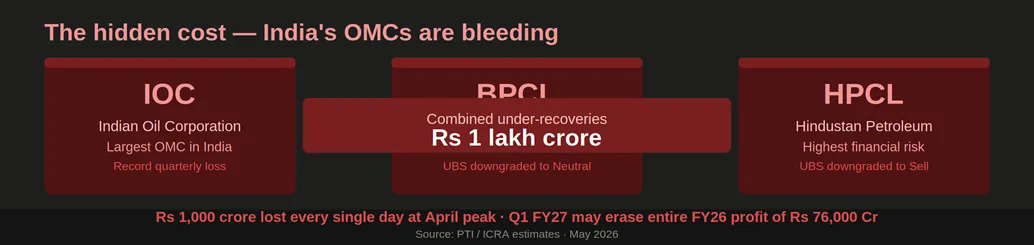

The Hidden Cost: India's OMCs Are Bleeding

The export duty story cannot be understood in isolation. It is inextricably linked to the financial catastrophe unfolding on the balance sheets of India's three state-run OMCs — IOC, BPCL, and HPCL.

Rs 1L Cr Estimated combined OMC losses since Mar 2026 | Rs 1,000 Cr Daily losses at peak (Apr 2026) | Rs 76,000 Cr Full FY26 profit — at risk of erasure in Q1 FY27 | 50%+ Surge in crude input costs since Feb 2026 |

At $123/barrel crude, the gap between production cost and permitted consumer price stood at Rs 15–30/litre on petrol and diesel. Daily combined losses were estimated by ICRA at Rs 1,000–1,200 crore at the April peak. UBS downgraded IOC and BPCL to 'Neutral' and HPCL to 'Sell' in March 2026, cutting FY27–28 marketing margin estimates by 43–45%.

The Reliance Anomaly

Reliance Industries' 35.2 million TPA Jamnagar SEZ refinery is legally exempt from SAED under the Special Economic Zones Act 2005. This means Reliance can continue exporting jet fuel and diesel duty-free, while state-run IOC, BPCL, and HPCL bear the full burden — a structural asymmetry that draws increasing scrutiny.

Energy Security in a Disrupted World

Nearly 90% of India's LPG supplies were previously routed through the Strait of Hormuz. While the government has secured crude inventories for two months forward and refineries are operating at full capacity, the fragility of India's energy supply chain is no longer theoretical.

The export duty mechanism serves a dual purpose: keeping refined product within India's borders during a supply emergency, and insulating domestic prices from full pass-through of global price spikes.

“The objective is to prioritise domestic availability of diesel and ATF and ensure energy security at a time of global uncertainty.” — Vivek Chaturvedi, Chairman CBIC — March 27, 2026 |

Stakeholder Impact Analysis

For Domestic Consumers

• Immediate impact: None. Domestic excise duty rates on petrol and diesel remain unchanged. Retail pump prices are unaffected by the June 1 revision.

• Risk horizon: If OMC losses continue accumulating without retail price correction or government compensation, a delayed but sharp price hike becomes increasingly unavoidable.

• Aviation passengers: Lower ATF export duties (Rs 9.5 from Rs 16) moderately improve airline economics and reduce pressure on airfare inflation.

For Oil Marketing Companies (IOC, BPCL, HPCL)

• Balance sheet stress: Combined losses approaching Rs 1 lakh crore threaten credit ratings, dividend sustainability and capital expenditure plans.

• Government support: FM Sitharaman has indicated OMC support through the budget mechanism, but quantum and timing remain unspecified, creating investor uncertainty.

For Private Refiners and Reliance Industries

• SEZ advantage: Reliance's Jamnagar SEZ refinery operates outside the export-duty net, preserving international competitiveness — a structural, legally grounded advantage that draws increasing scrutiny.

Outlook: Three Scenarios

Scenario A — Crude Eases, Crisis Normalises

If West Asia tensions de-escalate and Brent returns toward $85–90/barrel, the fortnightly mechanism would naturally unwind export duties toward zero, OMC under-recoveries would shrink, and the government could phase out SAED/RIC without a politically painful retail price hike.

Scenario B — Crude Stays Elevated, OMC Bailout Required

If crude holds above $110–120 and the price freeze continues into Q2 FY27, OMC losses will cross Rs 1.5–2 lakh crore. A combination of direct budget transfers, oil bonds, or a calibrated retail price hike becomes unavoidable.

Scenario C — Supply Shock Escalation

A further deterioration in the Strait of Hormuz situation could force India into emergency crude sourcing, stress the two-month inventory buffer, and trigger more aggressive export restrictions — potentially returning levies to or exceeding March 27 levels.

Conclusion: A Policy Walking a Razor's Edge

India's fortnightly recalibration of fuel export duties is, at its core, a sophisticated act of economic balancing — simultaneously managing consumer price stability, energy security, OMC financial health, refiner competitiveness, and macroeconomic inflation.

The June 1 revision reflects genuine progress in global price normalisation. But the structural vulnerabilities it exposes — the Strait of Hormuz dependence, the SEZ exemption asymmetry, the mounting OMC losses — are problems that predate the West Asia crisis and will outlast it.